The Structural Rise of Commodity ETFs

The rise of commodity ETFs reflects a broader transformation in financial markets. Historically, commodities were difficult to access. Exposure required futures contracts, physical ownership, or investment in resource companies, each with its own complexity and limitations.

Today, that structure has fundamentally changed.

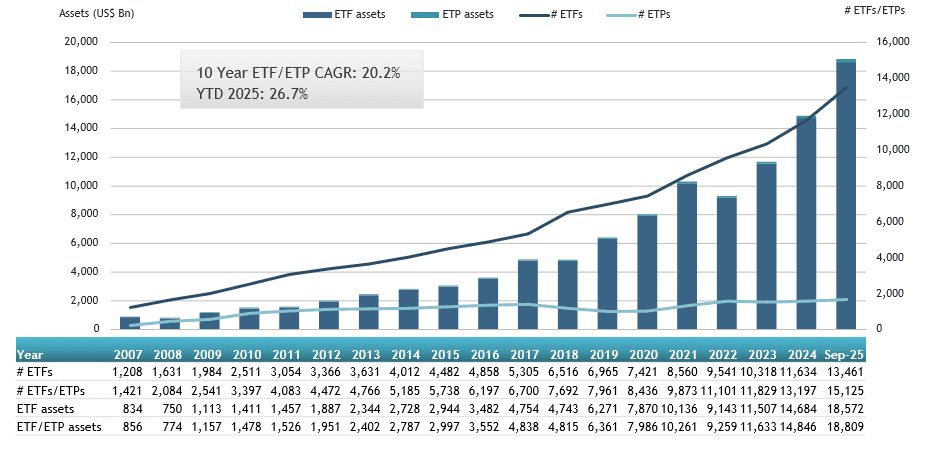

The ETFGI reports that global ETF assets have expanded rapidly, driven by investor demand for transparent, low-cost access to diversified asset classes. Commodity ETFs, while smaller than equity ETFs, have seen significant inflows during periods of inflation and market stress.

Source: ETFGI

This growth is not incidental. It is rooted in three structural drivers.

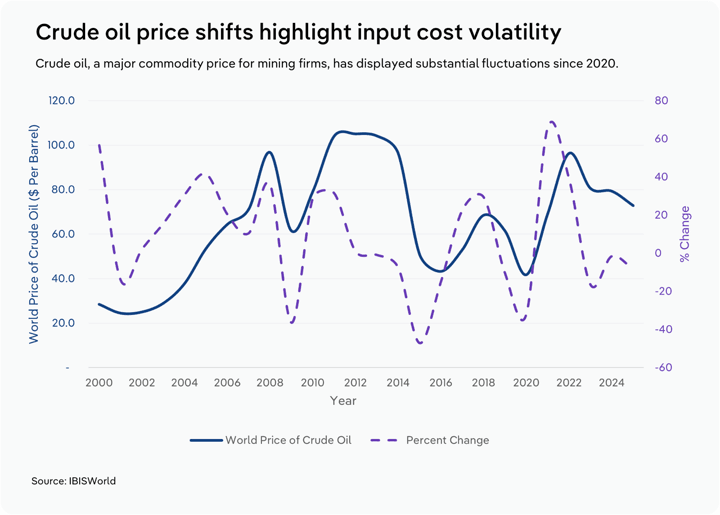

First, the nature of inflation has changed. The inflation shock of 2021 to 2023 was driven not only by demand but by supply constraints, including energy disruptions, geopolitical tensions, and supply chain bottlenecks. Commodities sit at the centre of these dynamics.

Source: IBISWorld

Second, traditional diversification has become less reliable. The simultaneous decline of equities and bonds in 2022 highlighted the limitations of conventional portfolio construction. Investors are increasingly seeking assets with different underlying drivers, and commodities provide precisely that.

Third, access has improved dramatically. ETFs have transformed commodities from a specialist asset class into a mainstream investment option.

Vanguard has noted that ETFs combine ‘the diversification benefits of managed funds with the flexibility of trading like shares’, a characteristic that is particularly valuable in commodity markets, where pricing can be volatile and timing matters.

For Australian investors, the ASX now offers a growing range of commodity ETFs, many of which are curated within the InvestmentMarkets platform.

Understanding Commodity ETFs: Structure, Function, and Behaviour

Commodity ETFs are often presented as simple instruments that track the price of commodities. While this description is technically accurate, it is insufficient for investors seeking to understand how these products behave in real portfolios.

