RMBS invests in a portfolio of Australian residential mortgage-backed securities. RMBS aims to provide investment returns, before fees and other costs, that closely track the performance of the Index.

The fund aims to achieve a total return at least equal to movements in the MSCI World REITs Index (USD) (hedged into AUD) over a rolling 5 to 7-year timeframe through exposure to a diversified portfolio of Sharia Compliant REIT investments.

REIT ETF gives investors access to a diversified portfolio of international REITs with returns hedged into Australian dollars. This fund aims to provide investment returns, before fees and other costs, which track the performance of the Index.

Vanguard Australian Property Securities Index ETF seeks to track the return of the S&P/ASX 300 A-REIT Index before taking into account fees, expenses and tax.

MVA gives investors exposure to a diversified portfolio of Australian REITs. MVA holds a minimum of 10 Australian REITs, with a maximum weighting of 10% for each REIT. This fund aims to provide investment returns, before fees and other costs, that closely track the returns of the Index.

Property ETF Investing: A Comprehensive Guide for Australian Investors

Property has long occupied a unique place in Australian investors' portfolios. It combines the potential for income generation with exposure to long-term economic growth, inflation-linked rental streams and tangible underlying assets. Yet while direct property ownership remains deeply ingrained in Australia's investment culture, the practical realities of buying, managing and financing property have become increasingly challenging.

Higher interest rates, elevated property prices, increasing regulatory complexity and changing workplace trends have prompted many investors to reconsider how they access the property sector. At the same time, the growth of exchange-traded funds has made listed property exposure more accessible, diversified and liquid than ever before.

Property ETFs provide investors with an efficient way to gain exposure to commercial real estate, shopping centres, industrial warehouses, healthcare facilities, residential developments, self-storage businesses and increasingly important digital infrastructure assets such as data centres. Investors can access these opportunities without the concentration risk, leverage requirements or operational burdens associated with direct ownership.

For investors, however, the key question is not whether property belongs in a portfolio.

The more important question is which type of property exposure best aligns with your portfolio objectives, risk tolerance and broader asset allocation decisions.

This guide examines property ETFs through that lens. It explores how they work, where they fit within diversified portfolios, how Australian and global property markets differ, and how investors can evaluate the growing range of property investment opportunities available today.

Table of Contents

Why Property ETFs Matter in Today's Market

Property ETFs occupy a unique position within modern portfolios because they provide exposure to one of the world's largest income-generating asset classes through a liquid, transparent and highly accessible structure. While Australians have traditionally favoured direct property ownership, listed property securities offer a fundamentally different investment proposition.

Rather than concentrating capital in a single residential property or commercial asset, property ETFs provide diversified exposure to portfolios of income-producing real estate spanning multiple sectors, geographies and economic drivers.

This distinction has become increasingly important as property markets have evolved. Two decades ago, listed real estate was largely associated with shopping centres, office towers and traditional commercial property. Today, many of the fastest-growing segments of the global property market are linked to structural themes that extend well beyond conventional real estate. Data centres supporting artificial intelligence and cloud computing, logistics facilities underpinning e-commerce supply chains, healthcare campuses serving ageing populations and specialised residential housing are all now significant components of global listed property markets.

According to MSCI, the global listed real estate universe represents trillions of dollars in market capitalisation across hundreds of companies spanning North America, Europe and Asia-Pacific. This breadth allows investors to access property sectors that are either unavailable or underrepresented in Australia, while also reducing reliance on a single economy, regulatory environment or property cycle.

For Australian investors, this creates an important strategic choice. Domestic property ETFs provide exposure to Australia's established A-REIT sector, which includes some of the country's largest and most sophisticated property owners. These businesses own and manage billions of dollars of property assets across industrial, retail, office and diversified property sectors, providing investors with access to rental income streams and commercial property markets that would otherwise require substantial capital to replicate directly.

