WayFinder Searcher Growth Fund I.L.P.

Australia’s first institutional fund to exclusively focus on investing in talented entrepreneurs looking to acquire and scale mid-market businesses. (For Wholesale Investors Only)

The WayFinder Searcher Growth Fund in a Nutshell:

- Up to $25M in committed capital fund as a VCLP.

- First fund in Australia to invest exclusively in Search Funds and Searcher-led transactions.

- Targeting an investor IRR of +20% (net of all fees).

- Search Funds are a globally proven investment vehicle for backing talent and investing in Mid-Market Enterprises (MME) businesses.

- Will invest in ~20 acquisition entrepreneurs in both their two year search phase and subsequent acquisition of the highest quality Australian "MME" businesses.

- $11m raised to date and

The Fund will seek to invest in the buyout of ~20 mid-market enterprises over a six-year period using the Search Fund Model.

The Fund will target returns equivalent to an IRR of 20% per year over a 11-year period. This is a target and may not be achieved.

The risks associated with investing in capital ventures are significant and Investors should read the Information Memorandum in its entirety before deciding to invest.

Fund

- Tax neutral VCLP

- First close achieved July 2022

- Second close achieved September 2023

- Current committed capital totals $11m, ~$3.5m called to date

- Final close targeted for March 2024 targeting additional ~$14m (to being total committed fund size of ~$25m)

- Deliver outstanding investor returns

- Fund has been operating since July 2022 and as at 5 November 2023 holds:

- Three investments in portfolio investments; and

- Six investments in search funds.

Commitment

- Minimum commitment of $500,000

- Plan to deploy capital by end of 2026 (over 4.5 years from fund first close )

- Capital called as required

- Capital returns expected to commence year seven

Target Returns (Pre-tax IRR of 20% (net) after:)

- Management Fee

- Carried Interest of 20% over performance hurdle of 8%

Unique in Australia

- Targeting access to ~20 entrepreneurs dedicating 100% of their time for two years in searching for business

- Proven business and financial model overseas (+35 years in the US)

- Investments are made in the search and/or buyout phase

- Minority but significant equity investments

- Stable, sustainable low-mid-market businesses with simple business models

- Tracking a pipeline of talented entrepreneurs and pending searchers currently in or intending to return to Australia

What is a Search Fund?

A financial vehicle and an entrepreneurial path undertaken by one or two individuals (the “Searchers”) who form an investment vehicle with a small group of aligned investors, some of whom become mentors, in order to search for, acquire, and lead a privately held company for the medium to long term. [Stanford GSB: 2020 Search Fund Study]

The objective of the Fund is to deliver returns to Investors equivalent to a net internal rate of return of approximately 20% per year over an 11-year period after management fees and performance fees (~2.7x capital invested). This is only a target and may not be achieved.

The Fund will aim to leverage the Fund Manager’s deep networks within Australia’s Searcher community to source Searchers who will pursue investment opportunities in mature MME businesses. Targeted businesses have the potential for high revenue growth when driven by a motivated entrepreneur (the Searcher).

The Fund Manager has an active management approach and will seek to work closely with the Searchers and the companies in which the Fund invests to help drive a return on capital.

WayFinder will typically invest the Fund’s assets as follows:

- ~$25,000 – $210,000 in the search phase; and

- ~$0.75 – 3.00 million in the acquisition of an investee company.

The Fund Manager targets ownership stakes in the range of 10% to 30% across the portfolio. The Fund Manager may invest above or below these thresholds where it believes it is in the interests of the Fund.

The Fund intends to:

- Maintain a diverse portfolio;

- Seek to appoint a director to the board of each portfolio company where it has a significant equity interest (this may or may not be a Principal of the Fund);

- Have appropriate shareholder protections and preferential rights as an investor in each portfolio company;

- Have meaningful input on key strategic decisions; and

- Work closely with the management of each investee company to help accelerate growth, mitigate risk, and maximise returns.

The Fund will co-invest alongside other parties. These co-investors may be third party entities and may be related to or associated with the Fund Manager or members of the Investment Team.

