The fund aims to provide investors with the performance of the S&P Small-Cap 600®, before fees and expenses. The index is designed to measure the performance of small-capitalisation US equities.

The SPDR® S&P 500® ETF seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index.

Vanguard All-World ex-U.S. Shares Index ETF seeks to track the return of the FTSE All-World ex US Index before taking into account fees, expenses and tax.

The Fund aims to provide investors with the performance of the MSCI World Ex Australia Custom ESG Leaders Index, before fees and expenses. The index is designed to measure the performance of global, developed market large and mid- capitalisation companies with better sustainability credentials relative to their sector peers.

H100 aims to track the performance of the AUD currency hedged FTSE 100 Index (before fees and expenses), which provides exposure to the largest 100 companies by market capitalisation traded on the London Stock Exchange. H100 currently obtains its investment exposure by investing in the Betashares FTSE 100 ETF (ASX: F100), with the foreign currency exposure hedged back to the Australian dollar.

LEND gives investors exposure to a portfolio of 25 of the largest listed companies involved in private credit. LEND aims to provide investment returns before fees and other costs which track the performance of the Index with returns hedged into Australian dollars.

Argo Investments is one of Australia's oldest and largest listed investment companies (LICs). Offering investors low-cost, conservative and diversified exposure to Australian listed companies.

The fund aims to achieve a total return of 1% above the S&P/ASX Accumulation Index p.a. and have a distribution yield 2% greater that the Intelligent Investor Growth portfolio over rolling five year periods, after fees.

The fund aims to provide investors with the performance of the S&P Global 100TM Index, before fees and expenses. The index is designed to measure the performance of 100 multi-national, blue chip companies of major importance in global equity markets.

The Fund is an actively managed fund that invests predominantly in a broad range of international shares and equity-related securities that are listed on stock exchanges in developed and emerging international markets. At least 80% of the Fund’s NAV will be invested in shares and equity-related securities selected by Russell Investments based on advice received from investment managers pursuing a Sustainable Strategy.

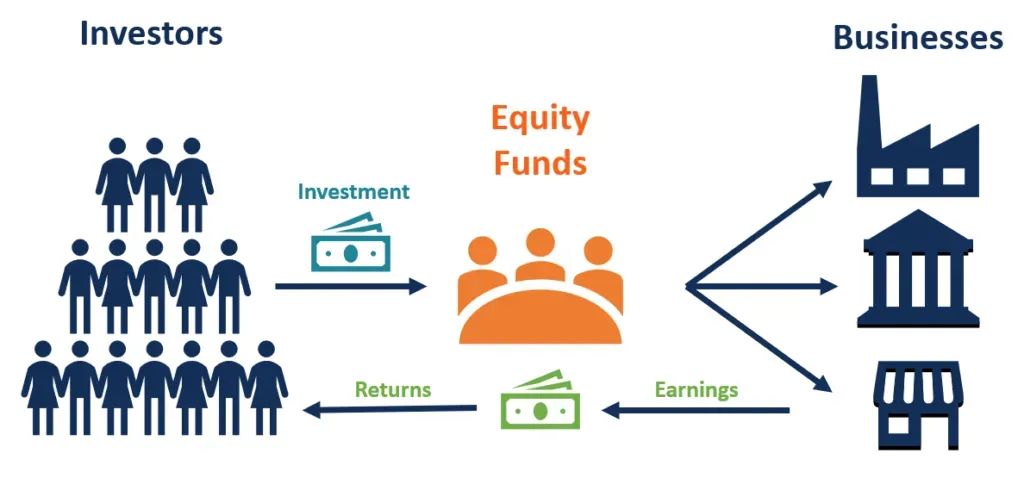

Equity funds are investment vehicles which pool capital from multiple investors to purchase shares of publicly traded companies. These funds aim to generate a total return through income and capital growth.

Investors choose equity funds based on their individual investment goals, risk profiles, and preferred market focus, such as large-cap, mid-cap, small-cap, or international equities. Equity fund managers actively or passively manage these funds, utilising various strategies to optimise their returns.

By diversifying across multiple stocks, equity funds help mitigate investors’ risk while offering the potential for to generate solid long-term gains, making them an appealing option for those looking to participate in the stock market with minimal effort.

What Are Equity Funds

Equity funds are pooled investment vehicles that primarily invest in publicly traded companies. These funds are commonly referred to as managed equity funds, mutual funds, stock funds, or share funds. By pooling money from multiple investors without the need for direct stock selection, equity funds provide diversification and professional management, making it easier for individual investors to access the stock market and potentially benefit from attractive total returns over the long term.