In practice, commodity ETFs are not a single homogenous category. They are a collection of structurally distinct vehicles, each with different return drivers, risks, and portfolio implications. The differences between these structures are not academic. They materially influence outcomes, particularly over longer investment horizons.

Understanding these distinctions is critical. Two ETFs may appear similar on the surface, both labelled commodity ETFs, yet deliver very different results depending on their construction.

At a fundamental level, commodity ETFs can be divided into three primary structural types: physical, futures-based, and equity-linked.

Each reflects a different approach to solving the same problem, how to provide investable exposure to real-world commodities.

Physical Commodity ETFs: Direct Exposure to Scarcity and Store of Value

Physical commodity ETFs represent the most intuitive form of commodity exposure. These funds hold the underlying asset directly, typically in the form of securely stored reserves.

This structure is most commonly associated with gold, reflecting the unique characteristics of the metal. Unlike energy or agricultural commodities, gold is durable, easily stored, and widely accepted as a store of value.

The World Gold Council notes that gold’s role within portfolios is driven by its dual identity as both a commodity and a monetary asset. It is not consumed in the same way as oil or wheat. Instead, it is accumulated, held, and traded as a form of financial insurance.

This distinction matters.

A physical gold ETF provides exposure that is closely aligned with the spot price of gold. There is minimal structural interference between the investor and the underlying asset. This leads to relatively low tracking error and high transparency.

However, even within this simplicity, there are important nuances.

Storage costs, insurance, and operational expenses are embedded within the ETF’s fee structure. While these costs are typically modest, they represent a persistent drag on returns over time. In addition, physical ETFs do not generate income. Their return is entirely dependent on price appreciation.

For investors, this creates a specific use case.

Physical commodity ETFs are most appropriately viewed as portfolio stabilisers and inflation hedges, rather than return-generating assets. Their value tends to emerge during periods of monetary instability, currency debasement, or geopolitical stress, environments in which traditional financial assets may struggle.

Within the InvestmentMarkets ecosystem, these ETFs often serve as the entry point for investors seeking commodity exposure, particularly those focused on capital preservation and diversification.

Futures-Based Commodity ETFs: Accessing Complex Markets Through Financial Engineering

While physical ETFs dominate precious metals, most other commodities cannot be held directly in a practical or cost-effective way. Oil, natural gas, and agricultural products are perishable, expensive to store, or logistically complex.

To solve this, ETFs use futures contracts.

A futures-based commodity ETF does not own the commodity itself. Instead, it holds contracts that provide exposure to the future price of that commodity. These contracts are rolled periodically as they approach expiry, creating a continuous exposure profile.

This structure introduces a layer of complexity that is often underestimated.

The CME Group explains that futures markets can exist in two primary states: contango and backwardation.

In a contango market, future prices are higher than spot prices. This creates a negative roll yield, meaning that as contracts are rolled forward, the ETF effectively sells low and buys high. Over time, this can erode returns, even if the spot price of the commodity remains stable.

In backwardation, the opposite occurs. Future prices are lower than spot prices, creating a positive roll yield that can enhance returns.

These dynamics are not theoretical. They have had a profound impact on commodity ETF performance, particularly in energy markets.

For example, during periods of oil oversupply, futures curves have frequently moved into contango. Investors in oil ETFs during these periods have experienced returns that diverged significantly from headline oil price movements.

Investors often assume that commodity ETFs provide a direct reflection of spot prices. In reality, futures-based ETFs provide exposure to a combination of spot prices, futures curves, and rolling mechanics.

From a portfolio construction perspective, this makes them more suitable for:

- Tactical allocations;

- Shorter-term positioning;

- Macro-driven investment strategies.

They are less appropriate as long-term ‘buy and hold’ exposure without active monitoring.

Equity-Based Commodity ETFs: The Illusion of Direct Exposure

A third category of commodity ETFs, equity-based ETFs, provides exposure not to commodities themselves, but to the companies that produce them.

These ETFs invest in:

- Mining companies;

- Energy producers;

- Resource extraction firms.

At first glance, this may appear equivalent to commodity exposure. In practice, it is fundamentally different.

The performance of commodity-producing companies is influenced by a wide range of factors beyond commodity prices, including:

- Operational efficiency;

- Capital allocation decisions;

- Cost structures;

- Regulatory environments;

- Equity market sentiment.