The Fund intends to maintain a relatively concentrated portfolio, limiting its investments to approximately 20 businesses. In the Fund Manager’s view, this will enable the Fund Manager to be actively involved in each investee company whilst ensuring appropriate diversification of risk. The Fund Manager will generally seek to appoint a director (this may or may not be a Principal of the Fund) to the board of each portfolio company and will endeavour to secure appropriate shareholder protections. It is expected that the Fund Manager will have meaningful input on key strategic decisions and will work closely with the management of each portfolio company to help maximise the probability of success.

Potential investors in the Fund should be persons seeking access and exposure to a portfolio of privately held, cash-flow-generating MMEs with potential to generate high returns on investment. The Fund may be suited to investors who do not necessarily have the expertise or resources to undertake direct MME investments.

The Fund allows such investors to leverage the deal flow and experience of the Fund Manager to source prospective investments, actively engage with investee companies, manage portfolio risk, and maximise returns.

Investment in the Fund involves a high level of risk, and redemptions or withdrawals from the Fund are not permitted. Accordingly, an investment in the Fund is not suitable for investors who are unable to sustain the loss of all or part of the sum invested, or who require predictable levels of return or liquidity. Please refer to Section 6.0 of the Information Memorandum on investment risks.

Issuer

This Information Memorandum dated 19 October 2023 (IM) has been prepared and issued by WayFinder Capital Managers Pty Ltd ACN 645 959 128 (WayFinder Capital, WayFinder, Fund Manager, us, we or our) to provide background information for persons considering applying for interests in the WayFinder Searcher Growth Fund I.L.P. (Fund). No persons other than the Fund Manager have caused or authorised the issue of the IM nor do they take any responsibility for its preparation.

The Fund

The Fund is an incorporated limited partnership registered in Western Australia (ILP L2021002) and has applied for conditional registration as a Venture Capital Limited Partnership (VCLP). Persons who successfully subscribe to the Fund will become limited partners of the Fund.

WayFinder Management Partnership I.L.P. (ILP L2021001) is the general partner of the Fund (General Partner). The General Partner is an incorporated limited partnership registered in Western Australia that operates as a Venture Capital Management Partnership (VCMP). The General Partner's general partner is WayFinder Capital.

The General Partner has appointed WayFinder Capital (in its own capacity) as the manager of the Fund under a management agreement, and as manager, WayFinder Capital will source and present investment opportunities to the Fund

WayFinder Capital is the authorised representative (No 001285888) of Acrux Capital Pty Ltd ACN 608 420 873, holder of AFSL Number 492534. WayFinder Capital intends in the future to obtain its own AFSL and is preparing an application for its own AFSL. Offers of Partnership Interests under the IM will be made under an arrangement between the Fund and WayFinder Capital as an authorised intermediary. The Fund has authorised WayFinder Capital to make offers to arrange for the issue of Partnership Interests.

Important information

The IM should be read in its entirety before making a decision to invest in the Fund. An investment in the Fund is subject to the terms of the Investment Documents, which are summarised in the IM. The IM is not a comprehensive statement of the Partnership Deed or of all of the terms applicable to an investment in the Fund. A copy of the Fund’s Partnership Deed can be obtained by contacting WayFinder Capital. In the event of any inconsistency between the Investment Documents and the IM, the Investment Documents will prevail to the extent of the inconsistency.

An application to invest in the Fund is an application for Partnership Interests based on the Investment Documents. Information in the IM is subject to change from time to time. We intend to issue a supplementary or replacement IM if any material changes are made. No person is authorised to provide information or to make a representation in connection with the Fund that is not contained in the IM. Any information or representation in connection with the Fund that is not contained in the IM may not be relied upon as having been authorised by the Fund Manager. No representation or warranty is made as to the achievement or reasonableness of any plans, financial returns or forward-looking statements.