Equity funds are structured based on specific goals, such as income generation or capital growth, thus allowing investors to align their investments with their financial objectives. Equity funds offer a number of key advantages including professional management without the need for direct stock selection, and reduced risk due to diversification. This is general information only. Speak to a financial adviser and review a fund’s Product Disclosure Statement (PDS) before making an investment decision.

Table Of Contents

How do Equity Funds Work?

Equity funds pool money from multiple investors to buy shares in publicly listed companies. These investments combine to form a diversified portfolio which is either managed actively by a fund manager, or passively through an index-tracking strategy.

It’s important to understand that when you invest in an equity fund, you’re buying units in the fund — not the individual shares themselves. The value of your fund investment rises or falls based on the performance of the underlying shares.

There’s a vast array of equity funds available to investors. For example, some funds focus on capital growth and reinvest their gains to compound over time, while others prioritise income, paying dividends to investors at regular intervals. Other funds may invest in local or international markets, target specific sectors like technology or healthcare, or align with ethical screening criteria (ESG).

Equity funds offer professional management, built-in diversification, and varying levels of risk and return depending on the fund’s strategy. Importantly, all equity funds charge management fees, and returns aren’t guaranteed — so careful comparison is essential.

Income vs Growth: What Do You Want from Your Equity Fund?

Equity funds deliver two primary investment outcomes: income or growth.

Understanding which of these outcomes best aligns with your investment goals is critical to selecting the right fund.

Income from Equity Funds

Income-focused equity funds generate income primarily through dividend distributions, which are generally made quarterly or semi-annually, thus providing regular cash flow for investors. Income-focused equity funds often invest in high-yielding stocks which consistently pay-out above-average dividends. In general, investors can choose between reinvesting their fund dividends to compound their returns or receiving cash dividend payments. Income-focused equity funds are ideal for investors seeking regular income payments such as self-managed superannuation funds (SMSFs) and self-funded retirees.

In tax-advantaged markets like Australia, franked dividends enhance fund income by allowing investors to benefit from tax credits.

Other benefits of income-focused equity funds include: lower volatility than most strategies, the potential for long-term capital growth, and diversification.

Growth from Equity Funds

Growth-focused equity funds aim for capital appreciation through rising share prices, harnessing growth-oriented strategies centred on future earnings potential. These funds generally aim to amplify their long-term returns through portfolio rebalancing and dollar-cost averaging (buying more stock at regular intervals).

While growth-focused equity funds can be more volatile than income-focused funds, they have historically generated strong long-term returns, making them a compelling choice for investors who are willing to withstand market volatility.

Ultimately, these funds are best suited to long-term investors, wealth builders, and younger investors who have the time to ride out market cycles.

How to Invest in Equity Funds

Investing in equity funds is a convenient and easy way for investors to gain exposure to the share market, whether you’re aiming to grow your wealth or generate income. But with so many options available, it’s important to choose an equity fund that aligns with your financial goals, time horizon, and risk tolerance.

Start with a clear goal

Prior to investing in equity funds, it’s important to clarify what your investment goals are.

There are three main investment goals which equity funds can help deliver:

Capital growth: If you’re building long-term wealth, consider growth-focused equity funds which invest in high growth businesses and generally reinvest their gains to compound their long-term returns.

Income generation: If you’re seeking regular cash flow, consider income-focused equity funds that pay regular dividends. In Australia, most of these funds pay fully or partially franked dividends which enhances their value for most investors.

Balanced approach: If you’re after both capital growth and income, consider both growth and income funds for diversification and portfolio stability.

Compare fund options

Once you’ve identified your investment goal, the next step is to compare the available equity funds based on the following factors:

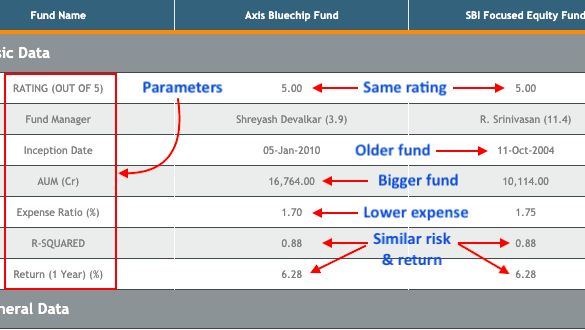

Past performance (1/3/5 years): Start by analysing the funds’ past performance over 1, 3, and 5 years, as it provides contextual insights into how they performed in a range of market conditions, despite not guaranteeing future results.