The role of these ETFs extends beyond simple property exposure. Goodman Group, for example, has become one of the world's largest owners and developers of logistics and industrial facilities, benefiting from long-term growth in e-commerce, supply-chain modernisation and increasingly, demand for AI-related infrastructure. As a result, investors purchasing a broad Australian property ETF are often gaining exposure not merely to 'property', but to some of the most important structural growth themes shaping the global economy.

Investors seeking broader diversification may look beyond Australia. These global businesses derive their value from entirely different economic drivers than a traditional suburban shopping centre or office building, highlighting how specialised listed real estate has become.

Institutional investors increasingly view property through a sector-allocation lens rather than treating it as a single homogeneous asset class. The investment characteristics of a data-centre operator exposed to artificial intelligence infrastructure demand differ significantly from those of an office landlord navigating hybrid work trends. Likewise, healthcare property, self-storage facilities, student accommodation and logistics warehouses each respond to different demographic, technological and economic forces.

The RBA’s March 2026 Financial Stability Review offers a balanced view of Australian commercial real estate. It noted that fundamentals improved across most CRE markets in 2025 and that valuations and rents increased across most sectors. It also highlighted that demand for prime office space is supporting valuations and rents, while weaker conditions remain in lower-grade office properties and areas with high vacancies, including parts of Melbourne. Industrial property has been supported by demand for warehousing and distribution centres.

As MSCI has argued in its recent outlook for real assets, sector selection within listed real estate is becoming increasingly important as structural growth trends reshape property markets globally. For investors, this means the question is no longer simply whether property deserves a place in a portfolio. Increasingly, the more important question is which types of property exposure are likely to benefit from the long-term forces transforming the global economy, and which ETF provides the most effective way to access them.

What Is a Property ETF?

A property ETF is a listed investment vehicle that provides exposure to property-related securities, usually real estate investment trusts, known as REITs or A-REITs in Australia.

The ASX describes A-REITs as listed vehicles that provide exposure to assets such as office towers, shopping malls, industrial buildings, hotels and cinemas. They are pooled investments managed professionally and traded on the ASX in the same way as shares. That liquidity is one of the main reasons property ETFs are structurally different from direct property and unlisted property funds.

They own listed securities issued by property companies or trusts. Those underlying entities own, manage, finance or develop real estate assets.

This means property ETFs sit between direct real estate and listed equities.

They are exposed to property fundamentals, but their unit prices move daily with share market sentiment, interest-rate expectations, earnings revisions and capital-market liquidity.

This hybrid quality is both useful and dangerous. It gives investors liquidity and transparency, but it also means listed property can fall sharply during equity-market stress, even when underlying buildings are still leased.

Australian REIT ETFs invest primarily in listed Australian real estate investment trusts (A-REITs), providing exposure to commercial property sectors such as industrial, retail, office and diversified property portfolios.

A practical example available on InvestmentMarkets is the Vanguard Australian Property Securities Index ETF (ASX: VAP), which seeks to track the performance of the S&P/ASX 300 A-REIT Index. VAP provides broad exposure to Australia's listed property sector through a single investment and can be useful for investors seeking diversified domestic property exposure without having to select individual REITs.

Another example is the VanEck Australian Property ETF (ASX: MVA), which applies a maximum weighting to individual REITs to reduce concentration risk. This can appeal to investors concerned about the dominance of a small number of large property companies within the Australian listed property market.

Australian REIT ETFs may be most suitable for investors seeking Australian-dollar income streams, exposure to domestic commercial property and a closer connection to Australian economic conditions.

Global Property ETFs

Global property ETFs invest in listed real estate companies and REITs across multiple countries, allowing investors to access sectors and opportunities that are either underrepresented or unavailable in Australia.

This can include exposure to global leaders such as Prologis, the world's largest logistics REIT, Equinix, a major data centre operator, and Digital Realty, one of the largest owners of digital infrastructure globally.

A relevant example on InvestmentMarkets is the VanEck FTSE International Property (Hedged) ETF (ASX: REIT). The ETF provides exposure to a diversified portfolio of international REITs while hedging currency movements back into Australian dollars. This allows investors to focus primarily on underlying property performance rather than foreign exchange fluctuations.