The IM does not constitute, and may not be used for the purposes of, an offer of an interest in, or an invitation to apply to participate in, the Fund by any person in any jurisdiction in which such offer or invitation is not authorised or in which the person endeavouring to make such offer or invitation is not qualified to do so or to any person to whom it is unlawful to make such an offer or invitation. No action has been taken to register or qualify interests in the Fund, the invitation to participate in the Fund, or to otherwise permit any public offering of Fund interests in any jurisdiction.

It is the responsibility of prospective Investors to satisfy themselves as to full compliance with the relevant laws and regulations of any territory in connection with any application to participate in the Fund, including obtaining any requisite governmental or other consent and adhering to any other formality prescribed in such territory.

By receiving and viewing the IM, the recipient is warranting that they are legally entitled to do so, that the securities laws of their relevant jurisdiction do not prohibit them from acquiring interests in the Fund and, if they reside in Australia, that they are a Wholesale Client (as defined in the Corporations Act).

Investments in the Fund will be by invitation only. No public offer of Interests in the Fund will be made. An interest in the Fund may be offered in a jurisdiction outside Australia only where such an offer is made in accordance with the laws in that jurisdiction.

With respect to Australian jurisdiction, the IM has been prepared on the basis that prospective Investors are Wholesale Clients. Accordingly, the IM is not a Product Disclosure Statement for the purposes of Part 7.9 of the Corporations Act. The level of disclosure in the IM is less than that of a Product Disclosure Statement, prospectus or similar disclosure document. A copy of the IM does not need to be and has not been lodged with the Australian Securities and Investments Commission (ASIC).

The information in the IM is general advice and does not constitute personal advice or investment advice. In preparing the IM, WayFinder Capital has not taken into account the investment objectives, financial situation or particular needs of individual investors. WayFinder Capital strongly recommends that potential investors read the IM in its entirety and seek independent professional advice as to the financial, taxation, and other implications of investing in the Fund and the material contained in the IM.

No person guarantees the performance of, or rate of return from, the Fund nor the repayment of capital from the Fund. Investments in the Fund are not deposits with or liabilities of the Fund Manager or any associated company and are subject to investment and other risks, including possible delays in repayment and loss of income or principal invested. Recipients of the IM should ensure they are fully aware of all these risks before investing in the Fund. As with any investment, there are inherent risks in investing in the Fund, including the risk that an investment in the Fund is speculative, that the investment may result in a reduction in or loss of the capital value of the investment, loss of income and returns that are less than expected or delays in repayment of capital.

Investing in the Fund involves a high level of risk and is not suitable for investors who are unable to sustain the loss of all or part of the sum invested, or who require predictable levels of return or liquidity. Please refer to Section 6 on investment risks.

To the maximum extent permitted by law, none of the Fund Manager, its associated entities, nor any of their respective officers, directors, advisers or associates provide any representations or warranties in relation to the IM or the Fund and they disclaim all liability and responsibility in relation to the IM and the Fund. The Fund Manager does not make any representation or warranty as to the accuracy or truth of the contents of the IM.

Any information or representations not contained in the IM may not be relied upon as having been authorised by the Fund Manager and should be disregarded. The IM supersedes all previous representations and communications (including investor presentations) in respect of the Fund. The Fund Manager may vary the offer without notice at any time, including to close the offer at any time, accept late subscriptions, or to increase or decrease the size or timing of the offer, without notice.

Any forward-looking statements in the IM (including statements of intention, projections and expectations of investment opportunities and rates of return) are made only at the date of the IM based on current expectations and beliefs but involve risks, contingencies, uncertainties and other factors beyond the control of the Fund Manager which may cause actual outcomes to be materially different. Assumptions underlying such statements involve judgements which may be difficult to accurately predict. Therefore, such forward-looking statements included in the IM may prove to be inaccurate and should not be relied upon as indicative of future matters.

Neither the IM nor any other information provided by the Fund Manager may be disclosed to any other party, except for the purpose of obtaining independent advice in connection with the consideration of an investment in the Fund or used for any purpose other than the consideration of an investment in the Fund, unless the express prior written consent of the Fund Manager is obtained. Any reproduction of all or part of the IM is strictly prohibited without the written consent of the Fund Manager.

