Constantia Investment Partners - Global Equity Fund

The AIM Global High Conviction Fund provides Australian and New Zealand investors with the opportunity to diversify into a unique global equity proposition.

Constantia Investment Partners is an independently owned fund manager, running a single long-only global equities strategy.

We search across sectors, styles and regions to find and invest in businesses that will deliver superior long term returns for our investors.

The portfolio is concentrated with 15 to 25 of our very best international stock ideas.

Our philosophy is simple - exceptional businesses, run by exceptional people, at the right price will deliver out performance over the long term.

With a proven track record of solid returns, our focus is building your wealth so your focus can be enjoying life.

We are aligned with our investors. All staff are invested in the fund and pay fees.

An exceptional company in our view is one with the ability to grow faster and for longer than its peers – leading to higher share prices over time.

While any investor can screen for the numbers, our edge lies in identifying exceptional management teams.

‘The best orchestra can still deliver a bad performance if they’re

not led by a great conductor.’

The same is true of a company. The best employees, strategy and products can still fail, without strong leadership.

That’s why management teams are our focus.

We use our experience and knowledge to identify management teams that are aligned with shareholders and have a track record for creating value.

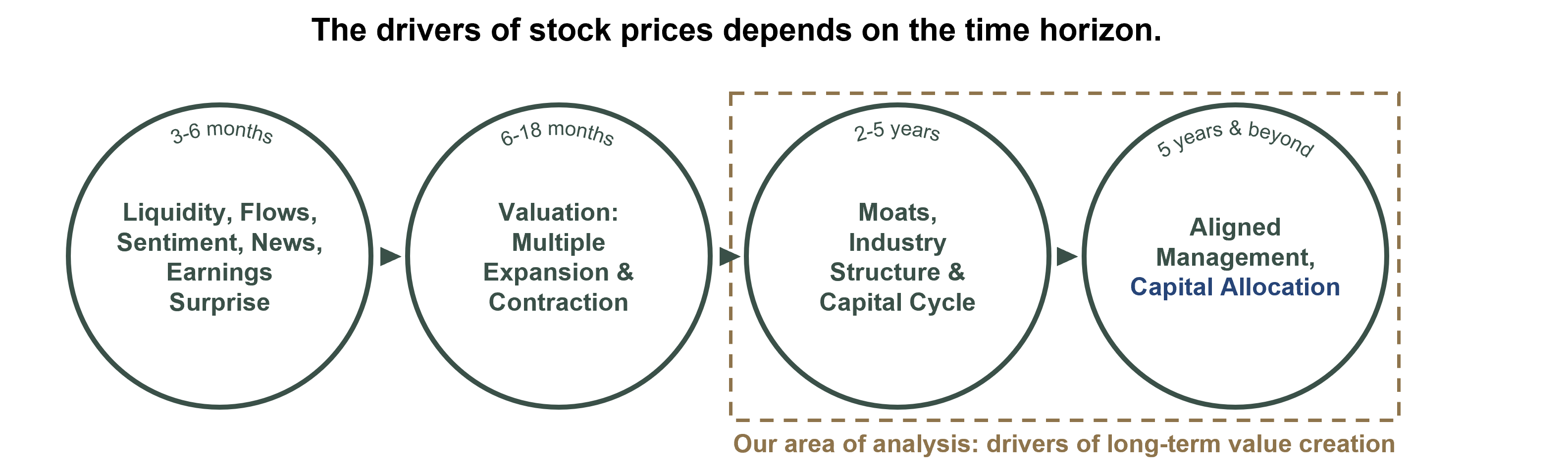

In a world obsessed with short-term gains and quick wins, we believe the best way to sustainably build your wealth is over the long-term.

The average time a stock is held on the stock exchange is five and a half months. It’s near impossible to capture the true value of a company in that time.

Because the market’s focus is so short-term, even exceptional companies can be sold off and undervalued.

When they are - we look to buy these exceptional companies at attractive prices, and hold them for the long-term.