This creates a divergence between commodity prices and equity returns.

For example, during periods of rising commodity prices, mining companies may underperform if cost inflation erodes margins. Conversely, companies may outperform commodity prices due to operational improvements or market re-rating.

The International Monetary Fund has highlighted that commodity-linked equities often exhibit higher volatility than the underlying commodities themselves, reflecting their dual exposure to both commodity cycles and equity market dynamics.

For investors, the implication is clear.

Equity-based commodity ETFs should not be treated as substitutes for direct commodity exposure. They are, in effect, a hybrid asset class, combining elements of commodities and equities.

Within portfolios, they are typically used for:

- Growth-oriented commodity exposure;

- Leveraged participation in commodity cycles;

- Integration with broader equity allocations.

The Behaviour of Commodity ETFs: Beyond Simple Price Tracking

To understand commodity ETFs fully, it is necessary to move beyond structure and examine behaviour.

Unlike equities, which are driven by earnings, or bonds, which are driven by interest rates, commodities are driven by real-world supply and demand dynamics. This gives them a unique position within portfolios.

However, it also makes their behaviour more complex and, at times, counterintuitive.

Inflation Sensitivity and Real Asset Characteristics

Commodity ETFs are often described as inflation hedges, and this characterisation is broadly supported by historical data.

The Reserve Bank of Australia has observed that commodity prices tend to rise during periods of elevated inflation, reflecting their role as inputs into the production of goods and services.

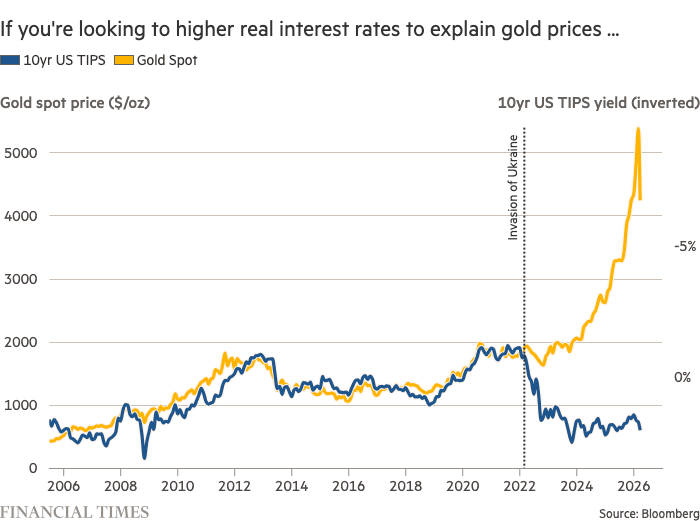

Gold, in particular, has historically, but not always, demonstrated a strong relationship with real interest rates. When real yields fall or become negative, gold prices have often risen, reflecting its role as a store of value.

Source: Financial Times

However, not all commodities behave identically.

Industrial commodities are influenced by both inflation and growth, while agricultural commodities are affected by weather patterns, supply shocks, and seasonal dynamics.

This diversity reinforces the importance of broad commodity exposure rather than reliance on a single asset.

Cyclicality and Economic Regimes

Commodity markets are inherently cyclical.

Periods of strong economic growth drive increased demand for energy, metals, and raw materials. This pushes prices higher, often leading to what is commonly described as a commodity supercycle.

Conversely, economic slowdowns reduce demand, leading to price declines.

The International Energy Agency has repeatedly highlighted how shifts in global growth expectations influence energy markets, particularly oil.

For investors, this cyclical behaviour creates both opportunity and risk.

Commodity ETFs can deliver strong returns during expansionary phases, but they can also experience significant volatility during downturns. This makes timing and portfolio context critical.

Diversification Properties and Correlation Dynamics

One of the primary reasons investors allocate to commodity ETFs is diversification.

Historically, commodities have exhibited low correlation with equities and bonds. This means they can provide portfolio benefits when traditional assets underperform.

However, this relationship is not stable.

During certain market regimes, particularly those driven by inflation shocks, correlations can shift. The simultaneous decline of equities and bonds in 2022 demonstrated that traditional diversification assumptions can break down.

Commodities, by contrast, performed relatively strongly during this period, reinforcing their role as alternative diversifiers.

The CFA Institute emphasises that diversification must be considered dynamically, with asset class relationships changing over time.