All amounts in the IM are stated in Australian currency, unless specifically stated. Fees and costs in the IM are disclosed exclusive of Goods and Services Tax (GST). Applications to invest in the Fund may only be made on the application form attached to or accompanying the IM. The General Partner is not obliged to accept applications and reserves absolute discretion in limiting or refusing any application in whole or in part.

Certain capitalised words and expressions used in the IM are defined in the Glossary of the IM.

Our Ethos:

- Talent First. Acquisition targets will come and go. What we know is that backing the right talent into an acquisition will create value.

- Skills & Aspiration. Work with high-energy entrepreneurs who can lead, sell and relate; have empathy, listen, and are open to learning.

- Value is built over time. Patient capital is needed for long-term, sustainable value creation.

- Be active in the global Search Fund community.

Introduced to one another by a mutual colleague in 2008, Lui and Ak began ‘trading notes’ on their combined experiences of helping clients with growth, mergers, acquisitions, MBOs and other forms of business transitions.

This led them to discover – and get passionate about – the Search Fund concept and investment asset class. In 2018 they established Second Squared to officially introduce Search to the Australian market and accelerate the opportunity for growing a thriving Search community here.

The unexpected speed with which the community has grown has led them to establish WayFinder Capital in 2021 with Nima Sedaghat, Australia’s leading practising corporate lawyer and expert on Search Funds.

Lui is a Managing Director and Co-Founder of WayFinder.

Lui has had significant involvement in corporate development activity (mergers, acquisitions and divestments) in a range of industries covering transport and logistics, retail, chemical manufacturing, professional services, marine and civil engineering, laboratory services, subscription-based technology services, and for-purpose organisations.

As Principal of Loop Advisory, he has spent more than 15 years working with business owners and executives to grow the sustainability and value of both themselves, and their businesses (including through mergers, acquisitions and divestments). Lui will continue to operate Loop Advisory on a part-time basis as he has done for the last three years.

He is an experienced executive and business coach, Non Executive Director and a member of the Institute of Chartered Accountant and a graduate of the Australian Institute of Company Directors.

Lui co-founded Second Squared five years ago to develop the ecosystem and accelerate the development of the Searcher Community in Australia. He has mentored and provided advice to many of the existing Searchers throughout their searches and acquisitions.

SABBAGH1698905739155.png)

Ak is a Managing Director and Co-Founder of WayFinder.

Ak has worked extensively with entrepreneurs and business owners in the MME sector across Australia for over 20 years.

As Principal and Director of Beckon Business, his work has primarily focussed on sustainable business growth, alignment of commercial strategy with partnership/shareholder aspirations, structuring for growth (including setting up of boards and governance processes), acquisitions, and succession (MBO, outright sale, etc).

Whilst his career began in the corporate world in organisations like IBM, EY, PMP Ltd etc, and part of his coaching and consulting practice services this market, his real passion lies in the MME sector where he has worked across a broad sphere of industries including Federal and State Governments, forpurpose organisations, banking, financial planning, accounting, town planning, property, legal, bio-technology, engineering and construction, mining & mining services, advertising, hospitality, IT, and manufacturing. Ak will continue to operate BeckonSecond Supplementary Information Memorandum - Business on a part-time basis as he has done for the last three years.

His understanding of the challenges of the MME environment led him to start up (and subsequently sell) MyHRadvisor – a boutique HR consulting practice to the MME sector. Pre GFC, he also started up MyGM which provided outsourced ‘growth focussed’ general manager solutions to MMEs struggling to find the right talent at that level to support their growth.

Ak is an experienced executive and business coach, certified internationally as a Master Practitioner (European Mentoring & Coaching Council Accredited), a Non-Executive Director and Chair on advisory and formal boards, and a graduate of the Australian Institute of Company Directors.

Ak co-founded Second Squared in 2018 to develop the ecosystem and accelerate the development of the Searcher Community in Australia. He mentors and advises many of the existing Searchers throughout their searches and acquisitions.

Nima is a Managing Director and Co-Founder of WayFinder.

