The Rise of Exchange Traded Funds and the Democratisation of Fixed Income

The growth of exchange traded funds represents one of the most significant structural developments in modern finance. While ETFs were initially associated with equity index tracking, their expansion into fixed income has been transformative.

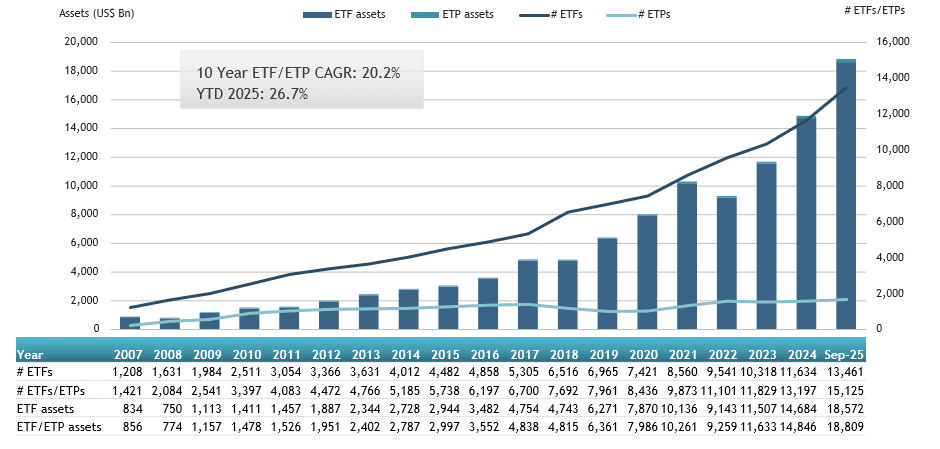

Global ETF assets now exceed US$11 trillion, with fixed income ETFs representing one of the fastest growing segments of that market. This growth reflects more than simple product innovation. It reflects a fundamental change in how investors access markets.

Source: ETGI

Traditional bond markets are complex and, in many cases, opaque. Individual bonds trade over the counter rather than on centralised exchanges, pricing is not always transparent, and minimum investment sizes can be prohibitive. For retail investors, constructing a diversified bond portfolio directly is often impractical.

ETFs have addressed these limitations. By packaging large portfolios of bonds into exchange traded structures, they have made fixed income accessible in a way that was previously impossible for many investors.

Vanguard has noted that exchange traded funds combine ‘the diversification benefits of managed funds with the flexibility of trading like shares.’

This combination of diversification, liquidity, and transparency has been particularly powerful in fixed income markets, where these characteristics were historically lacking.

In Australia, the expansion has been equally pronounced. EY reports that ETF assets have grown to more than $330 billion, a figure that continues to grow as investor adoption broadens across asset classes. Fixed income ETFs have played a meaningful role in this growth, particularly as investors have sought alternatives to traditional cash and term deposit strategies.

Understanding Bond ETFs: Structure, Function, and Behaviour

At their simplest, bond ETFs are investment vehicles that hold diversified portfolios of bonds and allow investors to trade exposure to those portfolios on a stock exchange. However, this simplicity at the surface can obscure important structural nuances that influence how these products behave.

Unlike individual bonds, which have fixed maturity dates and defined cash flows, bond ETFs are perpetual vehicles. They do not mature in the traditional sense. Instead, they continuously rebalance their holdings, replacing bonds that approach maturity with new securities that meet the fund’s criteria.

This has important implications.

When an investor purchases an individual bond and holds it to maturity, the return is largely determined by the bond’s yield at the time of purchase, assuming no default. With bond ETFs, returns are influenced not only by the yield of the underlying securities, but also by changes in interest rates, credit conditions, and market pricing.

This distinction is central to understanding how bond ETFs function.

Income generated by bond ETFs is derived from the coupon payments of the underlying bonds. These payments are typically distributed to investors on a regular basis, often monthly or quarterly. For income-focused investors, this distribution profile is one of the primary attractions of bond ETFs.

