Remara Private Credit Income Fund

When you invest in our private credit fund you not only have control and flexibility, but the choice of a secure long-term income through monthly payments or reinvestment plan.

Comparison Data

1Performance

| 1 month | 3 month | 1 year | 3 year | 5 year | Since Inception | Inception Date |

|---|---|---|---|---|---|---|

| 0.94% | 2.86% | 13.18% | - | - | 12.75% | 1 Aug 2022 |

Fees

| Management Fee | Performance Fee | Morningstar Total Cost Ratio |

|---|---|---|

| 0.5% | - | 0.71% |

The Fund will provide investors the opportunity to gain indirect exposure to direct credit opportunities through investment into bi-lateral loans, syndicated loans, asset-backed securities, mortgage-backed securities and collateralised loan obligations.

The Manager seeks to deliver the Target Return while seeking to preserve the Fund's capital. The Manager has developed a proprietary risk management framework which forms a fundamental part of its investment process. This investment process has been formed having regard to the Manager’s investment philosophy which gives priority to capital preservation before assessing the income return.

The Fund's investment strategy will impose a minimum 5% credit enhancement for direct or securitised loans. This means that the first 5% of losses will be borne by the originator/manager and not our investors.

The Manager has developed exclusive relationships with a number of ABS and MBS originators. These relationships enable the Manager to closely monitor the underlying credit written by these originators and enables the Manager to ensure that the originator and servicer of the loans are suitably aligned with the Fund through the retention of ‘first loss’ within the loan. The Manager will only invest into the originator’s product offering at the completion of stringent due diligence and enactment of a continuous reporting framework.

The Fund will benefit from diversification of the underlying loan portfolios through the ABS and MBS product suite in addition to direct loans. This diversification reduces the prospect of significant capital loss. The total return of the Fund may rise or fall based on, amongst other things, performance in the underlying investments and movements in the BBSW Rate.

During times when the Fund is not fully invested, the Fund may invest in short-term government obligations, certificates of deposit, commercial paper and other money market instruments.

Below outlines the types of credit investments available to the Fund. The Fund will primarily focus on ABS and MBS products, however, will gain exposure across the spectrum as opportunities present.

- Corporate Loans

- Project Finance

- Leveraged Buyouts

- Securitised Loan Structure

- Mezzanine Loans

- Real Estate Loans

- Asset Backed Security (ABS)

- Corporate Bonds

- Convertible Notes

- Collateralised Loan Obligation (CLO)

- Mortgage-Backed Security (MBS)

Below outlines the types of common loan structures that the Fund may be involved in in its debt investments.

Direct lending (bi-lateral)

This is the most common form of lending between borrowers and lenders in corporate and business lending. Bi-lateral lending refers to individually negotiated loan transactions which are often highly bespoke, containing specific terms and conditions relevant to the borrower’s corporate profile and industry.

Syndication

Syndicated debt refers to a group of lenders, sharing common security, terms, pricing and covenants providing finance to a borrower. Commitments are shared on a pro-rata basis upfront and held for the life of the loan. Security is held by a Security Trustee (with lenders ranking pari-passu) and all communication with the borrower is managed by an agent on behalf of the lenders. Amendments to facilities generally require majority lender consent.

Securitisation

Securitisation involves creating debt securities directly out of cashflows from specific assets such as home loans or corporate loans. The originator of the loan retains an ownership in the loan and services the loan on behalf on the security holders. Securitisation is a method that allows the transfer of a loan or portfolio of loans to investors in different sizes and risk profiles, creating multiple tranches within a larger pool of loans.

The Fund intends to invest in a portfolio of loans to Australian corporate and business borrowers, in line with the Fund’s investment strategy, with diversification across borrower, industry, geography and loan types.

