Australian Equity Funds: An Investor's Guide to the Local Share Market

Discover everything you need to know about Australian equity funds, their potential for growth and income, the associated risks, and how to invest in the various types.

What are Australian Equity Funds? & Key Investment Concepts

Australian equity funds are investment vehicles which pool money from investors to buy shares (equities) in companies listed on the Australian Securities Exchange (ASX) or other local companies. They aim to generate capital growth and/or income with a range of strategies such as focusing on large-cap, small-cap, value, or growth stocks.

Australian Equity Funds are popular with local investors because they offer easy, diversified access to Australia's top companies, including well-known names in banking, mining, and retail, without directly buying shares. They provide a convenient way to benefit from the country’s economic fundamentals and dividend streams with franking benefits in investment vehicles which are managed by professionals who handle the research and stock selection.

For many Australian investors, they’re an easy but smart way to grow their wealth with minimal effort on their part. In the words of investment legend Peter Lynch: ‘Equity funds are the perfect solution for people who want to own stocks without doing their own research.’

Before we dive in, here’s a brief definition of some key terms Australian Equity Fund investors need to understand:

- Equity is ‘The value of an asset such as your house or property, less any money owing on it.’ Moneysmart

- Shares are ‘part ownership of a company … also known as shares or stocks.’ Moneysmart

- Equity Finance is ‘An investment where you buy and hold shares in a company or property from which you expect to receive income and capital gains.’ Moneysmart

- Exchange-Traded Funds (ETFs) are ‘managed funds or unit trusts that are quoted and traded on a stock exchange such as the ASX. ETFs generally seek to mimic the performance of a specific index, such as the S&P/ASX 200 index, a currency, such as the USD, or a commodity, such as gold.’ Moneysmart

The Australian Equity Market Landscape

Overview of the Australian Stock Exchange (ASX)

The Australian Securities Exchange (ASX) was formed in 2006 through the merger of the Australian Stock Exchange and Sydney Futures Exchange, and is a leading financial market in the Asia-Pacific region.

Key ASX indices include the S&P/ASX 200, representing the top 200 companies by market capitalisation, the broader S&P/ASX 300, and the broader All Ordinaries, which includes the 500 largest companies listed on the ASX.

The ASX market of listed stocks has a market capitalisation exceeding $A2 trillion, with major sectors including financials, materials, healthcare, and a growing presence in technology and energy.

Key Drivers of the Australian Equity Market

The Australian equities market is influenced by key domestic factors such as GDP growth, interest rates, inflation, and employment levels. Global economic trends, including trade dynamics and geopolitical events, also affect market performance.

Given Australia’s resource-rich economy, commodity prices, particularly for iron ore, coal, and natural gas, heavily impact upon the performance of large sectors like materials and energy.

Additionally, company earnings, dividend policies, and overall investor sentiment play critical roles in shaping market movements and driving investment decisions across various industries.