Investors seeking a more active approach may consider the Resolution Capital Global Property Securities Active ETF (ASX: RCAP), which uses active management to identify what its managers believe are the most attractive listed property securities globally. Rather than simply tracking an index, the fund seeks to add value through security selection and portfolio construction.

Global property ETFs can play an important diversification role because they provide access to sectors such as data centres, healthcare facilities, self-storage, residential rental housing and logistics infrastructure, many of which have much smaller representation in Australian property indices.

Thematic Property ETFs

Thematic property ETFs focus on specific real estate sectors rather than the property market as a whole.

These strategies allow investors to express a view on structural trends that may drive long-term demand for particular property types. Common themes include logistics facilities, healthcare real estate, residential rental housing, self-storage assets and digital infrastructure.

The investment case for thematic property exposure is often driven by secular growth trends. The rapid expansion of cloud computing and artificial intelligence has increased demand for data centres. Population ageing is supporting healthcare real estate. Meanwhile, continued growth in e-commerce is driving demand for modern logistics and distribution facilities.

The trade-off is that thematic strategies can be more concentrated than broad property ETFs. While this concentration may enhance returns when a theme performs well, it can also increase volatility and sector-specific risk.

For investors, the choice between broad property exposure and thematic property exposure ultimately depends on whether the objective is diversified real estate income, targeted growth opportunities, or a combination of both.

Australian property ETFs

Australian property ETFs give investors exposure to A-REITs and listed property securities on the ASX. They are generally useful for investors who want local property exposure, Australian dollar income and familiarity with major domestic property groups.

VanEck Australian Property ETF (ASX: MVA) gives investors exposure to a diversified portfolio of Australian REITs and, importantly, applies a maximum 10% weighting to each REIT. That matters because the Australian listed property market can be highly concentrated. A market-cap weighted index may give very large weights to a small number of dominant names. MVA’s equalisation-style discipline can reduce single-stock concentration, although it may also reduce exposure to the highest-quality market leaders.

SPDR S&P/ASX 200 Listed Property ETF (ASX: SLF) seeks to track the S&P/ASX 200 A-REIT Index. Its role is straightforward: broad Australian listed property beta at a low management fee. For investors who want liquid exposure to the largest A-REITs without trying to select individual securities, SLF is a clean implementation option.

Vanguard Australian Property Securities Index ETF (ASX: VAP) seeks to track the S&P/ASX 300 A-REIT Index. It is another broad Australian listed property option, but because it references the broader S&P/ASX 300 A-REIT universe, investors should compare its holdings, concentration and sector exposures with SLF rather than assuming they are identical.

The key due diligence question for all three is not simply cost. It is index construction. Investors should ask:

What are the top ten holdings?

How much is retail versus office versus diversified versus industrial?

Is the fund market-cap weighted or does it apply concentration limits?

What is the distribution yield after fees?

How have distributions changed through different property cycles?

Does the ETF increase or reduce concentration already present in the investor’s portfolio?

For example, an SMSF trustee who already owns Australian banks, domestic equities and a residential investment property may not need more Australian economic concentration. A domestic A-REIT ETF may still have a role, but only after considering whether global property or infrastructure exposure would improve diversification.

Global property ETFs

Global property ETFs can provide exposure to real estate sectors underrepresented in Australia, including data centres, telecommunications-related real estate, healthcare property, self-storage, apartments, logistics and specialist property platforms.

VanEck FTSE International Property (Hedged) ETF (ASX: REIT) gives Australian investors access to international REITs with returns hedged into Australian dollars. The hedging point is important. Currency can dominate short and medium-term returns from global assets. A hedged global REIT ETF is primarily a property-sector allocation rather than a combined property and currency allocation.

Resolution Capital Global Property Securities Active ETF (ASX: RCAP) is different. It invests in a select number of global listed real estate securities with the aim of providing income and capital growth over the long term. This is not simply passive beta. It introduces manager judgement, portfolio concentration and an active view on which listed real estate companies are mispriced or structurally superior.