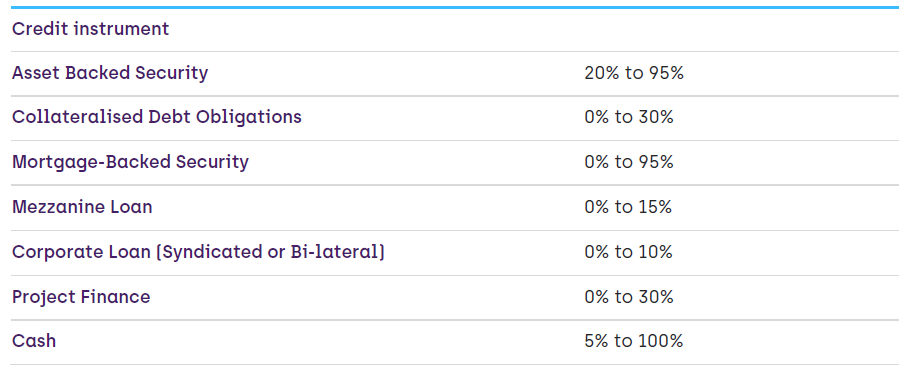

Target parameters for loan type will be aligned to the loan strategies as follows:

The Fund’s investment strategy composition depicted above is illustrative only and is based on the Manager’s current expectations but may not reflect the actual allocation of the Fund’s investments.

Click here to view the consolidated performance returns for our investment funds. For in-depth, month by month returns please refer to the individual fund page. Please note that past performance is not a reliable indicator of future performance.

As an Australian based Asset Management company, Remara Investment Management is focused on achieving attractive results and helping you make your money go further.

As a business we currently manage in excess of $1.7bn in funds, offering investments across three key asset areas, private credit, real estate and tactical opportunities, with the intention to increase your personal and/or family wealth.

Our investors have the ability to choose their level of investment risk and associated return on investment. Diversify your wealth, reduce your portfolio risk and gain exposure to higher returns.

Andrew founded Remara, a Sydney based investment firm, focusing on real estate, private credit and tactical investment.

Prior to commencing Remara, Andrew held multiple positions within Brookfield Asset Management across the Australian and Asian Platforms.

Andrew most recently held the position of CFO AsiaPacific covering Financial Leadership of both Brookfield Property & Private Equity Group across Asia-Pacific and Brookfield’s Corporate Operations for Asia-Pacific. This followed previous roles covering Group Finance, External Investments, Infrastructure and Commercial Properties.

Prior to joining Brookfield, Andrew gained experience in Audit, Corporate Taxation, Corporate Finance and Business Services within Industry.

Andrew currently holds a Bachelor of Business in Accounting and also a Masters in Finance.

He has served on the CFO Round-table and the National Accounting Round-table for the Property Council of Australia, while also serving as a Steering Committee member for the Bachelor of Accounting Scholarship course at The University of Technology Sydney.

Andrew also served as a board member of the Cronulla Sharks Football and Leagues Club, holding the roles of Chair of the Audit, Risk and Compliance Sub-Committee and the Property Sub-Committee.

David is a Managing Partner of Remara, focusing on debt capital markets, private credit and private equity relating to financial services.

David founded Grow Finance Limited in December 2016. Grow is an Australian non-bank lender, focusing on small to medium enterprises.

David's background includes over 25 years of investment banking and finance experience. David started his finance career as a credit analyst at Westpac and became responsible for capital raising and trading corporate debt from 2001 at BNP Paribas in Tokyo and Hong Kong in 2004.

Moving back to Australia in 2009, David was instrumental for raising capital for Australia's largest non-bank financial institutions which included mortgage-backed debt as well as consumer and auto finance.

David has a Bachelor of Finance (Information Technology), Master of Applied Finance, Certificate IV and Diploma of Finance & Mortgage Broking.

Click here to view our latest News & Insights.

Click here to view our latest Monthly Update.

No, the Fund invests into a portfolio of underlying direct loans to borrowers across multiple product and asset classes. The return to fund investors is not guaranteed and is subject to underlying market conditions. The fund has a target return rate of 4% above the RBA cash rate. The underlying return post fees to investors could be higher or lower than the historical track record of 10.5% achieved to date.

The Fund will pay monthly distributions on the 15th of each month.

