Private Credit in Australia: An Investor’s Guide

Discover everything you need to know about private credit, its opportunities, risks, and how to invest in this alternative fixed-income asset class in Australia.

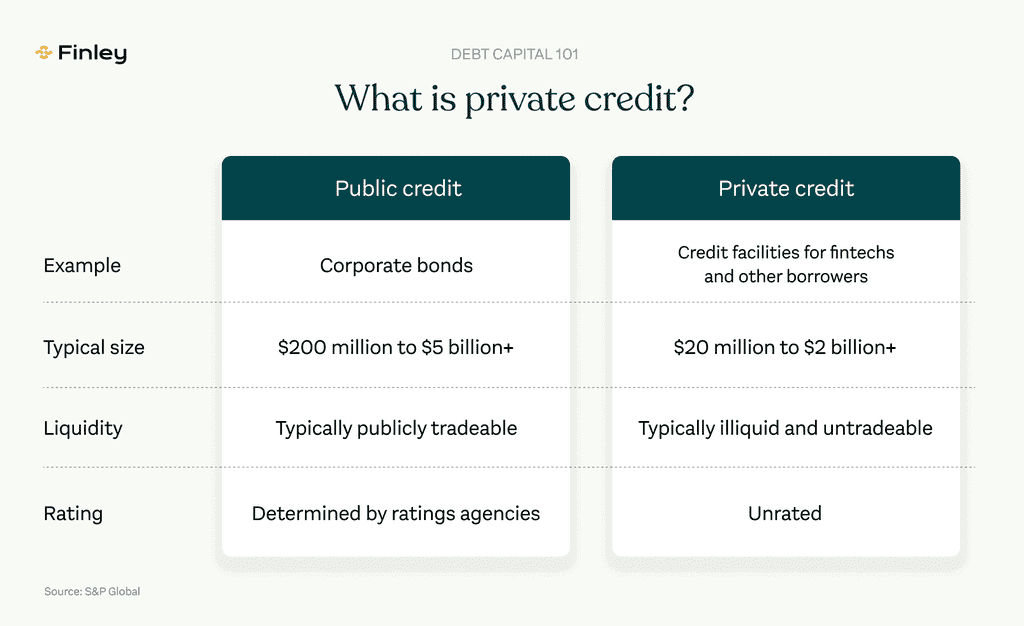

What is Private Credit?

Private credit is a form of non-bank lending whereby capital is provided to borrowers in exchange for interest payments. Unlike traditional bank loans, private credit is issued by institutional investors, private debt funds, or alternative lenders. In recent years, private credit as an asset class has grown significantly in Australia and globally.

Private credit is attractive to many investors due to the solid risk-adjusted returns on offer with minimal correlation to global stock markets. According to the Australian Investment Council, private credit has also become more attractive to lenders since the global financial crisis because: ‘Tighter regulations on banks created demand for private credit as an alternative source of finance from sectors of the market seeking more flexible capital.’