Currency Effects for Australian Investors

For Australian investors, commodity ETF returns are influenced not only by commodity prices but also by currency movements.

Most commodities are priced in US dollars. As a result:

- A weaker Australian dollar enhances returns;

- A stronger Australian dollar reduces returns.

This introduces an additional layer of variability.

Currency effects can amplify or offset commodity price movements, depending on the direction of exchange rates.

For investors using InvestmentMarkets, this highlights the importance of understanding whether an ETF is:

- Currency hedged, or

- Unhedged.

It’s also important to focus on how this aligns with investors’ broader portfolio exposures.

Putting Structure and Behaviour Together

The combination of structural differences and behavioural drivers explains why commodity ETFs cannot be treated as a simple asset class.

Their performance is shaped by:

- ETF structure;

- Futures market dynamics;

- Macroeconomic conditions;

- Geopolitical events;

- Currency movements.

For investors, this complexity is both a challenge and an opportunity.

Those who understand these dynamics can use commodity ETFs to enhance portfolio resilience, improve diversification, and position for macroeconomic trends.

Those who do not may experience outcomes that diverge significantly from expectations.

The Commodity ETF Landscape: Categories, Comparison, and Portfolio Integration

For Australian investors, the critical insight is that commodity ETFs are not a single, uniform asset class. They are a set of distinct instruments, each designed to capture different aspects of the global commodity complex.

This distinction is not semantic. It is the difference between using commodities effectively as a portfolio tool, or misallocating capital based on incomplete understanding.

The InvestmentMarkets commodities ETFs universe is best understood not as a list of interchangeable products, but as a curated entry point into multiple forms of commodity exposure, each with a specific role in portfolio construction.

At a structural level, the commodity ETF universe reflects the underlying reality of commodity markets themselves. Commodities are not driven by a single economic force. They sit at the intersection of inflation, industrial production, geopolitics, and currency movements. As a result, the ETFs that track them must take different forms.

Understanding these forms, and how to compare them meaningfully, is essential for any investor seeking to integrate commodities into a portfolio in a deliberate and informed way.

The Evolution of Commodity Exposure: From Single Assets to Multi-Dimensional Allocations

Historically, commodity investing for Australian investors was synonymous with two approaches.

The first was direct exposure to gold, typically held as a defensive asset.

The second was indirect exposure through equities, particularly large resource companies listed on the ASX.

Both approaches remain relevant, but neither fully captures the breadth of the modern commodity opportunity set.

The expansion of exchange traded funds has changed this.

Commodity ETFs now provide access to a much broader spectrum of exposures, allowing investors to move beyond single-commodity or single-sector positions and instead engage with commodities as a diversified and dynamic asset class.

The International Monetary Fund has noted that commodities play a central role in global economic cycles, acting both as inputs into production and as indicators of economic momentum. This dual role explains why different commodities behave differently across market regimes, and why a single, undifferentiated allocation is rarely sufficient.

Within InvestmentMarkets, this complexity is reflected in the range of available ETFs. While they may be grouped under a single category for navigation purposes, their underlying exposures and behaviours differ materially. The practical implication for investors is that selecting a commodity ETF is not simply a matter of choosing a product. It is a matter of selecting a specific type of economic exposure.

Interpreting Commodity ETF Categories Through an Investor Lens

Rather than viewing commodity ETF categories as static classifications, it is more useful to interpret them through the lens of what problem they are solving within a portfolio.

Gold and Precious Metals: Monetary Assets in a Financial System

Gold occupies a unique position among commodities. It is both a physical asset and a financial instrument, with a history that predates modern capital markets. Unlike industrial commodities, gold is not consumed in the production process. Its value is derived from its role as a store of wealth.

The World Gold Council has consistently emphasised that gold’s performance is closely linked to real interest rates and currency dynamics. When real yields fall, or when confidence in fiat currencies weakens, gold tends to appreciate.

For Australian investors, this distinction is critical. A gold ETF is not simply a commodity investment. It is, in many respects, an alternative monetary asset.

For example, Betashares Gold Bullion ETF (ASX: QAU) is backed by physical gold bullion and aims to track the performance of the price of gold, hedged for currency movements in the AUD/USD exchange rate.

Within a portfolio, gold ETFs often serve as a form of insurance. They do not generate income, and they may underperform during periods of strong economic growth. However, their value becomes apparent during periods of stress, when other assets are under pressure.