Historical Performance and Future Outlook

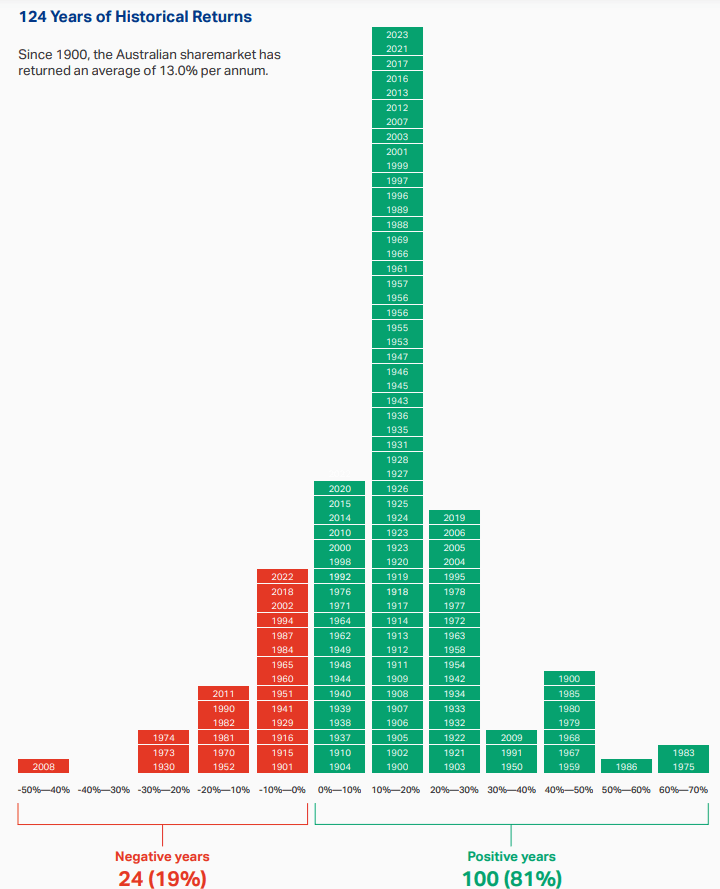

The Australian share market has shown strong long-term growth despite periods of volatility, including the Global Financial Crisis and COVID-19 pandemic.

According to MarketIndex: Australian equities have generated an average return of 13% p.a. since 1900 with 81% of years generating a positive return since then.

Source: Firstlinks

Historically, the Australian market has rebounded from downturns, driven by robust sectors like financials and resources.

Current market conditions reflect cautious optimism amidst global economic uncertainty and inflation pressures. Future growth for Australian equities may be driven by sectors such as renewable energy, technology, and healthcare, though challenges remain.

According to Macquarie Bank: ‘The Australian equity market is expected to deliver moderate returns in 2025 as investors navigate external geopolitical pressures and domestic challenges.’

A long-term perspective is essential with equity investing to weather short-term fluctuations and capitalise on the benefits of compounding returns.

Types of Australian Equity Funds

Australian equity funds cater to various investment strategies, risk appetites, and access methods. Here are the main types of funds:

Managed Funds (Unlisted)

Managed funds pool money from multiple investors to invest in a diversified portfolio of assets, managed by professional fund managers. They suit investors with a long-term investment horizon and varying risk appetites depending on the fund type (e.g. conservative, balanced, or growth).

Investors can access managed funds through financial advisors, online platforms, or directly from fund providers, making them a convenient option for those seeking diversification and professional management.

For example, the ELMRI ANZ Conviction Fund invests in Australian and New Zealand mid and large cap companies that are included in the S&P/ASX 300 Index.

Exchange-Traded Funds (ETFs)

Exchange Traded Funds (ETFs) are passive investment funds traded on the ASX like shares, offering exposure to a basket of assets. In the words of the ASX: ‘Investors mostly use ETFs to achieve the return of an underlying index through a diversified portfolio of securities.’

ETFs provide benefits such as liquidity, low fees, and transparency. They suit investors with varied risk appetites seeking diversification and ease of access.