Click here for our latest Pricing and Performance.

The information on this website has been prepared by Constantia Investment Partners Pty Ltd (CIP) (AFSL no. 473 534). Your access to this website is conditional upon your acceptance and compliance with the terms, conditions and disclaimers below and your use of, and/or access to this website constitutes your agreement to these terms of use. This website does not constitute financial product advice nor does it constitute the offer of a financial service and is provided for information purposes only. This website does not contain an offer or invitation to invest in any financial product. The information on this website has been prepared without taking into account any investor’s objectives, financial situation or needs. The information on this website (including any commentary) has been prepared based on information believed to be accurate as of the date of publication and the views of CIP. Assumptions and estimates may have been made which may prove not to be accurate. CIP undertakes no responsibility to correct any such inaccuracy. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information. To the full extent permitted by law, neither CIP or its related entities makes any warranty as to the accuracy or completeness of the information on this website (or the views expressed) and disclaims all liability that may arise due to any information contained in this document being inaccurate, unreliable or incomplete. Past performance is not indicative of future performance. This website may contain links to websites offered by third parties. These linked websites are not under the control of CIP, and neither CIP nor any related entity makes any representations as to the contents of any third party. Privacy Policy

Following recent amendments to the Corporations Act; where you have provided us with your email address, we will now send notices of meetings, other meeting-related documents and annual financial reports (each a “Communication”) to you electronically unless you elect to receive these in physical form and notify us of this election. You have the right to elect whether to receive some or all of these Communications in electronic or physical form and the right to elect not to receive annual financial reports at all. You also have the right to elect to receive a single specified Communication on an ad hoc basis, in an electronic or physical form.

The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL No 235150) is the responsible entity of, and issuer of units in the AIM High Conviction Fund (ARSN 63 603 583 768) (Fund). You should consider the product disclosure statement (PDS) prior to making any investment decisions. The PDS and target market determination can be obtained for free by calling +61 2 8379 3700 or on our website.

Whether you’re a SMSF, trust or an individual wanting to build your wealth, Constantia Investment Partners can work with you to reach your goal. Investing with us gives you direct access to the knowledge and experience of our team.

Our independence means we treat our investors as partners, and our goal is simple – to build your long-term wealth.

We're a team with award-winning international experience investing in global equities.

We believe in our process and portfolio - as owners and co-investors in the fund we are 100% aligned with our clients.

- Morningstar award winning fund manager (Best Global Equity Fund: South Africa, 2019).

- 15 years global investment experience.

- Analyst & Global portfolio manager at Melville Douglas Investment Management, from 2010 to 2019.

- B. Comm. (Honours) Accounting degree from the University of Pretoria; CA(SA) and CFA Charterholder

- 15 years global investment experience.

- Analyst at Investec Asset Management.

- Analyst & Head of research at Foord Asset Management, from 2012 to 2021, in Cape Town and Singapore.

- B. BusSci. (Honours) Finance degree from the University of Cape Town; CA(ANZ) and CFA Charterholder.

- 39 years global fund management experience.

- Worked at UBS, Goldman Sachs, and Dresdner Bank AG in various risk, compliance and senior operating positions.

- Honorary degree from the Securities Institute of Australia for services rendered to the Australian financial markets.

- Member of the Executive Committee of the Australian Alternative Investment Management Association (AIMA).

- 7 years global capital markets experience.

- Analyst & Associate at Bank of America Merrill Lynch, from 2017 to 2019, in Capital Markets.

- B. Comm. Finance and B. Econ. Business & Industry degrees from the University of Queensland.

Click here to view the latest factsheet.

A quality strategy is focused on buying only the best businesses when the market prices them like average businesses. We expect to generate our long-term return from these businesses being able to sustain a high level of return on invested capital for a substantial period of time due to powerful competitive advantages, leading to a compounding effect of their capital base.

While a quality strategy may optically look like a growth strategy, it differs substantially. The question a quality strategy first seeks to answer when evaluating a company is not how fast is the business growing, but rather what return is this business earning on the capital invested to grow?