Hejaz Property ETF (ASX: HJZP) aims to provide exposure to a diversified portfolio of Sharia-compliant REIT investments and references the MSCI World REITs Index hedged into Australian dollars over a rolling five to seven-year timeframe. It may be relevant for investors seeking property exposure within a values-based or Islamic investment framework, although investors should examine its fee level, holdings, screening methodology and performance history carefully.

Global property exposure is compelling because the global REIT market is more diverse than the Australian market. The US REIT universe includes apartments, single-family rental housing, manufactured housing, towers, data centres, healthcare, self-storage, industrial, gaming, timber and life sciences. Europe and Asia add additional listed real estate sectors and local cycles.

The trade-off is complexity. Global property ETFs can introduce different tax outcomes, regional property cycles, currency hedging costs, overseas interest-rate sensitivity and unfamiliar accounting conventions.

RMBS: property exposure, but not a property ETF in the usual sense

VanEck Australian RMBS ETF (ASX: RMBS) invests in Australian residential mortgage-backed securities. That means investors are exposed to pools of residential mortgages rather than listed property landlords. The income stream is credit-driven, not rent-driven.

The key risks include prepayment, credit spreads, mortgage arrears, housing market conditions and securitisation structure.

This can be highly relevant for income-focused investors, but it belongs in a different portfolio bucket. RMBS is closer to fixed income or securitised credit than listed property equity. It may be useful for investors researching property-linked income, but it should not be used as a substitute for A-REIT exposure.

Property ETFs versus direct property

Property ETFs solve many of the problems direct property creates, but they do not replicate direct property economics.

Direct property gives the investor control. The owner can choose the asset, tenant, debt level, renovation strategy and holding period. It also allows higher leverage than most listed portfolios. For many Australians, this has been the source of wealth creation.

But direct property has structural weaknesses. It is lumpy, illiquid, transaction-cost heavy and idiosyncratic. Stamp duty, selling costs, vacancy, repairs, insurance, body corporate fees, land tax and refinancing risk all matter. A single residential property is not a diversified real estate portfolio. It is a concentrated leveraged asset.

Property ETFs offer the opposite profile: liquidity, diversification and small minimum investment sizes. The InvestmentMarkets listings often show minimum investments of $1 for the listed ETFs. That does not mean investors should allocate casually, but it does highlight how dramatically ETFs reduce the access barrier.

Factor

Property ETF

Direct Property

Liquidity

High

Low

Diversification

High

Typically low

Entry cost

Low

High

Transaction costs

Low

High

Management burden

Minimal

Significant

Borrowing control

Limited

High

Asset control

None

Complete

Geographic reach

Global

Usually local

The behavioural difference is underappreciated. Direct property looks stable partly because it is not priced every second. Listed property looks volatile partly because markets do the repricing continuously. That does not necessarily mean direct property is economically safer. It means the volatility is less visible.

Property ETFs versus unlisted property funds

Unlisted property funds can be attractive for investors seeking direct exposure to specific property assets or portfolios, often with income objectives and less visible price volatility.

The key trade-off is liquidity. A listed property ETF can be sold on market. An unlisted property fund may have limited redemption windows, withdrawal queues, asset-sale dependencies or fixed investment terms. This can be acceptable for investors who are deliberately harvesting an illiquidity premium. It is problematic for investors who mistake illiquidity for capital stability.

Unlisted property may also provide more direct exposure to valuations, rental income and asset-management strategy.

Listed property ETFs provide market liquidity and transparency, but they may trade at discounts or premiums to underlying net asset values based on sentiment.

A sophisticated allocation may use both.

For example, a listed A-REIT ETF for liquidity and tactical rebalancing, and a global property ETF for diversified sector exposure.

An unlisted property fund for targeted income or development exposure.

Infrastructure or private credit for adjacent real-asset income.

The point is not to choose one structure forever. It is to match structure to purpose.