At the same time, the price of a bond ETF fluctuates throughout the trading day, reflecting changes in the value of the underlying portfolio. These price movements are driven by a range of factors, including interest rate expectations, inflation data, and broader market sentiment.

This combination of income generation and price variability means that bond ETFs occupy a unique position within portfolios. They are not as volatile as equities, but they are not static instruments like term deposits. Their behaviour sits somewhere in between, shaped by both income and market dynamics.

The Core Components of Fixed Income Investing

To fully understand bond ETFs, it is necessary to understand the underlying components of fixed income markets. Three concepts are particularly important: yield, duration, and credit risk.

Yield represents the income generated by a bond relative to its price. It is often the first metric investors consider, particularly those seeking regular income. However, yield cannot be viewed in isolation. Higher yields often reflect higher risk, whether in the form of longer duration or lower credit quality.

Source: InvestmentMarkets

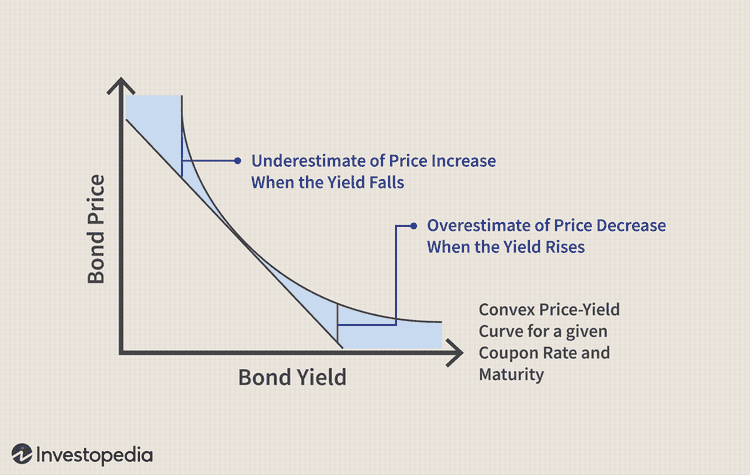

Duration is a measure of a bond’s sensitivity to changes in interest rates. It provides an estimate of how much the price of a bond or bond portfolio will change in response to a given movement in rates. Longer duration bonds are more sensitive to interest rate changes, meaning their prices will fluctuate more significantly when rates move.

Source: Investopedia

This relationship has become particularly relevant in recent years. As interest rates have risen, long-duration bond ETFs have experienced greater price declines than their short-duration counterparts. This has led to increased investor interest in strategies that manage duration exposure more actively.

Credit risk refers to the likelihood that a bond issuer will fail to meet its obligations. Government bonds are generally considered to have low credit risk, particularly in developed markets such as Australia. Corporate bonds, by contrast, carry varying levels of credit risk depending on the financial strength of the issuing company.

Source: MicroMacro

The interplay between these factors determines the risk and return profile of a bond ETF. A portfolio composed of high-quality government bonds with short duration will behave very differently from one composed of lower-rated corporate bonds with longer duration.

The Role of Bond ETFs in Portfolio Construction

The resurgence of bond ETFs is closely linked to their role in portfolio construction. Modern portfolio theory has long emphasised the importance of diversification across asset classes. Bonds have historically played a central role in this framework, providing stability and income to offset the volatility of equities.

The CFA Institute has observed that diversification across asset classes can improve the long-term risk-adjusted return of a portfolio. Bonds contribute to this outcome by exhibiting different return characteristics from equities, particularly during periods of market stress.

However, the relationship between bonds and equities is not static. The events of 2022, when both asset classes declined simultaneously, highlighted the importance of understanding the conditions under which diversification benefits may weaken. Inflation, in particular, can alter correlations between asset classes, reducing the effectiveness of traditional portfolio structures.