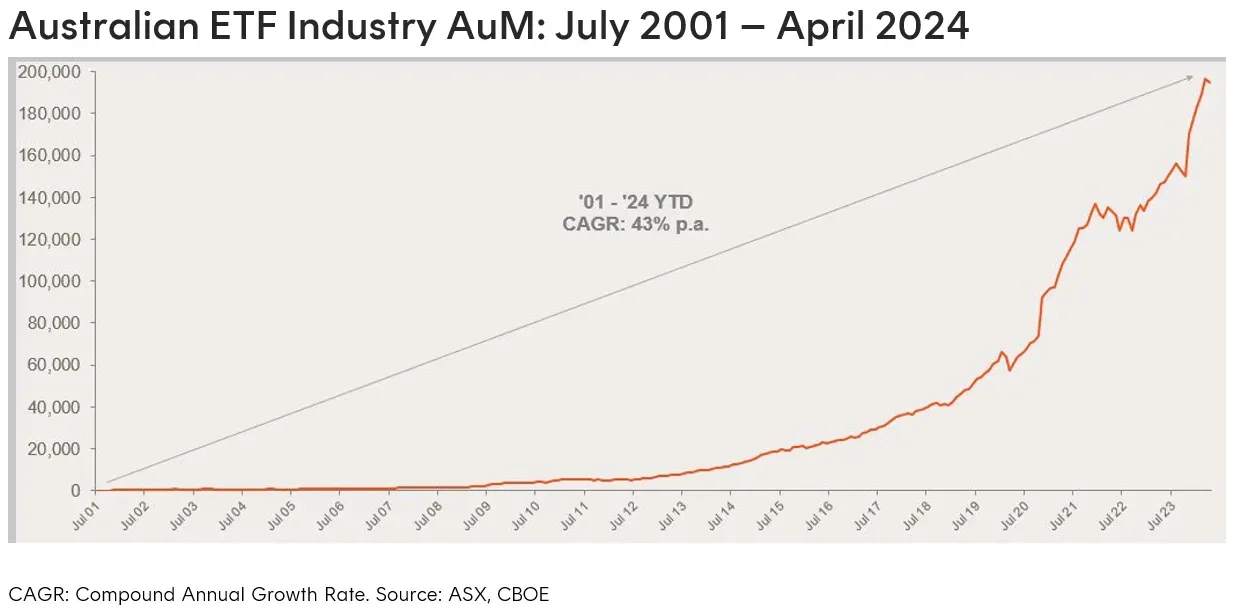

In recognition of these benefits, the Australian ETF industry’s assets under management (AuM) have been growing at 43% p.a. since 2001—as shown below.

Source: Betashares

For example, BetaShares Australian Dividend Harvester Fund generates income-driven returns through a diversified portfolio of Australian shares.

Listed Investment Companies (LICs) & Listed Investment Trusts (LITs)

Listed Investment Trusts (LITs) and Listed Investment Companies (LICs) are closed-end funds which are traded on the ASX like shares.

They pool investor money to invest in a range of assets, including Australian equities, and aim for dividends and long-term capital growth. LICs and LITs are generally suited to moderate to higher risk investors. They offer diversification and income generation potential, and can be bought like shares via a broker.

According to the ASX: ‘Unlike ETFs that usually aim to provide an index return, LIC managers aim to outperform the benchmark index against which their fund is compared.’

For example, Flagship Investments Ltd is a LIC providing investors with access to a portfolio of Australian growth companies.

Tip: LIC and LIT share prices can differ from their Net Tangible Assets (NTA). They often trade at a premium or discount.

Style-Specific Funds - Growth, Value, Income & Dividend

Style-specific Australian equity funds focus on distinct investment strategies such as:

- Growth funds target companies with high earnings potential;

- Value funds seek undervalued stocks;

- Income funds prioritise high-yielding shares, and often leverage the associated franking credits to generate tax-effective income.

These distinct types of managed funds suit varying risk appetites and can be purchased through financial advisors, online platforms, or directly from fund providers. For example, growth funds generally suit higher risk investors, while income funds tend to suit moderate risk investors.

For example, Hamilton12 Australian Shares Income Fund is an income-focused fund which invests in Australian equities with high franked dividend yields.

Size-Specific Funds: Large-Cap, Mid-Cap, Small-Cap

Size-specific Australian equity funds invest in companies differentiated by their market capitalisation: large-cap (e.g. S&P/ASX 50), mid-cap, or small-cap:

- Large-cap funds generally offer stability and lower volatility, suiting conservative investors;

- Mid-cap funds balance growth and risk;

- Small-cap funds aim for high growth but carry greater risk, appealing to more aggressive investors.

These various types of funds are accessible via managed funds or ETFs on investment platforms or through brokers, and allow investors to tailor their exposure to their risk and return profiles.

For example, Perpetual Smaller Companies Fund aims to generate long-term capital growth and income by investing in companies outside the S&P/ASX 50 Index.

Thematic & Sector-Specific ETFs

Thematic and sector-specific Australian ETFs offer targeted exposure to trends or industries, such as gold, crypto (Bitcoin), AI, technology, mining, property (REITs), and ethical/sustainable investing.

These ETFs allow investors to capitalise on specific themes but often carry higher volatility and risk due to their focused nature. They’re best suited to growth-focused investors and typically form a smaller, satellite portion of a diversified portfolio. Investors can access them via trading platforms or brokers on the ASX.

For example, Global X Australia ex Financials & Resources ETF is a targeted ETF which excludes ASX 100 companies in the financial (including REITs), basic material, and energy sectors.