This explains why gold ETFs are frequently used as a foundational allocation within commodity exposure, particularly for SMSFs and investors focused on capital preservation.

Broad Commodity Exposure: Capturing the Global Economic Cycle

While gold is driven primarily by monetary conditions, most other commodities are tied to economic activity.

Broad commodity ETFs are designed to capture this broader dynamic. They provide exposure across multiple sectors, including energy, metals, and agriculture.

This diversification is not incidental. It reflects the reality that different commodities respond to different drivers.

Energy markets are influenced by geopolitical events and supply constraints. Industrial metals are driven by infrastructure spending and manufacturing activity. Agricultural commodities are affected by weather patterns and seasonal cycles.

The International Energy Agency has highlighted the extent to which energy markets alone can be reshaped by geopolitical developments, from production decisions by major exporters to disruptions in supply chains.

By combining multiple commodities within a single structure, broad commodity ETFs smooth some of this volatility while maintaining exposure to the overall direction of global demand.

For example, Global X Bloomberg Commodity Complex ETF (ASX: BCOM) invests in a highly liquid, broad-based basket of commodities, including energy, grains, precious metals, industrial metals, softs and livestock.

For investors, these types of ETF create a more balanced form of exposure. Rather than relying on a single commodity cycle, they gain access to a range of economic drivers. Within portfolios, these ETFs are often used as macro hedges, particularly in environments where inflation is rising or economic conditions are uncertain.

Energy and Resources: Cyclical Exposure to Global Growth

At the more concentrated end of the spectrum are energy and resource-focused ETFs. These products provide targeted exposure to sectors that are highly sensitive to economic cycles.

Investors searching energy ETFs are typically seeking to capitalise on specific market conditions. Energy markets, in particular, are characterised by sharp price movements driven by supply disruptions, geopolitical tensions, and changes in demand.

The behaviour of these ETFs reflects this reality. They tend to perform strongly during periods of economic expansion, when demand for energy and raw materials increases. However, they can also experience significant declines during downturns, when demand weakens.

This makes them fundamentally different from diversified commodity ETFs.

Where broad exposure provides balance, energy-focused exposure provides concentration and sensitivity. It is a more tactical allocation, suited to investors who have a view on the direction of global growth or commodity markets.

For example, Betashares Global Energy Companies ETF (ASX: FUEL) tracks the performance of an index (before fees and expenses) that comprises the largest global energy companies (ex-Australia), hedged into Australian dollars.

In short, these types of ETF are best understood as tools for expressing macroeconomic views, rather than as core holdings.

Commodity-Linked Equities: The Intersection of Commodities and Capital Markets

A further layer of complexity is introduced by commodity-linked equity ETFs. These products invest in companies involved in the production of commodities, rather than the commodities themselves.

This distinction is often overlooked.

The performance of these ETFs is influenced not only by commodity prices, but also by corporate factors such as management decisions, cost structures, and capital allocation. This creates a divergence between commodity prices and equity returns.

The International Monetary Fund has noted that commodity-linked equities can amplify commodity cycles, delivering higher returns during upswings but also experiencing greater volatility during downturns.

For example, Global X Physical Precious Metals Basket Structured (ASX: ETPMPM) offers a low-cost and secure way to access physical gold, silver, platinum, and palladium.

Within portfolios, these ETFs occupy a hybrid role. They provide exposure to commodities, but through the lens of equity markets. As a result, they are typically used to enhance returns, rather than to provide diversification.

Moving Beyond Labels: How to Compare Commodity ETFs Properly

For investors, the key challenge is not identifying available ETFs, but comparing them in a way that reflects their underlying characteristics.

A superficial comparison based on recent performance is rarely sufficient. Commodity ETFs are highly sensitive to market conditions, and short-term returns often reflect temporary dynamics rather than structural differences.

A more rigorous approach begins with a simple question: what exposure am I actually buying?

Two ETFs may both be described as ‘commodity ETFs’, yet one may derive its returns from gold prices, while another is driven by energy markets or futures contracts. Without understanding this distinction, it is impossible to make a meaningful comparison.

The next layer of analysis involves structure.

As discussed earlier, the choice between physical and futures-based exposure has significant implications. Futures-based ETFs, in particular, introduce additional return drivers through rolling mechanics. The impact of contango or backwardation can materially influence long-term performance.

Costs must also be considered in context.