He has spent over 15 years advising business owners, executives, Australian and foreign investors on business restructures, mergers, acquisitions, and investment transactions.

As both a lawyer and chartered accountant, Nima has been appointed to senior roles in professional service organisations such PwC and Deloitte, and law firms Minter Ellison and HWL Ebsworth.

Nima has been active in the Australian Search Fund ecosystem since 2017, having advised on structuring the first traditional funded Search Fund in Australia. In this context, Nima is well known in the Australian search ecosystem and recognised as being a leading adviser on search funds in Australia.

Nima will be actively involved in the Fund Manager’s evaluation of Searchers and the structuring of potential acquisitions by WayFinder investees, as well as ongoing portfolio management.

Click here for our latest News.

Please click on the below PDF to read "Searching for the perfect opportunity" that was in the Australian Financial Review.

1. The Fund aims for 20% return to LPs. Was that compound return?

Yes, this is a 20% IRR to investors based on pure money going in and money going out. Broadly speaking, investor calls will be made over the next two to four years and then returned over the following five to seven years.

2. The searchers get 8.3% for originating the deal with the balance up to 25% on meeting hurdles?

Yes, in practice they are allocated all 25% but only get ownership in tranches (vesting conditions).

The first 8.33% (of the 25%) of the ordinary shares vests on the day that the business is acquired.

The next 8.33% vests monthly over four years.

The balance vests based on the return that they give to the investors in that search and business (which includes us). They start to earn it at 20% and completely get it at 35% IRR.

One exception to the above – the 25% relates to a single searcher and it increases to 30% in the case of a partnered search (i.e. two people going into it together). We can do this because the success rate of partnerships is somewhat better than single searchers. The other exception to the above is where we participate in a Self-Funded Acquisition, where terms will be negotiated and agreed on a deal by deal basis.

3. No above hurdle performance is paid until there is a sale.

Yes, for the searcher – their ordinary shares are worthless until the investors have received all of their capital back and then an 8% return.

Yes, for investors in our fund – we (as the General Partner) also do not receive performance fees until we have returned all investor money and an 8% compound return.

4. Management fee is only paid once 8% return is achieved.

No, our management fee starts from Day 1 and is paid quarterly in advance.

The management fee to the fund manager enables the fund manager (i.e. the General Partner) to do the work required to source 25 searchers over the five years and make ~20 acquisitions.

5. How is 8% calculated prior to a sale. i.e as we go along is there any calculation of the value of the business or is this yield only?

5. How is 8% calculated prior to a sale. i.e as we go along is there any calculation of the value of the business or is this yield only?

There are two aspects to the question:

(a) How do we calculate the 8% hurdle value?

The 8% hurdle is converted to a daily hurdle rate of 0.021087%.

Whilst we (the Fund Manager) will maintain these calculations for the fund, they will also be prepared by an external fund administrator and audited by a third-party accounting firm.

(b) Cash flow yielding business or Value uplift on a specific investment?

The hurdle capital is only impacted by cash in or out. So, if the business pays a dividend or does some other form of distribution (e.g. buyback of the redeemable preference share) it will reduce the capital (i.e. some cash has come out).

The hurdle capital continues to increase regardless of business performance as that is the base rate to be achieved.

Some of the businesses will produce a yield, but not all. It will depend on how each business acquisition is structured (quantity of debt, repayment scheduled) and business performance. Should businesses that we invest in pay a dividend it is likely we would use that first to pay management fees, rather than making another cash call from investors.

(c) A side note:

As part of our reporting to our investors in the fund (i.e. the Limited Partners) we will periodically value the portfolio. At each valuation point we show aggregate value of the fund, the investors portion of the fund, and their original cost and the hurdle that must be achieved for that investor.

6. What happens if returns are above 20%?

To clarify, the 20% is the target net return to investors after all management fees and performance fees.

If the investments do better than this, then the uplift is split 80% Limited Partners (investors) and 20% General Partner (manager).