ETFs vs. Managed Funds: Key Differences for Australian Investors

Here’s a comparison between ETFs and managed funds to help investors choose the right vehicle for them:

Structure and Trading

ETFs are open-end funds which are traded on stock exchanges, allowing investors to buy and sell throughout the trading day at market prices. This intraday trading provides real-time pricing and liquidity.

In contrast, managed funds can be either open-end or closed-end, and are typically not traded on exchanges. Open-end managed funds are priced once daily at the net asset value (NAV), while closed-end funds have a fixed number of shares and trade on exchanges, but their market prices can fluctuate based on supply and demand, potentially trading at a premium or discount to NAV.

ETFs and managed funds both share the benefit of diversification. In the words of Vanguard: ‘Both ETFs and managed funds have in-built diversification. They pool together money from many people and invest across hundreds, and sometimes thousands, of individual shares, bonds, and other investment securities.’

Fees and Costs

ETFs typically have lower fees and Management Expense Ratios (MERs) than managed funds but incur brokerage fees when bought or sold.

Managed funds usually charge higher MERs and management fees reflecting the higher costs of active management.

Transparency

ETFs offer greater transparency than most managed funds, typically disclosing their full portfolio holdings daily, allowing investors to see exactly what they own.

In contrast, managed funds usually disclose their holdings quarterly or semi-annually, providing less frequent updates and making it harder for investors to track a fund’s exact investments in real time.

Tax Efficiency

ETFs are often more tax-efficient than managed funds due to their unique creation and redemption process, which allows in-kind transfers of securities. This can minimise their capital gains tax liabilities.

Managed funds, by contrast, must sell assets to meet redemptions, potentially triggering capital gains that are passed on to all investors.

Accessibility & Minimum Investments

Managed funds often require higher minimum investments and may be less accessible as they are typically purchased through financial advisors or platforms.

In contrast, ETFs are more accessible as they traded like stocks on exchanges and usually have lower minimum investment requirements.

Key Benefits of Investing in Australian Equity Funds

Potential for Capital Growth

Australian equity funds offer long-term capital growth potential as they invest in their fund holdings with the expectation of outperformance.

Investors who invest regularly in these funds can benefit from the compounding effect, whereby reinvested returns generate additional returns over extended periods and market cycles.

Dividend Income and Franking Credits

Australian shares often provide attractive dividend income, a key component of total equity fund returns, particularly for income-focused funds.

Many Australian dividends come with franking credits, which can reduce the tax paid by Australian residents. These credits reflect tax already paid by companies, making income from these equities more tax-effective for local investors.

Diversification

Equity funds spread investments across a broad range of companies and sectors, offering instant diversification. This reduces the impact of poor performance by any single stock, helping to manage risk while maintaining exposure to growth opportunities across the Australian economy.

Moneysmart explains why diversification is so important: ‘Diversification is your best defence against a single investment failing or one asset class performing poorly (for example, the share market falling or one fund manager failing).’

Professional Management & Systematic Approach

Active equity funds offer professional expertise in stock selection and market timing with the objective of outperforming the market.

Passive funds (ETFs) use a systematic, rules-based approach to track an index, offering diversification, transparency, and low-cost exposure to the Australian market.

Accessibility and Liquidity

Australian equity funds, especially ETFs, are easily accessible through online platforms and brokers. Many have low minimum investment requirements. ETFs are particularly liquid, allowing investors to buy or sell units on the ASX throughout the trading day at market prices.

Risks and Challenges of Australian Equity Funds

While offering benefits, investing in Australian equity funds involves inherent risks, namely:

Market Risk (Systematic Risk)

Market risk refers to the risk of economic, geopolitical, or other events causing overall market declines. Even well-diversified equity funds are vulnerable to market downturns which affect all sectors and companies simultaneously.

Company-Specific Risk (Unsystematic Risk)

Company-specific risk arises from poor performance or mismanagement of individual companies within a fund. Unlike market risk, it can be reduced through diversification but may still affect returns if key holdings underperform significantly.