Unlike equities or bonds, commodities do not generate income. Returns are driven entirely by price movements. This means that fees, even when relatively low, represent a direct reduction in returns. Over time, this effect compounds.

Liquidity is another critical factor, particularly in the Australian market.

More liquid ETFs tend to trade with tighter spreads and more efficient pricing. This reduces transaction costs and improves execution, particularly for investors making regular adjustments to their portfolios.

Ultimately, however, the most important consideration is how an ETF fits within a portfolio.

An investor seeking inflation protection will prioritise different characteristics from one seeking growth exposure. The same ETF may be entirely appropriate in one context and inappropriate in another.

Integrating Commodity ETFs into Portfolio Construction

The role of commodity ETFs within portfolios cannot be understood in isolation. It must be considered within the broader framework of asset allocation.

The CFA Institute has long emphasised that diversification across asset classes is a primary driver of long-term investment outcomes. Commodities contribute to this by introducing exposures that are fundamentally different from equities and bonds.

However, their role is not static.

Commodity ETFs are rarely used as core holdings. Instead, they function as satellite allocations, designed to enhance diversification and provide exposure to specific macroeconomic conditions.

For most investors, this translates into relatively modest allocations, typically in the range of 5-15% of a portfolio. The precise allocation depends on individual objectives, risk tolerance, and market conditions.

Portfolio Construction Across Investor Types

For SMSF investors, commodity ETFs provide a practical way to diversify portfolios that are often heavily weighted towards equities and property.

The Australian Taxation Office emphasises the importance of diversification and liquidity within SMSFs, both of which are supported by commodity ETFs.

Gold ETFs, in particular, are frequently used within SMSFs as a defensive allocation. Broader commodity ETFs may be added to provide exposure to inflation and global growth.

For more sophisticated investors, commodity ETFs are often integrated alongside alternative assets such as private credit and infrastructure. In this context, they provide liquidity and flexibility that complements less liquid investments.

Self-directed retail investors tend to approach commodity ETFs as an entry point into alternative assets. For these investors, a phased approach is often appropriate, beginning with gold exposure and expanding into diversified commodities or sector-specific ETFs as understanding develops.

Commodities in Different Market Environments

The effectiveness of commodity ETFs is closely tied to macroeconomic conditions.

During inflationary periods, commodities tend to perform well, reflecting rising input costs and supply constraints. During economic expansions, energy and industrial commodities benefit from increased demand. Conversely, during recessions, commodity prices may decline, although gold may perform more defensively.

This regime-dependent behaviour is central to their value.

Commodity ETFs are not designed to outperform in all environments. Their purpose is to provide diversification and resilience, particularly when traditional assets face challenges.

Risk, Behaviour, and Reality: What Determines Outcomes in Commodity ETF Investing

Commodity ETFs offer Australian investors access to one of the most powerful yet misunderstood segments of global markets. They can improve diversification, provide protection in inflationary environments, and offer exposure to real economic activity. Yet these same characteristics introduce risks that are fundamentally different from those associated with equities or bonds.

The critical insight is this: commodity ETF outcomes are not primarily determined by the product itself, but by the interaction between structure, macroeconomic conditions, and investor behaviour.

Investors who approach commodities as if they were simply another ‘growth asset’ are likely to be disappointed. Those who understand their role as cyclical, regime-sensitive instruments are far more likely to use them effectively.

The Nature of Risk in Commodity ETFs: Why Volatility Is Structural

Risk in commodity ETFs is often described in terms of volatility, but this framing can be misleading. Volatility is not simply a statistical property. It is a reflection of how commodities themselves are priced.

Unlike equities, which are ultimately anchored to earnings, or bonds, which are anchored to contractual cash flows, commodities are priced at the margin of supply and demand. Small imbalances can produce disproportionately large price movements.

The International Energy Agency has repeatedly demonstrated how energy markets respond to relatively modest disruptions in supply. A geopolitical event, a production decision, or a shift in inventory levels can lead to rapid repricing across global markets.

For investors, this has two important implications.

First, commodity ETFs will exhibit periods of sharp appreciation and equally sharp declines. These movements are not anomalies. They are intrinsic to the asset class.

Second, these movements are often disconnected from traditional financial indicators. Earnings forecasts, valuation multiples, and interest rate models provide limited explanatory power in commodity markets. Instead, prices are driven by physical constraints, logistical realities, and geopolitical developments.