Source: Finlay

The Growth of Private Credit in Australia

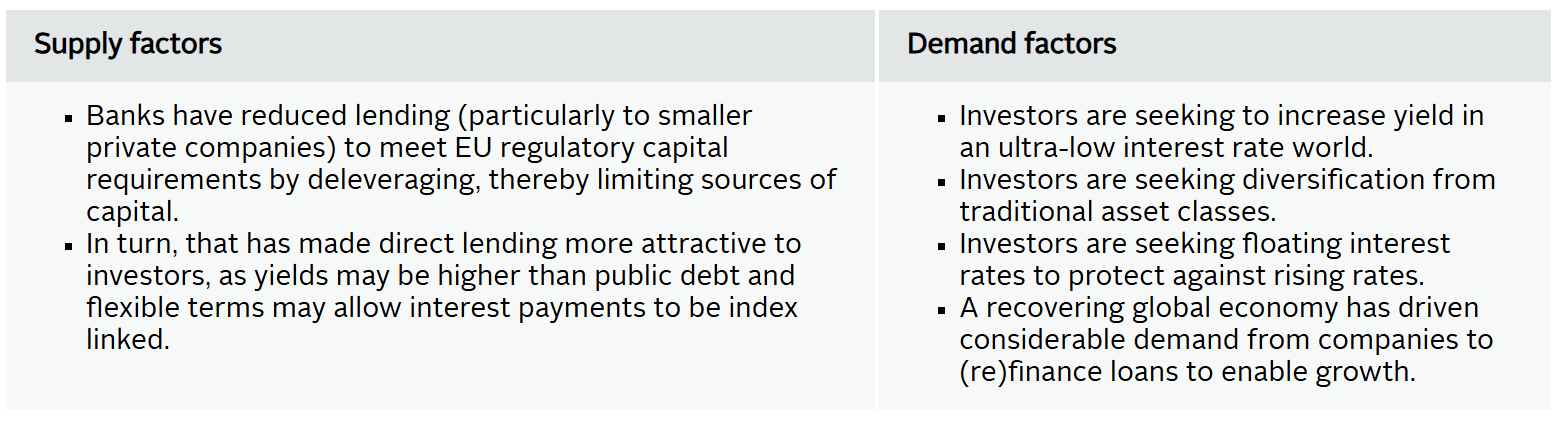

Market Expansion and Rising Demand

The Australian and global private credit markets have grown rapidly over the past decade driven by growing demand for alternative financing while the traditional banks have become more risk-averse, particularly in lending to small and mid-sized enterprises (SMEs).

Source: Adviser Voice

Non-bank lenders, private credit funds, and institutional investors have stepped in to fill this lending supply gap armed with investors’ funds searching for strong risk-adjusted returns with minimal correlation to global equities.

Source: UNPRI

Key Drivers of Growth

A. Post-GFC Regulatory Shifts

The 2008 global financial crisis led to stricter bank lending regulations (e.g. Basel III) all around the world, including in Australia.

According to the Australian Investment Council: ‘a range of measures implemented by the Australian Prudential Regulation Authority have changed the playing field for private credit. As a result, traditional bank lending to small and medium-sized businesses has contracted, opening up opportunities for private lending.’

So recent regulatory shifts have proven beneficial for private credit as an asset class.

B. Rising Interest from Institutional Investors

Australian institutional investors, particularly superannuation funds and family offices, are increasingly allocating capital to private credit funds due the attractive risk-adjusted returns on offer.

According to PGIM Private Capital managing director Michael Jones: ‘Superannuation funds make excellent partners for private market investments due to their long-dated liabilities, which align well with the typically longer-term buy and hold nature of these investments.’

C. Diversification Benefits & Market Resilience

A key attraction of private credit is its low correlation with public equity and bond markets. This explains why so many investors are investing in private credit for portfolio diversification benefits.

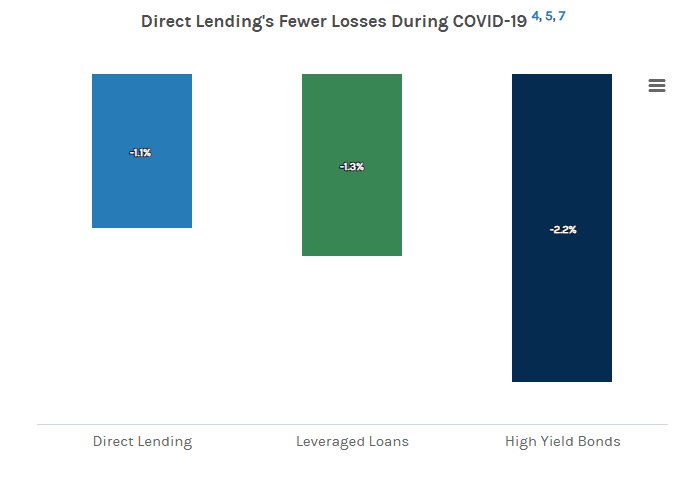

According to Morgan Stanley: ‘Since the global financial crisis, direct lending (the most common type of private credit) has provided higher returns and lower volatility compared to both leveraged loans and high-yield bonds.’

Source: Morgan Stanley

It’s noteworthy that direct lending tends to significantly outperform other types of fixed income investments in high interest rate environments.

Source: Morgan Stanley

Private credit also tends to outperform other types of fixed income during periods of market weakness, such as during the pandemic.

Source: Morgan Stanley

Future Outlook for Australian Private Credit

The private credit market in Australia is expected to continue its on its growth trajectory, following the structural trends seen in the US and Europe. Morgan Stanley expect global private credit AUM to grow from $US1.5 trillion in 2024 to $US2.6 trillion by 2029.

In particular, increased deal flow is expected into a broader array of private credit assets such as real estate lending, infrastructure finance, SME funding, and higher risk commercial property.