Despite these complexities, bonds continue to serve several important functions within portfolios. They provide income, which can be particularly valuable for investors in retirement or those seeking regular cash flow. They offer capital preservation relative to equities, helping to reduce overall portfolio volatility. They also provide liquidity, allowing investors to rebalance portfolios or meet cash needs without disrupting long-term positions.

Bond ETFs enhance these benefits by making them more accessible. They allow investors to adjust exposure quickly, to diversify across different segments of the fixed income market, and to integrate fixed income strategies more seamlessly into broader portfolio frameworks.

Bond ETFs and the Australian Investor Landscape

The relevance of bond ETFs is particularly pronounced in Australia, where the investor base is characterised by a high level of self-directed activity and a strong presence of self-managed superannuation funds.

SMSFs, in particular, have become a major driver of ETF adoption. These investors often seek a balance between income generation and capital preservation, making fixed income a natural component of their portfolios. However, direct access to bond markets can be challenging, particularly for smaller funds.

Bond ETFs provide a practical solution. They allow SMSF trustees to gain exposure to diversified bond portfolios without the complexity of direct bond investing. They also offer liquidity, which is important for managing pension payments and meeting regulatory requirements.

The Australian Taxation Office has consistently emphasised the importance of diversification within SMSFs. In this context, bond ETFs can play a valuable role, complementing equity exposures and reducing overall portfolio risk.

The Structure of the Bond ETF Market: From Government Securities to Global Credit

To understand how investors should approach bond ETFs, it is necessary to move beyond definitions and examine the structure of the fixed income universe itself. Bond markets are not a single homogeneous asset class. They are composed of multiple segments, each with distinct risk characteristics, return drivers, and roles within a portfolio.

This structural diversity is reflected in the range of bond ETFs available to Australian investors, many of which can be explored at InvestmentMarkets.

What distinguishes sophisticated investors from casual participants is not simply whether they allocate to bonds, but how they differentiate between these segments.

Government Bonds: The Foundation of Defensive Investing

Government bonds sit at the core of fixed income markets. In Australia, these are primarily Commonwealth Government Securities issued by the federal government. They are widely regarded as having minimal credit risk, given the government’s ability to raise revenue through taxation and, if necessary, monetary policy.

This perceived safety has made government bonds a central component of defensive portfolio allocations.

However, safety does not equate to stability in all environments. Government bonds are highly sensitive to changes in interest rates. When rates rise, the value of existing bonds falls, as newer bonds are issued with higher yields. This dynamic has been particularly visible in recent years.

The Reserve Bank of Australia provides detailed data on government bond yields and market conditions.

During the period of rapid rate increases between 2022 and 2023, long-duration government bond ETFs experienced significant price declines. This surprised many investors who had historically associated bonds with stability.

The lesson is not that government bonds are risky in the same way as equities, but that their behaviour is shaped by macroeconomic forces, particularly interest rates and inflation expectations.

For investors using InvestmentMarkets, government bond ETFs often serve as the anchor within fixed income allocations, providing exposure to high-quality debt while complementing other, higher-yielding segments.

Corporate Bonds: Yield Enhancement and Credit Risk

While government bonds provide stability, corporate bonds introduce an additional dimension: credit risk.

Companies issue bonds to raise capital, and investors are compensated for the risk of default through higher yields. The difference between the yield on corporate bonds and government bonds is known as the credit spread, and it fluctuates based on economic conditions and investor sentiment.

During periods of economic expansion, credit spreads tend to narrow, reflecting confidence in corporate earnings and balance sheets. In contrast, during periods of stress, spreads widen as investors demand greater compensation for risk.

The International Monetary Fund has noted that corporate bond markets play an increasingly important role in global financial systems, providing both opportunities and risks for investors.

Corporate bond ETFs allow investors to access this segment in a diversified manner. Rather than selecting individual issuers, investors gain exposure to a broad portfolio of companies, reducing the impact of any single default.

For Australian investors, this segment is particularly relevant for income generation. Yields on corporate bond ETFs are typically higher than those on government bond ETFs, making them attractive to investors seeking regular distributions.