Economic value is only created when a company can earn a return on capital greater than the cost of capital. Without this precondition being met, the rate of growth a company can achieve is meaningless, because it is entirely possible that growth can destroy value. As such, the first port of call for any quality strategy is to assess the return on invested capital, not the rate of growth.

A quality strategy is a derivation of traditional value investing. However, instead of seeking to buy businesses on optically low multiples, a quality strategy looks to buy businesses at prices below their justified intrinsic value, calculated by analysing the interaction between return on invested capital (ROIC), growth and required reinvestment.

A quality strategy earns alpha due to the market underestimating the compounding effect of the internal capital of high-quality businesses. It may be described as a 'persistence of earning excess returns on invested capital' strategy. A fundamental-based quality investment strategy should deliver superior risk-adjusted returns over multi-year periods, by owning what are in effect compounding machines.

Most investors have a natural home country bias in their portfolio allocation. This makes sense, given that their living costs are naturally going to be denominated in their home currency. However, in having this bias, most Australian investors tend to end up with portfolios that are concentrated in assets that are very closely correlated to the cyclical fortunes of the domestic economy, specifically banking stocks, mining stocks and real estate.

Conversely, it also means Australian investors tend to have low exposure to global opportunities in the technology, health care and consumer sectors. We believe that by investing globally, we can give Australian investors access to a much wider set of opportunities.

This is generally because the businesses we consider for investment have substantially larger end-markets into which they can sell their products or services than is generally the case for businesses listed in Australia. We also take advantage of the fact that where a business happens to be listed is not the determining factor of the underlying opportunities we are exposed to. Many of the companies we seek to invest in derive a substantial portion of their revenues from developing economies.

This enables us to gain exposure to the growth opportunities in developing markets whilst simultaneously benefitting from the governance, legal and market structures of investing in a company listed on some of the major stock markets around the world.

Because we follow a quality strategy, our portfolio will naturally have less exposure to deeply cyclical businesses, as well as businesses with poor balance sheets. This means we expect our portfolio to outperform during periods of market distress and risk-aversion, as well as during a cyclical downturn.

Conversely, during the early stages of a bull market, a cyclical upswing or during an extended risk rally, our portfolio may underperform. This will be because the cheapest assets - likely the most cyclical or those with the weakest balance sheets - rally off very depressed levels.

Over a full business and investment cycle, we believe a quality strategy will outperform the market, mainly because it should protect the downside during periods of distress and keep up with or outperform the market during periods of growth.

We want our fee structure to be simple, transparent, and easily understandable.

Firstly, there is a flat, annual investment management fee of 1.43%. This fee is inclusive of GST, and is accrued on a pro-rated basis over every financial year. In addition to covering our management fee, administrative costs such as audit and legal fees are paid out of this management fee.

Secondly, there is also a performance fee component, calculated as 10% of any outperformance of our benchmark. This performance fee is subject to a high-water mark, meaning we must first recover any prior underperformance before we can charge a performance fee. Practically, this means we must both be above our previous high-water mark and outperforming our benchmark before a performance fee is charged.

Finally, any transaction costs incurred in the management of the portfolio is deducted from the performance of the Fund. Because we look to be long-term investors, we anticipate a low portfolio turnover.

One of the fundamental truths of successful investing is that to do better than the market, one must be different to the market. Because our investment process disqualifies many companies for investment, there is no doubt that any portfolio we construct will differ from a market index. This will be further exacerbated by the fact that we will own a very concentrated portfolio of businesses.

We report the Fund's 'active share' on the Constantia factsheet each month. This measures how the portfolio differs to the Benchmark. A portfolio that fully mirrors the benchmark would have an active share of 0%, whereas a portfolio that has nothing in common with the benchmark would have an active share of 100%. In general, a portfolio needs to have an active share above 60% to be considered as 'actively managed'.

We aim to maintain an active share between 80% and 100%, and we will report this number to you on our factsheet every month.