Interest rates: the central variable investors cannot ignore

Property ETFs are highly sensitive to interest rates because real estate valuation depends heavily on discount rates, debt costs and income yields.

When bond yields rise, property securities often face pressure from three directions. First, higher discount rates reduce the present value of future rental income. Second, borrowing costs rise as debt is refinanced. Third, income investors can obtain more attractive yields from cash and bonds, reducing the relative appeal of property distributions.

But the relationship is not mechanical. Some property companies can grow rents faster than financing costs. Logistics landlords with scarce assets in supply-constrained locations may have stronger pricing power than secondary office landlords. Data centre operators may benefit from structural demand even when rates remain elevated. Retail landlords may recover if occupancy, foot traffic and tenant sales improve.

This is why broad macro calls are not enough.

A property ETF investor needs to understand whether the fund owns assets with pricing power, or merely assets with yield.

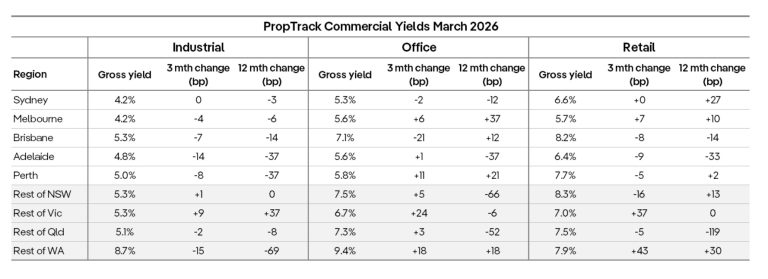

The sector split: office, retail, industrial, logistics, healthcare and data centres

The most important development in property investing is dispersion. Property is no longer a single asset class in any meaningful practical sense.

Here’s a snapshot of the gross yields on offer across the various Australian geographies and sectors:

Office faces a two-speed market. Premium buildings in strong locations can still attract tenants, especially where businesses want high-quality space to draw employees back. Lower-grade office buildings in weaker locations face vacancy, incentive and obsolescence risks.

Retail has moved beyond the simplistic ‘online shopping kills malls’ narrative. Strong convenience retail, neighbourhood centres and dominant experiential centres can remain resilient. Weak discretionary retail assets may still struggle.

Industrial and logistics have been structurally supported by e-commerce, supply-chain resilience and demand for warehousing. The RBA noted ongoing demand for warehousing and distribution centres as a driver of industrial valuations and rents in 2025.

Healthcare property benefits from demographic ageing, medical demand and often long leases. It can provide defensive characteristics, although valuation still matters.

Data centres are perhaps the most discussed property segment of the moment. PwC Australia notes that data centres support share trading, banking, streaming, weather apps, AI, cloud computing and the Internet of Things. It also cites forecasts that Australia may need an additional 1,750MW of data centre capacity by 2030, implying more than $20 billion of investment. That is a powerful structural tailwind, but not a free lunch. MSCI warns that AI workloads are increasing technical requirements, including power density, cooling and connectivity, raising obsolescence risk for older facilities.

This is exactly why global property ETFs and active property strategies deserve attention.

he future of listed property may be shaped less by the generic category of ‘real estate’ and more by which real estate businesses own scarce, technically relevant, well-located, well-capitalised assets.

How to evaluate a property ETF

Sophisticated investors should evaluate property ETFs across seven dimensions.

1. Geography.

Is the exposure Australian, global developed markets, US-heavy, Asia-heavy or currency-hedged?

2. Sector composition.

How much is industrial, office, retail, residential, healthcare, self-storage, data centres or diversified property?

3. Concentration.

Does the ETF have a dominant single holding? MVA’s maximum 10% weighting rule is relevant here because it directly addresses concentration risk within Australian listed property.

4. Fee structure.

ETF fees range from 0.3% to 1%. Fees are not the only variable, but they compound through time.

5. Currency.

A hedged global property ETF reduces currency volatility, but hedging has costs and may remove diversification benefits from foreign currency exposure.