However, this higher income comes with trade-offs. Corporate bond ETFs are more sensitive to economic cycles and may behave more like equities during periods of market stress. Understanding this relationship is critical when constructing portfolios.

InvestmentMarkets provides access to a range of corporate bond strategies, enabling investors to compare yield, duration, and credit exposure.

Global Fixed Income: Diversification Across Economies

One of the most significant developments in bond ETF markets has been the expansion of global fixed income strategies. These ETFs provide exposure to bonds issued by governments and corporations across multiple countries, allowing investors to diversify beyond domestic markets.

This diversification can be valuable for several reasons.

First, interest rate cycles differ across economies. While the Reserve Bank of Australia may be tightening policy, central banks in other regions may be easing. This creates opportunities for investors to access different yield environments.

Second, global markets offer a broader range of issuers and sectors, increasing diversification.

However, global bond investing introduces currency risk. Movements in exchange rates can significantly impact returns, particularly when investing in unhedged products. To address this, many global bond ETFs are hedged to Australian dollars, reducing currency volatility.

Vanguard highlights the importance of currency considerations in global investing, noting that hedging can help stabilise returns for domestic investors.

At InvestmentMarkets, global bond ETFs represent an important category for investors seeking to expand their opportunity set while maintaining diversification.

Inflation-Linked Bonds: Protecting Purchasing Power

Inflation-linked bonds occupy a unique position within fixed income markets. Unlike traditional bonds, which pay fixed coupons, inflation-linked bonds adjust their payments based on changes in inflation.

This makes them particularly relevant in periods of rising prices.

The Australian Office of Financial Management provides insights into the structure of inflation-linked securities issued domestically.

During the inflation surge of recent years, these bonds gained renewed attention as investors sought to protect purchasing power. However, their behaviour can be complex. While they benefit from rising inflation expectations, they are still influenced by real interest rates, which can offset some of the inflation adjustment.

Bond ETFs that focus on inflation-linked securities allow investors to access this segment without needing to manage individual bonds.

High Yield Bonds: Income at the Expense of Stability

At the higher end of the risk spectrum sit high yield bonds, often referred to as ‘sub-investment grade’ or ‘junk’ bonds. These securities are issued by companies with lower credit ratings and therefore offer higher yields to compensate for increased risk.

High yield bond ETFs have characteristics that differ markedly from traditional fixed income.

Their returns are more closely linked to economic conditions and corporate performance. During periods of growth, they can deliver strong income and capital appreciation. However, during downturns, they may experience significant declines, behaving more like equities than defensive assets.

This dual nature makes them a specialised tool within portfolios, rather than a core defensive allocation.

How Bond ETFs Behave in Different Market Environments

Understanding the behaviour of bond ETFs requires an appreciation of how they respond to changing macroeconomic conditions. Unlike equities, where performance is largely driven by earnings growth and sentiment, bond markets are heavily influenced by interest rates, inflation, and credit conditions.

Interest Rate Cycles

Interest rates are the primary driver of bond prices. When central banks raise rates, existing bonds with lower yields become less attractive, leading to price declines. Conversely, when rates fall, bond prices tend to rise.

This relationship is fundamental, yet its implications are often misunderstood by investors.

The period from 2022 to 2023 provided a clear example. As central banks tightened policy to combat inflation, bond markets experienced one of their worst performances in decades. This challenged the perception of bonds as consistently stable assets.

However, it also reset the market. Higher yields mean that future returns from bonds are more attractive, particularly for long-term investors.

Inflation Dynamics

Inflation affects bond markets in multiple ways.

Rising inflation erodes the real value of fixed coupon payments, making bonds less attractive. At the same time, it often leads to higher interest rates, which further pressure bond prices.

However, once inflation stabilises and begins to decline, bonds can recover as interest rates peak and expectations shift.

The Reserve Bank of Australia provides ongoing analysis of inflation trends and their impact on financial markets.