Source: McKinsey

As the industry grows, McKinsey expect scale to become increasingly important for private credit lenders: ‘As private credit’s footprint expands into additional, larger subsectors, possessing a certain scale may well be the cost of entry.’

They also expect: ‘a more prominent role in the fundraising, underwriting, and operations of private credit investors in this emerging ecosystem.’

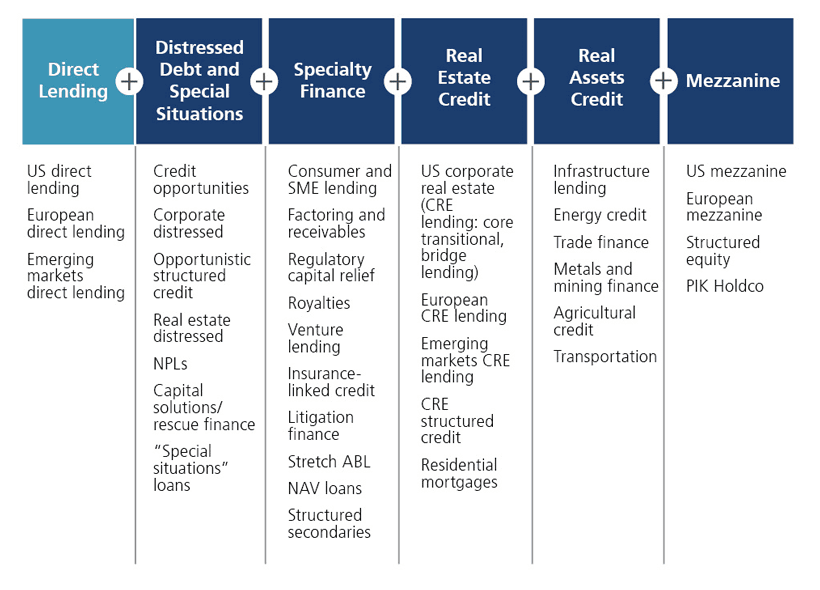

Types of Private Credit Investments

Private credit encompasses six distinct lending strategies, each one offering different risk-return profiles—as shown below.

Source: Calamos

Direct Lending

Direct lending involves providing loans directly to businesses, and is typically secured by assets. This is a common form of private credit in the mid-market corporate financing world.

Mezzanine Debt

Mezzanine debt is a hybrid of debt and equity financing and tends to be used by larger, more established companies. It is particularly common in acquisitions and expansion financing, and generally offers investors higher returns in compensation for a higher risk profile.

Distressed Debt

Distressed debt involves investing in companies experiencing financial difficulties, with potential upside through restructuring. This is a higher risk type of private credit opportunity but offers the potential for substantial returns.

Private Placements

Private placements are publicly traded debt securities issued to a select group of investors.

Special Situation Financing

Special situation financing is short-term or opportunistic lending to companies undergoing major transitions, restructurings, or turnaround situations. It’s aimed at companies requiring bridge financing, asset-backed lending, or event-driven funding. It often carries higher risk but also tends to generate higher returns due to the unique nature of the borrowers’ situations.

Venture Debt

Venture debt is financing provided to early-stage, high-growth start-ups which have secured equity funding but need additional capital to scale. It is generally used as an alternative to diluting ownership through further equity rounds, and often includes warrants or equity kickers as part of the deal.

Key Benefits of Private Credit for Investors

Portfolio Diversification

One of the main benefits of private credit is its low correlation with traditional equity and fixed-income markets. To that point, Russell Investments calculates private credit has a correlation of only 0.33 with US equities, and only 0.20 with the aggregated fixed income asset class—as shown below.

Source: Russell Investments

As a result of these low correlations, investing a portion of their portfolios in private credit helps protect investors during bouts of market volatility.

Enhanced Yield Potential

Whilst the private credit sector’s yields vary based on risk profile and structure, typical returns are higher than for traditional fixed income assets such as government or corporate bonds.

According to Morgan Stanley, private credit generated average returns of 11.6% p.a. between 2008 and 2023, which included the pandemic. Considering the low volatility behind those returns, private credit stands out for its ability to generate strong risk-adjusted returns versus other asset classes.

Source: Russell Investments

Flexible Investment Terms

Unlike standardized bank loans, private credit agreements can be tailored to specific borrower needs. These flexible terms are an important driver of private lending demand growth which is likely to help drive continued growth in private credit assets under management (AUM).

Risks and Challenges of Private Credit

While private credit offers compelling benefits, it also exposes investors to three distinct risks.