6. Distribution quality.

Investors should distinguish between recurring rental income, capital gains, tax-deferred components and distribution volatility.

7. Portfolio role.

A property ETF used for income should be judged differently from one used for global real asset growth or tactical recovery exposure.

Portfolio construction: where property ETFs fit

Property ETFs can play several roles in a portfolio.

For income investors, A-REIT ETFs may provide distributions linked to underlying rental income. The caveat is that distributions can fall, and listed property capital values can be volatile.

For growth investors, global property ETFs may provide exposure to structural sectors such as logistics, data centres, healthcare, storage and residential rental platforms.

For SMSFs, property ETFs can reduce concentration risk. Many SMSF members already have large exposure to Australian residential property through their home, investment property or family wealth. Adding an Australian A-REIT ETF may deepen domestic property exposure rather than diversify it. A global property ETF or infrastructure allocation may be more useful in some cases.

For diversified investors, property ETFs can sit between equities and fixed income. They are not defensive assets in the same way high-quality bonds can be defensive, but they may provide real-asset income and inflation-linked rental growth over time.

A practical allocation framework might look like this:

Investor objective

Potential ETF role

Relevant InvestmentMarkets examples

Domestic property income

A-REIT exposure

SLF, VAP, MVA

Reduced single-stock concentration

Capped Australian REIT exposure

MVA

Global real estate diversification

Hedged international REITs

REIT

Active global property selection

Manager-led security selection

RCAP

Values-based property exposure

Sharia-compliant global REITs

HJZP

Property-linked income via credit

Residential mortgage-backed securities

RMBS

Tax considerations for Australian investors

Tax should not drive the investment thesis, but it can materially affect after-tax returns.

Property ETF distributions may include rental income, capital gains, tax-deferred components, foreign income and franking credits depending on the underlying holdings and structure. Australian A-REIT distributions are often not franked in the same way company dividends may be, because trust income flows through differently.

Global property ETFs can introduce foreign withholding tax considerations and currency-hedging tax outcomes. SMSF investors should consider whether income, capital gains and liquidity align with pension-phase or accumulation-phase requirements.

The practical point is simple: investors should not compare property ETFs purely on headline yield. They should compare after-tax income quality, distribution sustainability and total return.

Risks and Considerations

Property ETFs can provide attractive income and diversification benefits, but they are not low-risk investments. Their performance is influenced not only by property market fundamentals, but also by equity market sentiment, interest-rate expectations and the financial health of the underlying property companies they hold.

One of the most important risks is interest-rate sensitivity. Property companies typically rely on debt to acquire and develop assets, meaning higher borrowing costs can place pressure on earnings, property valuations and investor demand. Rising bond yields can also reduce the relative attractiveness of property income, particularly when investors can obtain higher yields from cash and fixed-income investments.

Investors should also recognise that listed property securities can behave very differently from direct property ownership. While a residential property may be valued only periodically, property ETFs are priced continuously by the market. This can result in significant short-term volatility, even when the underlying properties remain occupied and continue generating rental income. During periods of market stress, listed property securities have historically exhibited equity-like drawdowns despite being backed by tangible assets.

Sector-specific risks are becoming increasingly important as the property market evolves. Office landlords continue to face uncertainty surrounding hybrid work arrangements, while retail property owners remain exposed to changing consumer spending patterns. Conversely, sectors such as logistics facilities, healthcare real estate and data centres may benefit from structural growth trends, but often trade at higher valuations that can make them vulnerable to changes in investor expectations.

Currency and geopolitical risks may also affect returns. While some funds hedge foreign currency exposure, global property markets remain exposed to differing economic cycles, regulatory environments and interest-rate settings.

Finally, investors should be aware of concentration risk.

Australia's listed property market is relatively small compared with global markets, and broad Australian property ETFs can be heavily influenced by a handful of large holdings. Understanding the composition of an ETF, including its exposure to individual companies, property sectors and geographic regions, is therefore an important part of the due diligence process.