Economic Risk

Economic risk factors like rising inflation, interest rate hikes, or recessions can impact company earnings and investor confidence, potentially reducing equity values and fund returns.

Sector Concentration Risk

The Australian market is heavily skewed toward financials and materials. If these sectors underperform, funds with high exposure may suffer, even if other sectors perform well, limiting diversification benefits.

Fund Manager Risk (for active funds)

Active fund performance depends on manager decisions. Poor stock selection or strategy may lead to underperformance compared to benchmarks or similar funds, affecting investor returns and confidence.

Liquidity Risk

Some unlisted or niche funds may be hard to buy or sell quickly without affecting prices. While ETFs and LICs are typically liquid, unusual market conditions or low trading volumes can sometimes limit liquidity.

Tracking Error (for passive/ETFs)

Tracking error occurs when a passive fund doesn’t exactly mirror its benchmark index due to fees, rebalancing lags, or sampling methods. This can lead to small, unintended performance differences.

Currency Risk (for ETFs investing overseas, even if ASX-listed)

If an ETF holds foreign assets and is unhedged, currency fluctuations can impact returns. For example, a weakening AUD benefits Australian investors, but a strengthening AUD can erode offshore gains significantly.

How to Invest in Australian Equity Funds

Here are the practical steps toward investing in Australian Equity Funds:

Choosing a Share Trading Platform or Broker

To invest in ETFs or LICs, choose a platform offering low fees, strong research tools, and user-friendly design.

Popular Australian brokers include CommSec, SelfWealth, and Stake.

Compare features using ASIC’s Moneysmart comparison tools to find the right fit for your investment needs.

Investing Directly via Fund Managers

Unlisted managed funds can be accessed directly through fund managers like Perpetual. You’ll typically need to complete an online application and meet a minimum investment (often $5,000+).

ASIC advises reviewing Product Disclosure Statements (PDS) to understand fees, risks, and fund objectives before investing.

Using Investment Platforms (Wraps, Master Trusts)

Wraps and master trusts provide access to a wide range of managed funds under one account. Platforms like HUB24 or Netwealth offer consolidated reporting and easier portfolio management.

ASIC recommends understanding platform fees, investment menus, and adviser involvement when using these services.

Through a Financial Advisor

A licensed financial advisor can tailor Australian equity fund choices to your goals, risk tolerance, and financial situation. Advisors often access wholesale funds and handle all paperwork.

ASIC stresses the importance of checking adviser credentials via the Financial Advisers Register before seeking advice.

Via Superannuation

Super funds offer Australian equity fund options via pre-mixed or custom investment choices.

Self-managed super funds (SMSFs) provide direct access to ETFs and equity funds.

ASIC recommends reviewing fees, performance, and the asset allocations of your super to align with your long-term retirement goals.

Practical Considerations for Investing

Decide between lump-sum or dollar-cost averaging (e.g. $500/month into an ETF). Many brokers allow automatic ETF investing. Factor in brokerage, management fees, and bid/ask spreads.

ASIC suggests setting clear goals and using budgeting tools to align regular investments with financial capacity.

Tax Implications of Australian Equity Funds

Understanding the tax implications of Australian equity funds is essential for maximising returns. Here’s a concise overview:

Dividend Income and Franking Credits

Australian companies often distribute dividends with franking credits.

According to the ATO: ‘Franking credits arise for shareholders when certain Australian-resident companies pay income tax on their taxable income and distribute their after-tax profits by way of franked dividends.’

For Australian residents, these credits can reduce their tax liabilities. For example, a $7,000 fully franked dividend comes with $3,000 in franking credits, resulting in $10,000 of effective income. If your tax rate is below the company tax rate, you may receive a refund.

Tax Treatment of Fund Types

For ETF and LIC investors, dividends are taxed when received, while capital gains from sales incur Capital Gains Tax (CGT) with a 50% discount for holdings over 12 months.

For managed fund investors, distributions may include dividends, interest, and capital gains, each with distinct tax treatments. Annual capital gains distributions can also trigger CGT events.

Tax Considerations for Non-Residents

Non-residents typically cannot claim franking credit refunds and may face withholding tax on dividends.