This explains why commodities can perform strongly at precisely the moments when traditional assets struggle. It also explains why they can underperform for extended periods when supply is abundant or demand weakens.

Structural Complexity: Why Exposure Is Not Always What It Appears

A further layer of risk arises from the way commodity exposure is constructed within ETFs.

For many investors, there is an implicit assumption that an ETF labelled as a commodity ETF will closely track the price of the underlying commodity. In practice, this is often not the case.

The use of futures contracts introduces additional return drivers that operate independently of spot prices. As the CME Group explains, the shape of the futures curve determines whether investors experience positive or negative roll yield over time.

In prolonged contango environments, this can result in a gradual erosion of returns, even if the underlying commodity price is stable. Conversely, in backwardation, returns may be enhanced.

These dynamics are subtle, but they accumulate over time. They also explain why two investors with identical views on a commodity may experience very different outcomes depending on the structure of the ETF they choose.

For Australian investors, this is one of the most important areas of due diligence. Understanding whether an ETF provides physical exposure, futures-based exposure, or equity-linked exposure is not a technical detail. It is central to expected outcomes.

Currency and the Australian Context: A Layer Often Overlooked

For investors operating within Australia, commodity ETF performance is further shaped by currency movements.

Most global commodities are priced in US dollars. As a result, the return experienced by an Australian investor reflects both the movement in the commodity price and the movement in the exchange rate.

A weakening Australian dollar can enhance returns, effectively amplifying gains from rising commodity prices. A strengthening dollar can have the opposite effect, offsetting or even reversing gains.

This interaction introduces an additional source of variability that is often overlooked in superficial comparisons. It also reinforces the importance of understanding whether an ETF is hedged or unhedged, and how this aligns with the broader portfolio.

Behavioural Risk: The Gap Between Theory and Practice

If structural risk explains how commodity ETFs behave, behavioural risk explains how investors experience that behaviour.

The CFA Institute has long emphasised that investor outcomes are shaped as much by behaviour as by asset allocation. In commodity investing, this is particularly evident.

Commodity cycles tend to attract attention at their extremes. Periods of rising prices generate strong narratives, often centred on supply shortages, structural demand, or geopolitical tension. These narratives are compelling, and they often coincide with increased search activity for terms such as ‘best commodity ETFs Australia’.

By the time these searches peak, however, prices have often already adjusted to reflect the underlying conditions.

This creates a recurring pattern.

Investors allocate capital during periods of strong performance, expecting continuation. When conditions normalise or reverse, prices decline, leading to disappointment and, in many cases, premature selling.

This pattern is not unique to commodities, but it is amplified by their volatility.

The consequence is a gap between theoretical returns and realised returns. Commodity ETFs may perform exactly as expected over a full cycle, yet investors may underperform due to timing decisions.

Common Misinterpretations: Where Investors Go Wrong

Much of the misunderstanding around commodity ETFs stems from applying frameworks designed for other asset classes.

One of the most persistent errors is treating commodities as long-term compounding assets. Unlike equities, commodities do not generate earnings that can be reinvested. Their returns are episodic, driven by cycles rather than growth.

This does not make them less valuable. It makes them different.

Their role is not to replace equities, but to complement them. They provide exposure to different drivers, and therefore different outcomes.

Another common misinterpretation is the assumption that all commodity exposure is equivalent. As discussed throughout this report, the difference between physical, futures-based, and equity-linked exposure is profound. Failing to recognise this can lead to outcomes that diverge significantly from expectations.

Finally, there is a tendency to over-allocate during periods of strong performance. While commodities can enhance returns in certain environments, excessive exposure increases portfolio volatility and reduces diversification benefits.

Reframing Commodity ETFs: From Products to Portfolio Tools

The most effective way to avoid these pitfalls is to reframe how commodity ETFs are understood.

They are not standalone investments in the traditional sense. They are tools, designed to achieve specific outcomes within a broader portfolio.

For some investors, that outcome is inflation protection. For others, it is diversification. For more sophisticated investors, it may be tactical positioning based on macroeconomic views.

This reframing shifts the focus from selecting the best commodity ETF to understanding how different types of commodity exposure interact with the rest of the portfolio.

It also aligns directly with the role of InvestmentMarkets. The platform is not simply a marketplace for products. It is a research environment that allows investors to move from broad concepts to specific implementations, comparing different forms of exposure and understanding their implications.

Limited")