Why do we focus on this measure? Essentially, a higher active share corresponds with a higher chance of outperformance.

We intend to hold between 15 and 25 businesses in the portfolio at any one time. For some context, this compares to roughly 1,600 businesses in our benchmark and thousands of businesses listed on stock exchanges around the world.

There are several reasons we choose to manage a concentrated portfolio.

Research has shown that the additional reduction in volatility and risk achieved by adding a second, fifth or fifteenth holding to a portfolio is substantial. However, by the time a portfolio has between twenty to twenty-five holdings, the additional reduction in volatility from an additional holding is small; beyond twenty-five, the benefit is negligible. Additionally, there are behavioural considerations to keep in mind.

As one keeps adding holdings to the portfolio, one eventually ends up adding the 30th or 50th 'best idea'. Eventually, this means the number of low-conviction holdings in the portfolio starts to outnumber the actual 'best ideas'. We prefer to own a limited number of businesses we know and understand well, leading to competition for capital when introducing new holdings in the portfolio.

Finally, adding enough additional holdings will eventually lead to owning the entire market. At this point, the investor will merely earn a market return. Because our goal is to outperform the market over time, a concentrated portfolio is a surer path to achieving this.

We do not intend to time the market by making substantial asset allocation calls between equity and cash. Practically speaking, we have a target cash allocation between 0% and 10%, with the view to hold more cash if we cannot find business that meet our criteria trading at valuation levels we consider attractive enough to warrant buying more at the price on offer.

In the unlikely event of an unprecedented global shock - such as war, a natural disaster or a pandemic - our mandate allows us to hold up to 20% of the value of the Fund in cash.

Given our belief that these are extremely rare occurrences, we do not intend to run such elevated cash levels for extended periods, if ever.

Ultimately, we understand that the Fund is not an asset allocation tool. If you have elected to invest in our Fund, we assume you have already elected to allocate a component of your wealth to be invested in international equities

Tags

Published by The Trust Company (RE Services) Limited (Issuer) & Constantia Investment Partners (Investment Manager)

Published by The Trust Company (RE Services) Limited (Issuer) & Constantia Investment Partners (Investment Manager)

Statutory Statement

The issuer of this product is identified at the top of this page. The PDS and target market determination for the product are available in the Documents section of this listing. Prospective investors should consider the PDS before deciding to acquire the product. This product listing was vetted by and approved by the product issuer identified above before publishing. Investment Markets (Aust) Pty Ltd AFSL 527875 (IM) is not the issuer of the product.

General Disclaimer

IMPORTANT STATEMENT ABOUT YOUR USE OF THIS SITE

Information on this site is intended for Australian users only.

This site is operated by Investment Markets (Aust) Pty Ltd. (ACN 634 057 248) (IMA, we, us and our), the holder of Australian Financial Services Licence (AFSL) no. 527875. The content is provided solely for information purposes, is not a recommendation or an offer to buy or sell a security, and is not warranted to be correct, complete or accurate. To the extent permitted by law, neither IMA, its affiliates, nor the content providers (such as the issuers of securities who appear on the site) are responsible for any investment decisions, damages or losses resulting from, or related to, the content, data and analyses or their use. The investment products on this site and any statements made about them by their issuers are not vetted, verified or researched by IMA. The presence of an investment product on this site should not be interpreted as an implied endorsement of it by IMA. Certain content provided may constitute a summary or extract of another document such as a Product Disclosure Statement. To the extent any content is general advice, it has been prepared by IMA. Any general advice has been provided without reference to your investment objectives, financial situations or needs. For more information refer to our Financial Services Guide. To obtain advice tailored to your situation, contact a financial advisor. You should consider the advice in light of these matters and, if applicable, the relevant Product Disclosure Statement (or other offer document) before making any decision to invest. Past performance does not necessarily indicate an investment product’s future performance. The content is current as at date of initial publication and may not be current as at your date of viewing. For a more complete understanding of all the terms and conditions of your use of this site click here.