Building and Managing Your Australian Equity Fund Portfolio

Here are the six main foundational strategies for constructing a portfolio of Australian Equity Funds:

Defining Your Investment Goals and Risk Tolerance

Start by setting clear investment goals: growth, income, or capital preservation. Understand how much risk you’re comfortable with. Aligning your equity fund choices to your goals and tolerance helps you stay invested through market ups and downs.

Asset Allocation within Australian Equities

Diversifying across styles and market capitalisations generally enhances portfolio resilience across market cycles while reducing volatility.

Core and Satellite Approach

Building a stable ‘core’ portfolio using broad-market funds like ASX 200 or ASX 300 ETFs, then complementing it with targeted ‘satellite’ allocations (e.g. sector or thematic funds), can balance long-term consistency with active opportunity-seeking.

Understanding ETF Overlap

Overlapping holdings, common in Australian equity ETFs, can unintentionally skew portfolio concentration.

Use ETF comparison tools and overlap calculators, available online, to ensure true diversification and avoid redundancy.

Rebalancing Your Portfolio

Rebalancing involves adjusting your holdings back to target weights, typically annually or semi-annually. It controls risk, locks in gains from outperformers, and maintains alignment with your strategy as markets shift.

As Betashares explain: ‘The primary objective of portfolio rebalancing is to safeguard the investor from being overly exposed to undesirable risks.’

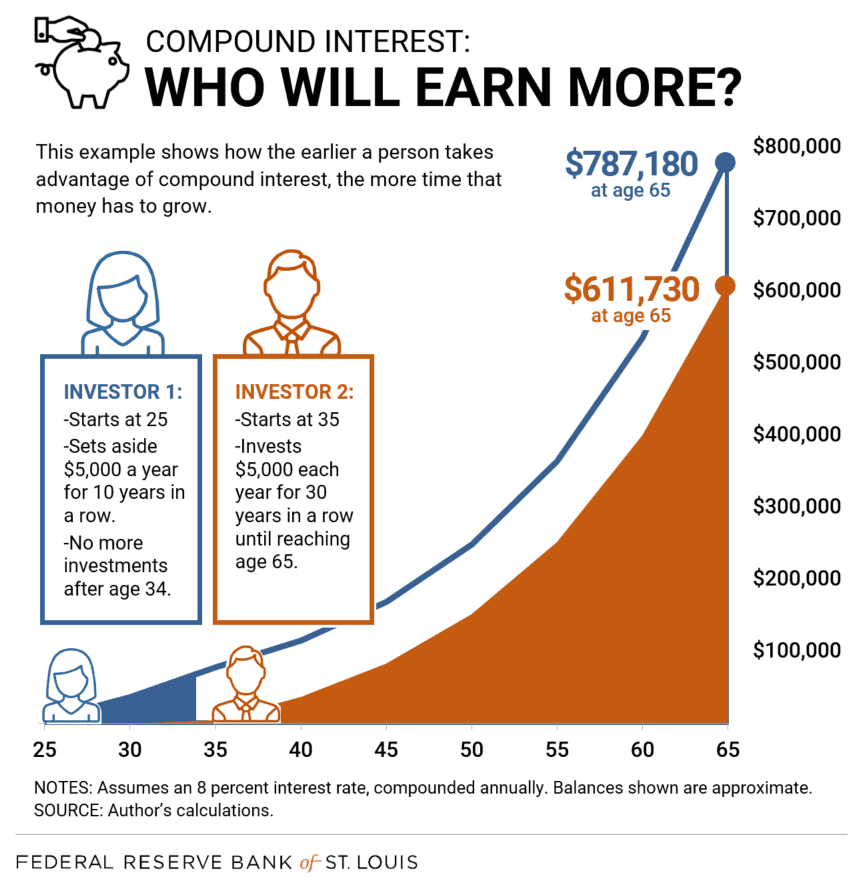

The Power of Compounding & A Long-Term Perspective

Reinvesting dividends and capital gains allows earnings to generate more earnings. Over time, this compounding significantly boosts total returns. Staying invested and patient is the key to maximising the benefits of long-term compounding.

For example, an investor who starts investing $5000 p.a. in equity funds at between the ages of 25 and 35 will have amassed nearly $800,000 by the time she is 65—as shown below.