Economic Growth and Credit Conditions

Corporate bond ETFs are particularly sensitive to economic conditions. During periods of strong growth, default risk is perceived to be low, and credit spreads tighten. This supports higher prices for corporate bonds.

In contrast, during recessions or periods of uncertainty, spreads widen, reflecting increased risk. This can lead to declines in corporate bond ETFs, even if government bond ETFs perform more defensively.

Source: RealInvestmentAdvice

Correlation with Equities

One of the key reasons investors allocate to bonds is diversification. Historically, bonds have exhibited low or negative correlation with equities, meaning they tend to perform differently during market downturns.

However, this relationship is not constant.

During inflation-driven environments, both equities and bonds can decline simultaneously, as seen in 2022. This highlights the importance of understanding the drivers of correlation, rather than assuming diversification benefits will always hold.

Source: Bogleheads

The CFA Institute emphasises that diversification must be considered in the context of changing market regimes.

The Risks of Bond ETFs: Understanding What Drives Volatility and Outcomes

One of the most persistent misconceptions in investing is that bonds are inherently ‘safe’. While fixed income securities are generally less volatile than equities over long periods, this characterisation can obscure the underlying risks that shape their performance.

Bond ETFs, in particular, have introduced a layer of accessibility that has broadened participation in fixed income markets. However, accessibility does not eliminate complexity. If anything, it increases the importance of understanding how these instruments behave.

The experience of recent years has underscored this point. During 2022, both equities and bonds declined simultaneously, challenging traditional assumptions about diversification. For many investors, this was their first direct encounter with the reality that bond prices can fall, sometimes materially, in response to macroeconomic shifts.

The CFA Institute has emphasised that fixed income investing requires a clear understanding of the drivers of return, noting that ‘interest rate sensitivity, credit exposure, and duration are fundamental to assessing risk in bond portfolios.’

Bond ETFs are no exception. Their risk profile is determined not by their label, but by the characteristics of the securities they hold.

Interest Rate Risk: The Dominant Force in Bond ETF Performance

The most significant risk affecting bond ETFs is interest rate risk.

Bond prices move inversely to interest rates. When rates rise, the value of existing bonds falls, as newer bonds are issued with higher yields. This relationship is foundational, yet its implications are often underestimated by investors.

The sharp increase in rates following the pandemic provides a clear illustration. As the Reserve Bank of Australia raised the cash rate from 0.10% to above 4%, yields across the bond market increased accordingly. Existing bond portfolios, including those held within ETFs, experienced price declines.

The Reserve Bank has noted that ‘longer-term bond yields rose significantly as markets adjusted to higher expected policy rates.’

The extent of these declines is largely determined by duration.

Bond ETFs with longer duration, such as those focused on long-dated government bonds, are more sensitive to interest rate changes. This means they experience larger price movements when rates rise or fall. Shorter-duration ETFs, by contrast, tend to exhibit greater stability.

This dynamic has become a focal point for investors, particularly in an environment where interest rate expectations remain uncertain.

Duration Risk and the Misinterpretation of ‘Defensive’ Assets

Closely related to interest rate risk is duration risk, which measures how sensitive a bond or bond portfolio is to changes in interest rates.

The concept is straightforward in principle but often misunderstood in practice.

A bond ETF with a duration of seven years, for example, may experience a price decline of 7% if interest rates rise by one percentage point. This sensitivity increases with longer durations, meaning that long-term bond ETFs can exhibit meaningful volatility.

This has led to a reassessment of what constitutes a ‘defensive’ asset.

Government bond ETFs, often perceived as the safest segment of fixed income, can still experience significant short-term declines if they are exposed to long-duration securities. This was evident in the recent rate cycle, where some long-duration government bond ETFs delivered negative returns despite their high credit quality.

Without understanding duration, it is easy to misinterpret short-term performance and make suboptimal allocation decisions.

Credit Risk: The Trade-Off Between Yield and Stability

While interest rate risk affects all bond ETFs, credit risk is specific to those that invest in corporate or lower-rated bonds.