Illiquidity

Private credit investments often lack a secondary market, making them less liquid than stocks or bonds. As a result, investors typically need to commit their funds for 2-5 years. According to Lonsec: ‘Illiquidity remains a major challenge, as loans can be long-term, restricting investors' ability to exit positions quickly.’

Credit Risk

Credit risk is generally higher for private credit than for publicly traded debt securities. As a result, investors are exposed to the risk of borrower default, so rigorous due diligence is required. This risk can be mitigated through diversification and strong underwriting standards.

Regulatory Considerations

The Australian Securities & Investments Commission (ASIC) oversees aspects of the private credit markets. As the asset classes grows, investors should expect greater regulatory oversight to emerge. ASIC is leading this discussion forward.

Hence, prior to investing investors should be aware of a fund’s structure, tax implications, and legal considerations of investing in private credit.

Ways to Invest in Private Credit

Investors can access private credit through four investment vehicles, each offering different levels of risk, liquidity, and accessibility.

Private Credit Funds (Managed Investment Vehicles)

Private credit funds are professionally managed funds that pool capital from investors to lend across various private credit strategies, including listed and unlisted opportunities. These funds are ideal for investors seeking diversification and professional management.

For example, Aura Private Credit Income Fund and Arbitrium Credit Partners Fund invest in diversified portfolios of private credit opportunities with the objective of generating solid risk-adjusted returns.

Direct Investments

Investors can purchase private debt securities directly from borrowers. The potential risk-adjusted returns on offer may warrant direct investment for some investors, but this strategy requires thorough due diligence and a long-term capital commitment.

Exchange-Traded Funds (ETFs)

Private credit ETFs provide diversified exposure to private credit opportunities through publicly traded ETFs, usually listed on the ASX. These vehicles allow investors to access diversified private credit portfolios without committing to long-term illiquidity.

Self-Managed Superannuation Funds (SMSFs) & Private Credit

SMSFs can allocate capital to private credit as part of their alternative fixed-income strategy.

By including private credit, SMSFs are able to enhance their tax-efficient income generation, although trustees should be aware of overexposing a fund to illiquid assets like private credit.

ASIC and the ATO have strict rules governing SMSF investments in alternative assets, so this strategy requires careful risk assessment and adherence to compliance regulations. In particular, there’s a risk that private credit investments may not align with the required pension withdrawals.

Advantages of Investing Through Private Credit Funds

Investing in private credit funds provides access to alternative fixed-income opportunities while benefiting from professional management and risk mitigation.

Professional Management & Expertise

Private credit funds are managed by experienced credit specialists who assess borrower risk, monitor loan performance, and structure debt effectively. These funds also have access to institutional-quality underwriting and risk assessments, which serves to reduce their default exposure.

Diversification & Lower Risk Exposure

Private credit funds spread their risk across multiple loans, industries, and borrower types. This helps reduce concentration risk compared to investing in a single direct loan.

Access to Institutional-Grade Opportunities

Most private credit investments are not available to individual investors as they require large capital commitments. Managed funds provide entry into these exclusive credit markets, including real estate, infrastructure, and corporate lending.

Liquidity Options

While private credit is inherently illiquid, some funds offer structured liquidity windows or tradeable options through listed vehicles.

Private credit ETFs also provide exposure to private lending strategies without long-term lockups.

How to Compare Private Credit Funds in Australia

Risk-Adjusted Returns

As a starting point, investors should compare historical private credit fund returns relative to the risks taken.

It’s important to bear in mind that different private credit fund strategies are associated with varying risk-return attributes. For example, direct lending generally offers lower returns than mezzanine financing due to the lower typical risk profile.

Credit Quality & Due Diligence

Investors should assess the financial strength or credit quality of the borrowers within a fund and the collateral backing their loans.

Liquidity & Investment Horizon

Liquidity is also an important consideration as most private credit funds require a long-term commitment. Investors should check whether a fund allows for redemptions or early exits.

Conclusion: Is Private Credit Right for You?

Private credit is an alternative fixed income asset class offering diversification, the potential for high risk-adjusted returns, and flexible lending solutions.

Investing in private credit funds offers investors a number of compelling advantages. However, investors should carefully assess their risk tolerance, liquidity needs, and they should also conduct appropriate due diligence before committing capital to these investment vehicles.

With a proper strategy and fund selection criteria, private credit can play a pivotal role in long-term wealth preservation and portfolio stability.

Head of Content (CFA)

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.