7. I see and have skimmed the US/EU reports on search funds and saw the estimated returns on Search Funds over time. I didn’t see any data on returns of Funds of Search Funds – do you have any sense of what this looks like?

There is no published data that we have found (on Prequin, S&P, Orbis), it is relatively closely guarded and only shared formally with investors in those funds.

We understand from our discussions with the Funds of Search Funds that they are all targeting similar to private equity returns.

8. You are seeking a total of $25M but can kick things off with $10M. Is the additional $15M also being applied to Searching or the late Financing stage?

All funds raised across the life of the fund will be applied to both the search and acquisition financing stages – we are aiming for a blended return across a portfolio of the estimated ~20 acquisitions.

During search phase

9. What control do Search Fund investors have over activities of the search fund and how funds are used?

Each Searcher (or Search Partnership) raising a fund has a Private Placement Memorandum which goes into some detail on their proposed search – where (thematic or opportunistic), what (size), how (use of external resources including interns). It is a good starting point for them to begin with but also naturally evolves as they learn from and during the process.

Each Searcher is also required to provide a report on their activities (essentially pipeline and negotiations) – some do this quarterly, some monthly.

10. What controls/vetoes do investors have?

The investors in the Search Fund have the ultimate veto of not participating in the acquisition. There are discussions that also take place amongst the investors. The reality is that it never gets to a veto – we have one-on-one calls with the searchers that we are closely tied to (and expect to invest in) and are seeing the opportunities that they are looking at before they get too far in.

11. What happens to unused funds?

Any unused funds are returned to the investors.

Once an acquisition target has been found

12. How do the ‘right of first refusal to invest’ rules work? Proportionate to search fund investment?

Yes, proportionate to the investment in the search, and then also pro-rata for any shortfall (if for example one of the investors is unable or unwilling to contribute to the acquisition)

13. “If we choose not to invest, our contribution to the search fund converts to equity…” is this always at the 1.5x multiplier?

Yes, the 1.5x multiplier is locked in. If for some reason we didn’t want that there would be a shortfall and we would seek to offload our shares to one of the other investors, but we think it is unlikely that this will occur.

14. How does the 25-30% equity for Searchers work? Are they expected to invest a little? How does this rank?

The searcher’s equity is their incentive. They are not expected to contribute cash, they have already contributed sweat as all of them could earn more than the Searcher salary during the search by working as an employee in an organisation. The standard amounts in a funded search for a sole searcher is 25%, in a partnership it is 30%. This vests in three tranches:

- 1/3 of the total amount upon acquisition of the entity

- 1/3 of the total amount monthly over the first four years post acquisition; and

- 1/3 based on the IRR achieved by the equity investors. The hurdle is 20% (at which point it starts being earned) and is fully earned (or vested) once the investors have achieved an IRR of 35%:

15. How do exits normally work?

A sale can be instigated by shareholders who collectively own 50% of both preference and ordinary shares and force it through the drag/tag alone.

The reality is that the Searcher is incentivised through the last vesting component to exit at a time that crystallises more of the upside for them. This gets relatively harder through the impact of compounding. The overseas experience on timing is 4-6 years is common. Exceptional businesses are held longer (or recapitalised allowing the Searcher to crystallise some upside and investors to take money off the table).

A range of options present themselves in terms of a liquidity event including:

- Trade sale within a particular industry/sector (a few SaaS businesses have scaled up and sold to the bigger sector consolidators).

- Sale to PE as the asset will be big enough and on the radar to be attractive (one of the med-tech businesses acquired by a searcher last year may probably go this way in 4-5 years from now).

- IPO if the searcher has “pushed it” in terms of scale.

16. What is the typical CEO compensation at this point?

There is no one size that fits all - it will be the market rate for the business that the searchers are in (sector and geography).

17. Are the principals full time? Who else is the team? Are they full or part time?

The principals are presently all part-time as that is all that is required during the ramp up phase.

We are supported by an office administrator and an associate (also part-time).

18. How many SF’s have the principals been involved in?

As at the date of this document, we have invested in ten.

We have been involved as mentors or advisors (in small parts) on almost all completed searches to date in Australia.