Credit risk reflects the possibility that an issuer may fail to meet its obligations. Investors are compensated for this risk through higher yields, which is why corporate bond ETFs typically offer higher income than government bond ETFs.

However, this higher yield comes with increased sensitivity to economic conditions.

During periods of economic expansion, corporate bonds tend to perform well. Default risk is perceived to be low, and credit spreads, the difference between corporate and government bond yields, narrow. This supports higher prices and stable income.

In contrast, during economic downturns, credit spreads widen as investors demand greater compensation for risk. This can lead to price declines in corporate bond ETFs, even if government bond ETFs remain relatively stable.

The International Monetary Fund has highlighted the importance of monitoring credit conditions, noting that corporate bond markets can amplify financial stress during periods of economic uncertainty.

For investors, the key is to recognise that higher yield is not simply a benefit. It is a reflection of underlying risk.

Liquidity Risk and Market Functioning

One of the advantages of bond ETFs is their liquidity. They can be traded on the ASX throughout the day, providing flexibility that is not always available in traditional bond markets.

However, this liquidity is not absolute.

During periods of market stress, trading conditions can become more volatile. Bid-ask spreads may widen, and ETF prices can deviate from the net asset value of their underlying holdings. While these deviations are typically temporary, they can create challenges for investors seeking to transact during turbulent conditions.

The Australian Securities Exchange notes that ETFs rely on market makers to provide liquidity, and while this system is generally robust, it is influenced by broader market conditions.

It is important to emphasise that these risks are not unique to ETFs. They reflect the underlying dynamics of bond markets themselves. However, the ETF structure can make these dynamics more visible to investors.

Currency Risk in Global Bond ETFs

For investors allocating to global bond ETFs, currency risk introduces an additional layer of complexity.

Exchange rate movements can have a significant impact on returns, particularly for unhedged products. A strengthening Australian dollar, for example, can reduce the value of foreign bond holdings when converted back into local currency.

To mitigate this risk, many global bond ETFs are hedged to Australian dollars. Hedging reduces currency volatility, but it is not without cost, and it may limit potential gains from favourable currency movements.

Vanguard highlights that currency hedging can help stabilise returns for domestic investors, particularly in fixed income portfolios where volatility is typically lower.

Investors must therefore decide whether to accept currency risk in exchange for potential diversification benefits, or to prioritise stability through hedged exposures.

Behavioural Risk: The Gap Between Expectations and Outcomes

Perhaps the most underestimated risk in bond ETF investing is behavioural.

Investors often approach bonds with expectations shaped by historical narratives rather than current market realities. The belief that bonds will always provide stability and positive returns can lead to disappointment when market conditions change.

The experience of 2022 is a case in point. As both equities and bonds declined, some investors reacted by reducing their fixed income exposure at precisely the wrong time, locking in losses and missing the subsequent recovery in yields.

Behavioural finance research suggests that investors are prone to loss aversion, meaning they are more sensitive to losses than gains. This can lead to reactive decision-making, particularly during periods of volatility.

The CFA Institute has emphasised the importance of aligning investment strategies with behavioural considerations, noting that well-constructed portfolios should help investors ‘maintain discipline through market cycles.’

Bond ETFs, when used correctly, can support this discipline. However, this requires a clear understanding of their role and limitations.

Putting Risk into Context

While the risks associated with bond ETFs are real, they must be considered in context.

Compared to equities, bond ETFs generally exhibit lower volatility and provide more predictable income. Compared to private credit, they offer greater liquidity and transparency. Compared to cash, they provide higher potential returns over longer time horizons.

The objective is not to eliminate risk, but to manage it effectively.

Bond ETFs in Portfolio Construction: From Theory to Practice

The role of bond ETFs within portfolios cannot be understood in isolation. It must be considered within the broader framework of asset allocation.

In traditional portfolio models, bonds serve as a counterbalance to equities. They provide income and reduce volatility, allowing investors to maintain exposure to growth assets while managing risk.