Fund ratings: Fund ratings by leading rating providers such as Morningstar, Lipper, Zacks, TheStreet.com, and Standard & Poor’s provide an assessment of a fund’s performance, risk, and consistency, in support of more informed investment decisions.

Yield: It’s worth checking a fund’s yield, particularly if you prioritise regular cash flow for expenses or reinvestment.

Management Expense Ratio (MER): It’s also crucial to consider fund management fees and costs as lower expenses can significantly enhance a fund’s long-term returns. The Management Expense Ratio is a fund’s combined management costs and includes management fees, commissions, operating expenses and taxes. In general, an MER below 0.75% is competitive while an MER above 1.5% is considered high.

Assets Under Management (AUM): Fund AUM is worth considering since larger funds are more likely to survive over the longer term as they are better able to cover their running costs. For example, a fund with AUM of $250 million may have a more sustainable future than a $10 million fund.

Inception Date: Funds with a successful longer term track record are generally regarded as lower risk since the manager has proven their ability to navigate the market’s ups and downs. Be more careful with new funds, or funds with short track records.

R-Squared Ratio: A fund’s R-squared ratio tells you how much of its price movement is explained by the movement of a benchmark index such as the All Ords. For example, a fund with an R-squared ratio of 1.0 can be expected to perform in line with the market, whereas a fund with an R-squared ratio of 0.5 can be expected to be less sensitive to market movements.

Asset focus: Lastly, evaluate the fund's asset focus: whether it targets Australian blue chips, global tech, or ESG-screened companies, to ensure alignment with your investment strategy and goals.

Each of these criteria collectively informs better investment decisions.

Choose your investment platform

You can invest in equity funds through several channels, including:

Online brokers (e.g. SelfWealth, CommSec) for ETFs and most managed funds.

Direct with fund managers (e.g. Vanguard, Magellan) via their websites.

Your super fund or SMSF platform, if you’re allocating within these retirement savings.

Through licensed financial advisers, if you prefer personalised guidance.

Balanced approach to find the best equity fund

In summary, there’s no universal ‘best’ equity fund for all investors.

Equity funds can be a powerful tool — but only when matched to the right strategy.

Some investors prefer low-cost ETFs for broad market exposure, while others seek actively managed funds for the potential outperformance on offer. What matters most is clarity around your investment goals and a willingness to compare the options carefully.

Always read a fund’s Product Disclosure Statement (PDS) and consider seeking financial advice from a licensed professional.

💡 Tip: Use fund analysis tools like InvestmentMarkets to research equity funds based upon their performance, risk, and fees.

Understand Fund Types – How Equity Funds Are Managed

Further to understanding the various fund types in terms of how they’re managed and what they’re aiming to achieve, here’s a brief comparison.

Fund Type

Strategy

Ideal For

Risk/Return Characteristics

Growth Funds

Invest in companies expected to grow faster than average

Investors seeking long-term capital appreciation

Higher risk and volatility, higher return potential

Value Funds

Target undervalued companies with solid fundamentals

Investors seeking undervalued opportunities

Medium risk and return potential

Index Funds (ETFs

Track a market index passively

Cost-conscious, passive investors

Market-matching returns, lower fees

Sector Funds

Focus on a specific industry or theme

Investors with thematic convictions

Higher risk and return potential

International Funds

Invest in global companies outside your home country

Investors seeking geographic diversification

Higher risk and volatility, higher return potential

Blue-Chip Funds

Invest in large, stable, dividend-paying companies

Conservative investors, SMSFs

Lower risk and volatility, lower return potential

💡 Tip: Start by choosing a fund type that matches your goals (growth vs income) and risk appetite.

Equity Fund Asset Classes - What You're Investing In

Equity funds are also categorised by the assets they invest in. This table breaks down the main asset class types based on region, strategy, size, or other factors.

Global exposure across developed and emerging markets

U.S., Europe, Japan, Asia, Global Tech leaders

Investors seeking diversification beyond Australia

Sector / Thematic

Targets specific industries or megatrends

Exposure to specific sectors such as technology, healthcare, clean energy, infrastructure

Thematic or future-focused investors

Market Cap-Based

Categorised by company size: large, mid, small or micro-cap

Large-cap = stable; Small & micro-cap = high growth

Investors with matching risk/return preferences

ESG / Ethical Equities

Apply screens based on environmental, social, or governance factors

ESG-driven exclusions (e.g. tobacco etc.) & inclusions (e.g. green energy)

Values-aligned investors

💡 Tip: Many investors blend asset classes — like large-cap Australian income funds with global tech or ESG exposure — to create a diversified equity portfolio.