Source: Federal Reserve Bank of St Louis

Monitoring Your Australian Equity Fund Investments

After investing, regular monitoring ensures your Australian equity funds align with your goals. Here’s how to do it effectively:

Key Performance Indicators (KPIs)

Track the total return of your equity funds: capital gains plus dividends. Compare performance to benchmarks like the S&P/ASX 200. Assess fund volatility as a key risk measure.

As MoneySmart notes: ‘comparing returns with similar investments or an index helps you judge performance realistically.’

Tools for Monitoring

Use fund manager reports, ASX announcements, and portfolio tracking tools to monitor performance. Staying informed helps you act early if issues arise.

MoneySmart advises: ‘Read the fund’s regular reports to check how your investment is performing and if it’s meeting your expectations.’

When to Review and Adjust

Review periodically: quarterly or annually. Rebalance if allocations shift, and switch funds if long-term underperformance occurs.

MoneySmart suggests: ‘If a fund consistently performs poorly compared to others, it may be time to look at other options better suited to your goals.’

How to Compare and Select Australian Equity Funds

Here are the eight key factors for informed decision-making about investing in Australian Equity Funds:

Investment Objectives and Strategy

Ensure the fund’s Product Disclosure Statement (PDS) aligns with your goals.

MoneySmart advises: ‘Understand the fund’s investment strategy—whether it’s passive, active, or benchmark-tracking—so it fits your time frame and risk profile.’

Performance History, Benchmarking, and Top Performers

Morningstar highlights that: ‘past performance isn’t everything, but consistent outperformance against a benchmark over time is a positive signal.’

Use 3–5 year returns to assess fund resilience, especially among top-performing ETFs or managed funds.

Fees and Costs (MER, Brokerage, Spreads)

As Canstar notes: ‘Even small differences in fees can make a big impact over time.’

Compare the Management Expense Ratio (MER), management fees, brokerage, and spreads.

Tip: Low-cost ETFs often provide the most competitive returns net of fees.

Fund Manager and Provider Reputation

Lonsec recommends considering ‘manager tenure, asset base, and investment process.’

Evaluate trusted managers for fund stability, transparency, and proven track records in delivering outcomes aligned with their mandates.

Holdings, Diversification, and Sector Allocation

Morningstar suggests reviewing fund fact sheets for holdings, saying: ‘broad diversification reduces risk.’

Check the number of fund holdings, top exposures, and sector weightings to ensure a fund is not overly concentrated in banks, miners, or a single industry.

Distributions: Dividends, Franking Credits, and Tax Effectiveness

Assess distribution yield, franking credits, and the availability of dividend reinvestment plans (DRPs).

As MoneySmart explains: ‘Reinvesting income can boost long-term returns, and franking credits may enhance after-tax income for Australian investors.’

Ethical and ESG Considerations

Ethical investing is growing in both managed funds and ETFs.

As Canstar highlights: ‘Ethical ETFs apply screening processes to exclude companies based on ESG factors.’

Look for funds aligned with your values using third-party ratings or Ethical Advisers’ Co-op listings.

Tools for Comparison

Use trusted fund comparison tools like InvestmentMarkets, Morningstar, Canstar, or MoneySmart. These platforms make it easier to filter funds by category, risk, and fees.

‘Comparison websites help you analyse features, costs, and performance,’ says MoneySmart.

Are Australian Equity Funds Right for Your Portfolio?

Australian equity funds offer an accessible way to participate in the growth potential and income generation of the local share market. They provide diversification and professional oversight, suiting investors with various goals, from long-term capital appreciation to regular income streams. However, like all investments, they come with risks, particularly exposure to market volatility.

Carefully assess your investment timeframe, risk tolerance, and financial objectives. By understanding the different types of funds, their benefits, risks, and how to compare them, you can make an informed decision on whether Australian equity funds align with your overall investment strategy and contribute to building your wealth.

Head of Content (CFA)

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.

& Spatium Capital (Investment Manager)")

/ Quest Asset Partners Pty Ltd (Investment Manager)")

/ APSEC Funds Management Pty Ltd (Investment Manager)")