Your benchmark document highlights how institutional investors incorporate different asset classes to improve risk-adjusted returns. Bond ETFs play a similar role within modern portfolios.

However, the way investors use bonds has evolved.

Rather than simply allocating a fixed percentage to ‘bonds’, investors are increasingly segmenting their exposure.

They may combine:

- Government bond ETFs for stability;

- Corporate bond ETFs for income;

- Global bond ETFs for diversification;

- Inflation-linked ETFs for protection.

This layered approach reflects a more sophisticated understanding of fixed income.

InvestmentMarkets is uniquely positioned to support this approach by enabling investors to compare different strategies and products within a single platform.

Income Generation and Cash Flow Management

For many investors, particularly retirees and SMSFs, income is the primary objective.

Bond ETFs provide regular distributions derived from coupon payments. This income can be used to fund living expenses, reinvested to compound returns, or combined with other income-generating assets such as dividend-paying equities.

Compared to term deposits, bond ETFs offer flexibility. Investors are not locked into fixed terms and can adjust their exposure as market conditions change.

However, this flexibility comes with variability. Unlike term deposits, where returns are fixed, the income from bond ETFs can fluctuate based on market conditions and portfolio composition.

Risk Management and Portfolio Stability

Beyond income, bond ETFs play a critical role in managing portfolio risk.

By allocating to assets that behave differently from equities, investors can reduce overall volatility. This is particularly important during market downturns, where losses in equities can be partially offset by stability or gains in fixed income.

However, as recent history has shown, this relationship is not guaranteed. Investors must consider the specific characteristics of their bond allocations, including duration and credit exposure.

Integrating Real Bond ETF Examples: From Theory to Practical Portfolio Decisions

A defining feature of high-quality investment research is the ability to bridge theory and implementation. While understanding duration, yield, and credit risk is essential, investors ultimately make decisions based on available products. In the Australian market, a relatively concentrated group of bond ETFs provides the foundation for most portfolios.

The most widely used ETFs broadly fall into three categories: diversified composite bond funds, government bond funds, and corporate or credit-focused strategies. Each plays a distinct role within a portfolio, and understanding their differences is critical.

The Core Allocation: Broad Market Bond ETFs

For many investors, the starting point is a broad, diversified bond ETF that provides exposure to the overall Australian fixed income market.

One of the most prominent examples is the iShares Core Composite Bond ETF (IAF), which provides exposure to investment-grade Australian bonds across government, semi-government, and corporate issuers. It is widely regarded as a ‘core’ allocation within portfolios.

IAF holds hundreds of underlying securities and is designed to track the Bloomberg AusBond Composite Index, making it a comprehensive representation of the domestic bond market. It is also one of the largest and most liquid bond ETFs in Australia, with assets exceeding $2 billion and a running yield of approximately 3%.

A closely related alternative is the Vanguard Australian Fixed Interest Index ETF (VAF), which tracks a similar index and provides comparable exposure. Both funds have seen fees compress significantly in recent years, with management costs falling to around 0.10%, reflecting increasing competition in the ETF market.

These products are often used as the foundation of fixed income allocations. Their diversified nature reduces exposure to any single issuer or segment, while still providing meaningful income and duration exposure.

For investors navigating the InvestmentMarkets platform, these ETFs typically appear as central comparison points within the bond ETF category.

Government Bond ETFs: Defensive Anchors with Duration Exposure

Where investors seek a more explicitly defensive allocation, government bond ETFs provide targeted exposure to sovereign debt.

The Vanguard Australian Government Bond Index ETF (VGB) is one of the most widely recognised examples. It invests in high-quality bonds issued by the Australian government and state authorities, offering exposure to assets traditionally considered among the safest in the market.

Similarly, the BetaShares Australian Government Bond ETF (AGVT) focuses on longer-duration government bonds, typically with maturities between seven and twelve years. This structure increases sensitivity to interest rate movements, which can amplify both gains and losses depending on the direction of rates.