As with most asset classes, the greatest risk is often not the property itself, but paying too much for it. Investors should evaluate property ETFs not only on distribution yield or recent performance, but also on valuation, balance-sheet strength, sector exposure and their role within a broader diversified portfolio.

Common mistakes property ETF investors make

1. Yield chasing.

A high distribution yield may signal value, but it may also signal stress, leverage risk, falling asset values or unsustainable payout policy.

2. Ignoring concentration.

Australian property indices can be heavily influenced by a few large names. That can be acceptable, but it should be intentional.

3. Assuming property ETFs are defensive.

Listed property can fall sharply in equity-market sell-offs.

4. Treating all property sectors alike.

Data centres, logistics warehouses, CBD office towers and suburban shopping centres do not share the same risk profile.

5. Ignoring fees in active or specialised funds.

Higher fees may be justified by skill, access or screening methodology, but investors should demand evidence.

6. Forgetting existing property exposure.

An Australian homeowner with an investment property and bank-heavy equity portfolio may already be more exposed to domestic property and credit cycles than they realise.

The outlook for property ETFs

The outlook is constructive but selective. The easy money from falling yields is gone.

Future returns are likely to depend more on rental growth, balance-sheet strength, asset quality, development discipline and sector selection.

Australian listed property appears to be moving into a more stable phase, supported by improving CRE fundamentals and still-sound financial conditions among A-REITs. But risks remain in lower-grade office assets and any property group dependent on cheap refinancing.

Global property offers a broader opportunity set. Data centres, logistics, healthcare and specialist residential sectors may benefit from structural demand, while traditional office and weaker retail assets require more caution.

The strongest argument for property ETFs is therefore not that ‘property always goes up’. It is that listed real estate gives investors a flexible way to allocate capital across a changing real-assets universe.

FAQs

Property ETFs can be useful for investors seeking diversified real estate exposure, income and liquidity. They are most suitable when the investor understands the difference between listed property securities and direct property ownership.

On InvestmentMarkets, the relevant listed examples include MVA, SLF, VAP, REIT, RCAP, HJZP and RMBS. Investors should compare them by geography, sector exposure, fees, index methodology, currency hedging and portfolio role.

An A-REIT ETF focuses on Australian listed property securities. A global property ETF invests across international REITs and property companies, often giving investors access to sectors such as data centres, self-storage, healthcare property and global logistics.

Property ETFs are usually more diversified and liquid than direct property, but they are not necessarily safer. They are priced daily on listed markets and can be volatile. Direct property has less visible volatility but higher concentration and liquidity risk.

Many property ETFs pay distributions, but income can vary depending on rents, borrowing costs, asset sales, tax components and underlying trust structures. Investors should assess total return rather than headline yield alone.

Higher interest rates can pressure property ETFs by increasing borrowing costs and reducing valuation multiples. However, strong rental growth, low vacancy and high-quality assets can partly offset rate pressure.

There is no universally better option. MVA may appeal to investors concerned about concentration because it limits individual REIT weights. SLF and VAP may suit investors seeking broad market exposure. The right choice depends on holdings, fees, sector exposure and portfolio role.

Global property ETFs can help SMSFs diversify away from Australian residential property and domestic A-REIT concentration. They may provide exposure to sectors less available in Australia, although currency, tax and global market risks need to be considered.

Key investor takeaways

Property ETFs are not a simple substitute for buying an investment property. They are liquid listed vehicles that provide diversified access to property-related securities.

Australian property ETFs such as MVA, SLF and VAP provide domestic A-REIT exposure, but investors should compare index construction, concentration and sector weights carefully.

Global property ETFs such as REIT, RCAP and HJZP can broaden exposure into sectors underrepresented in Australia, including data centres, healthcare, logistics and specialist real estate.

RMBS is property-linked, but it is closer to securitised credit than equity real estate exposure.

Interest rates remain central, but sector fundamentals now matter more than broad property labels.

The best property ETF choice depends on portfolio role, not product popularity.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.