Comparing Equity Funds to Other Investment Options

It’s also worth comparing equity funds with the other investment options, as per the table below.

Comparison

Key Differences

Best For

Risk Profile

Equity Funds vs. Balanced Funds

Balanced funds include bonds/cash, Equity funds are stock-only

Balanced funds are popular with investors wanting more stability than equity funds

Equity funds generally have higher risk/volatility than balanced funds

Equity Funds vs. Bond/Debt Funds

Debt = bonds, Equity = shares

Debt funds are popular with income-focused or conservative investors

Debt funds are generally lower risk than equity funds

Equity Funds vs. Hedge Funds

Hedge = complex, less regulated, high cost

Hedge funds are popular with sophisticated investors who want to manage their market exposure

Most hedge funds carry lower market risk than equity funds but the use of leverage can more than offset this

Equity Funds vs. Private Equity Funds

Private = unlisted, long lock-ins, Equity = listed, liquid

Private equity is popular with high-net-worth/institutional investors

Private equity is illiquid, and thus is generally higher risk than equity funds

💡 These are not always either/or decisions — many investors hold multiple fund types in their diversified portfolios.

What Are the Risks of Equity Funds?

Equity funds offer investors long-term upside potential — but they’re not without risk.

For example, here are a few of the main risks to be aware of

Market Risk

Markets rise and fall due to interest rates, inflation, global events, and economic shifts. Equity funds experience this market volatility.

Manager Risk

Actively managed funds depend on manager skill. Poor manager decisions or style drift can affect returns.

Fund Expenses

Every equity fund charges fees. High MERs (Management Expense Ratios) can erode performance.

Liquidity Risk

Some funds — especially those in micro-cap or emerging markets — may limit withdrawals in stressed conditions due to higher liquidity risk in these markets.

💡 Always review the PDS and understand the risk profile before investing.

Are Equity Funds Right for Me?

Equity funds aren’t just for one type of investor — they’re a flexible, accessible way to invest in the share market, whether you're building wealth, seeking income, or diversifying your portfolio.

But that doesn’t mean every equity fund suits every investor.

Ask yourself:

Am I comfortable with the equity market’s ups and downs?

Do I have a long-term investment horizon (5+ years)?

Do I want professional management rather than picking individual shares?

Am I looking for growth, income, or both?

Do I understand the differences between passive and active fund styles?

If you answered “yes” to most of the above, equity funds could be a strong addition to your investment strategy — especially when chosen carefully and aligned to your goals.

Whether you’re a retiree prioritising franked dividend income, or a growth-minded investor seeking capital appreciation through global tech or small-cap exposure, there’s an equity fund for that.

Equity funds are powerful tools — but like all investments, they work best when matched to a well thought out investment plan.

💡 Final tip: Don’t rush. Compare your options. Use trusted sources. And if in doubt, speak to a licensed adviser.

Equity Fund FAQs

An equity fund pools investors’ money to buy a diversified portfolio of shares. Managed by professionals or algorithms, these funds provide exposure to the stock market — aiming for capital growth, income, or both depending on the fund’s strategy.

Equity funds may suit you if you want long-term growth or income, can tolerate market ups and downs, and prefer professional management over picking individual stocks. They’re ideal for medium to long-term investors seeking diversification.

An ETF is a type of equity fund that trades on the stock exchange whereas an equity fund is an actively managed fund which may or not be listed. While both offer diversified exposure to shares, ETFs are passively managed, lower cost, and offer more trading flexibility than traditional managed equity funds.

A managed fund is a broad category of pooled investments. An equity fund is a type of managed fund that invests mainly in shares. So, all equity funds are managed funds, but not all managed funds are equity funds — some focus on bonds or cash.

Yes, some equity funds distribute dividends received from the companies they invest in. Australian equity funds often include fully or partially franked dividends, which can reduce your effective tax rate and boost after-tax income.

Compare equity funds based on your goals. Look at past performance, fees (MER), income yield, risk level, and investment focus. Use trusted tools like InvestmentMarkets, Morningstar, or Canstar, and always read the Product Disclosure Statement (PDS).

Yes. Most superannuation platforms and SMSFs allow investment in equity funds, including ETFs. It’s a common strategy for building long-term growth or income within a tax-effective retirement structure.

Limited")