The distinction between these products is subtle but important. While both provide exposure to government bonds, their duration profiles influence how they behave in different environments. AGVT, with its longer duration, tends to exhibit greater volatility when interest rates change, whereas shorter-duration strategies may offer more stability.

The performance of government bond ETFs in recent years has highlighted this dynamic. As interest rates rose sharply, many long-duration funds experienced price declines, even as they continued to generate income. This has led to a broader reassessment of what ‘defensive’ means in a modern portfolio context.

Recent market commentary has noted that some investors were surprised by the extent of these declines, with government bond ETFs delivering limited capital growth over multi-year periods despite consistent distributions.

This reinforces a critical insight: bonds are not risk-free. Their behaviour is shaped by macroeconomic conditions, and investors must align their expectations accordingly.

Corporate Bond ETFs: Balancing Income and Economic Sensitivity

Beyond government bonds, corporate bond ETFs introduce a different set of characteristics.

Funds such as the BetaShares Australian Investment Grade Corporate Bond ETF (CRED) and similar strategies provide exposure to bonds issued by companies with relatively strong credit ratings. These ETFs typically offer higher yields than government bond funds, reflecting the additional risk associated with corporate issuers.

The structure of these funds often includes a concentrated portfolio of investment-grade bonds, with yields that can exceed 4 to 5% depending on market conditions.

This makes them particularly attractive to income-focused investors.

However, the trade-off is increased sensitivity to economic cycles. During periods of economic strength, corporate bond ETFs can perform well, benefiting from tightening credit spreads and stable default expectations. During downturns, however, spreads can widen, leading to price declines.

This dual nature means that corporate bond ETFs often behave as a hybrid between traditional fixed income and equities.

These strategies provide an important complement to government bond exposure, allowing investors to enhance income while maintaining diversification.

Liquidity, Fees and Market Structure

One of the most practical considerations for investors is liquidity.

In the Australian market, ETFs such as VAF and IAF are among the most liquid bond ETFs.

Higher liquidity reduces transaction costs and improves execution, making these funds more suitable for both long-term investors and those implementing tactical strategies.

Fees have also declined significantly. The compression of management costs across major bond ETFs reflects increasing competition and scale within the industry. For investors, this is a meaningful benefit, as lower fees directly improve net returns over time.

Advanced Portfolio Construction: Combining Bond ETF Strategies

The integration of multiple bond ETF types within a single portfolio represents a key evolution in investor behaviour.

Rather than treating fixed income as a single allocation, sophisticated investors increasingly construct layered exposures.

A portfolio may combine a core allocation to a broad bond ETF such as VAF or IAF with a satellite allocation to government bonds for stability and corporate bonds for yield enhancement. Global bond ETFs can be added to diversify interest rate exposure, while inflation-linked securities provide protection against rising prices.

This approach reflects a shift towards more granular asset allocation.

It is also consistent with institutional practices. Large pension funds and endowments have long segmented their fixed income exposures to manage risk and optimise returns. Retail investors now have the tools to adopt similar strategies through ETFs.

InvestmentMarkets facilitates this approach by enabling investors to compare and analyse different bond ETF categories within a unified framework.

Bond ETFs and Market Reality: Managing Expectations

One of the most important themes emerging in recent years is the gap between investor expectations and actual outcomes.

Many investors entered bond ETFs with the assumption that they would provide stable returns and consistent capital preservation. While this has historically been true over long periods, the experience of rising interest rates has demonstrated that short-term outcomes can differ significantly.

The underperformance of some government bond ETFs during the recent rate cycle has been widely discussed in the financial press, highlighting the importance of understanding duration and interest rate sensitivity.

This does not diminish the value of bond ETFs, but it underscores the need for education.

Investors must recognise that:

- Bonds can decline in value when rates rise;

- Income does not guarantee positive total returns;

- Diversification benefits vary depending on macroeconomic conditions.

These insights are central to building resilient portfolios.

Limited")