19. How do you plan to manage the investments?

We anticipate being one of the largest single shareholders in most Search Funds. We also expect to hold board roles either ourselves or through nominees. We will match our skills to the requirement of the searcher and business acquired.

20. Do investors in WayFinder have the opportunity to co-invest and be exposed directly to investments?

Yes.

21. Target returns? What are the key assumptions and evidence for this?

WayFinder is targeting returns of ~20% IRR for the LPs. The underlying assumptions (based on both overseas SF stats and our own experiences here) are:

- Search Investments (average $120k) – 3 out of 4 successfully acquire. 1 out of 4 terminated at full loss

- Average investment value expected at acquisition:

-

- Self-Funded Search - $1.1m

- Funded Search (where we have invested in the search fund) - $1.1

- Average IRR on WayFinder investments and hold period of 29% over 5 years

- Note that the 29% is only on acquisitions, not on incomplete searches.

- Rationale

-

- The 29% is below both the aggregate returns experience overseas including failed searchers and businesses

- Searchers are targeting 35% in order to maximise their own outcomes

- The portfolio of 25 allows sufficient diversification to not be overly exposed to a poor performing investments

- We are being slightly conservative in using a lower return as this is still a first of its kind fund in Australia.

The only other major assumption is that the fund incurs administration and overheads of $4k per month in addition to the management fee paid to the fund manager.

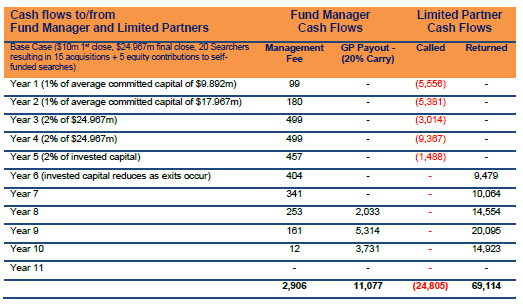

22. Can you show the return arrangement and the 2 and 20% fee in an annual cash flow?

The table below sets out the forecast annual payments to the Fund Manager in our base case (20 Searches -> 15 acquisitions, 5 self-funded acquisitions). Also included are the forecast cash flows to/from the Limited Partners (i.e. investors which also includes ourselves) as it lacks context without it.

The GP payout of the 20% carry is all contingent on the investors getting an 8% compound return first.

Statutory Statement

This offer of scheme interests is available to wholesale clients only. This product listing was vetted by and approved by the product issuer identified above before publishing. Investment Markets (Aust) Pty Ltd AFSL 527875 (IM) is not the issuer of the product.

General Disclaimer

IMPORTANT STATEMENT ABOUT YOUR USE OF THIS SITE

Information on this site is intended for Australian users only.

This site is operated by Investment Markets (Aust) Pty Ltd. (ACN 634 057 248) (IMA, we, us and our), the holder of Australian Financial Services Licence (AFSL) no. 527875. The content is provided solely for information purposes, is not a recommendation or an offer to buy or sell a security, and is not warranted to be correct, complete or accurate. To the extent permitted by law, neither IMA, its affiliates, nor the content providers (such as the issuers of securities who appear on the site) are responsible for any investment decisions, damages or losses resulting from, or related to, the content, data and analyses or their use. The investment products on this site and any statements made about them by their issuers are not vetted, verified or researched by IMA. The presence of an investment product on this site should not be interpreted as an implied endorsement of it by IMA. Certain content provided may constitute a summary or extract of another document such as a Product Disclosure Statement. To the extent any content is general advice, it has been prepared by IMA. Any general advice has been provided without reference to your investment objectives, financial situations or needs. For more information refer to our Financial Services Guide. To obtain advice tailored to your situation, contact a financial advisor. You should consider the advice in light of these matters and, if applicable, the relevant Product Disclosure Statement (or other offer document) before making any decision to invest. Past performance does not necessarily indicate an investment product’s future performance. The content is current as at date of initial publication and may not be current as at your date of viewing. For a more complete understanding of all the terms and conditions of your use of this site click here.