Yes, the fund offers a dividend reinvestment program.

Fund investors will have an open period at the end of each quarter to request a redemption. Redemptions will be completed 15 days after the end of the quarter. Investors should review the conditions around redemption in the Investment Memorandum.

The fund invests into secured bankruptcy remote trusts. The underlying loan portfolio within the trusts are all secured. The fund does not invest into unsecured loan products.

Remara has established relationships with proven and profitable loan originators and servicers. Remara undertakes a review of the credit policy and sets stringent portfolio and credit parameters to ensure a tight credit structure is maintained. Remara on a monthly basis will monitor the ongoing credit of the investment portfolio. Each originator retains a ‘first loss’ position in the loan.

Remara has structured its investments to require the loan originator to fund and retain a ‘first loss’ portion of the loan. This means in the event of a credit loss, the originators capital is paid last in the recovery scenario. This results in an improved credit enhanced position for fund investors as the originator is aligned to fund investors with their money at risk ahead of fund investors.

No, Remara is an investment manager regulated by the Australian Investment and Securities Commission via a Financial Services licence.

No, as Remara is not an Australian deposit taking institution, the investment is not covered under the guarantee.

Tags

Published by Remara Investment Management Pty Limited

FIXED INTEREST

PRIVATE ASSETSINVESTOR EDUCATION

Published by Remara Investment Management Pty Limited

Statutory Statement

The issuer of this product is identified at the top of this page. The PDS and target market determination for the product are available in the Documents section of this listing. Prospective investors should consider the PDS before deciding to acquire the product. An investment in the product is not a bank deposit and investors risk losing some or all of their money. This product listing was vetted by and approved by the product issuer identified above before publishing. Investment Markets(Aust) Pty Ltd AFSL 527875 (IM) is not the issuer of the product.

General Disclaimer

IMPORTANT STATEMENT ABOUT YOUR USE OF THIS SITE

Information on this site is intended for Australian users only.

This site is operated by Investment Markets (Aust) Pty Ltd. (ACN 634 057 248) (IMA, we, us and our), the holder of Australian Financial Services Licence (AFSL) no. 527875. The content is provided solely for information purposes, is not a recommendation or an offer to buy or sell a security, and is not warranted to be correct, complete or accurate. To the extent permitted by law, neither IMA, its affiliates, nor the content providers (such as the issuers of securities who appear on the site) are responsible for any investment decisions, damages or losses resulting from, or related to, the content, data and analyses or their use. The investment products on this site and any statements made about them by their issuers are not vetted, verified or researched by IMA. The presence of an investment product on this site should not be interpreted as an implied endorsement of it by IMA. Certain content provided may constitute a summary or extract of another document such as a Product Disclosure Statement. To the extent any content is general advice, it has been prepared by IMA. Any general advice has been provided without reference to your investment objectives, financial situations or needs. For more information refer to our Financial Services Guide. To obtain advice tailored to your situation, contact a financial advisor. You should consider the advice in light of these matters and, if applicable, the relevant Product Disclosure Statement (or other offer document) before making any decision to invest. Past performance does not necessarily indicate an investment product’s future performance. The content is current as at date of initial publication and may not be current as at your date of viewing. For a more complete understanding of all the terms and conditions of your use of this site click here.

1 For use in Australia: © 2025 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its affiliates or content providers; (2) may not be copied, adapted or distributed; (3) is not warranted to be accurate, complete or timely and 4) has been prepared for clients of Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892), subsidiary of Morningstar. Neither Morningstar nor its content providers are responsible for any damages arising from the use and distribution of this information. Past performance is no guarantee of future results.

Any general advice has been provided without reference to your financial objectives, situation or needs. For more information refer to our Financial Services Guide at http://www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement before making any decision to invest. Morningstar's publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Morningstar's full research reports are the source of any Morningstar Ratings and are available from Morningstar or your advisor. Past performance does not necessarily indicate a financial product's future performance. To obtain advice tailored to your situation, contact a financial advisor. Some material is copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782.