The Water Is Slowly Warming: Systemic Risks Investors Are Underpricing

Simon Turner

Wed 4 Mar 2026 8 minutesMost investors tend to think of systemic risk as something that arrives with a bang, like a banking crisis, a pandemic, or a war. Increasingly, the more realistic systemic dangers are slower to gauge and harder to price. They are an ominous set of interconnected and interacting stresses that have the potential to degrade the very conditions required for markets to compound at all.

What’s the point in just focusing on chasing alpha when the beta remains vulnerable and unprotected?

The Foundations of Markets Matter

Markets are so dynamic, it’s easy to forget that they’re built upon systemic foundations; real-world foundations that investors tend to assume will always be there.

In particular, there are four foundations that are essential for markets to remain functional:

A relatively stable climate.

The health and abundance of nature.

Social cohesion.

Functioning institutions.

You’ll notice that the first three items on the list, climate, nature, and social cohesion, are all public goods. That means they benefit humanity at large, although no one pays for these benefits directly.

Herein lies a structural challenge. Any single individual is incentivised to take more than their fair share from these freely available public goods. It’s a classic example of the tragedy of the commons.

Markets reflect this incentive problem. The costs of taking from the commons are generally externalised, delayed, or pushed onto those with the least political and economic power, while the short-term gains remain privately captured.

This dynamic tends to eat away at the foundations of the system without the global population’s awareness, making the system more fragile than many understand.

Nature: There for All, Protected by No One

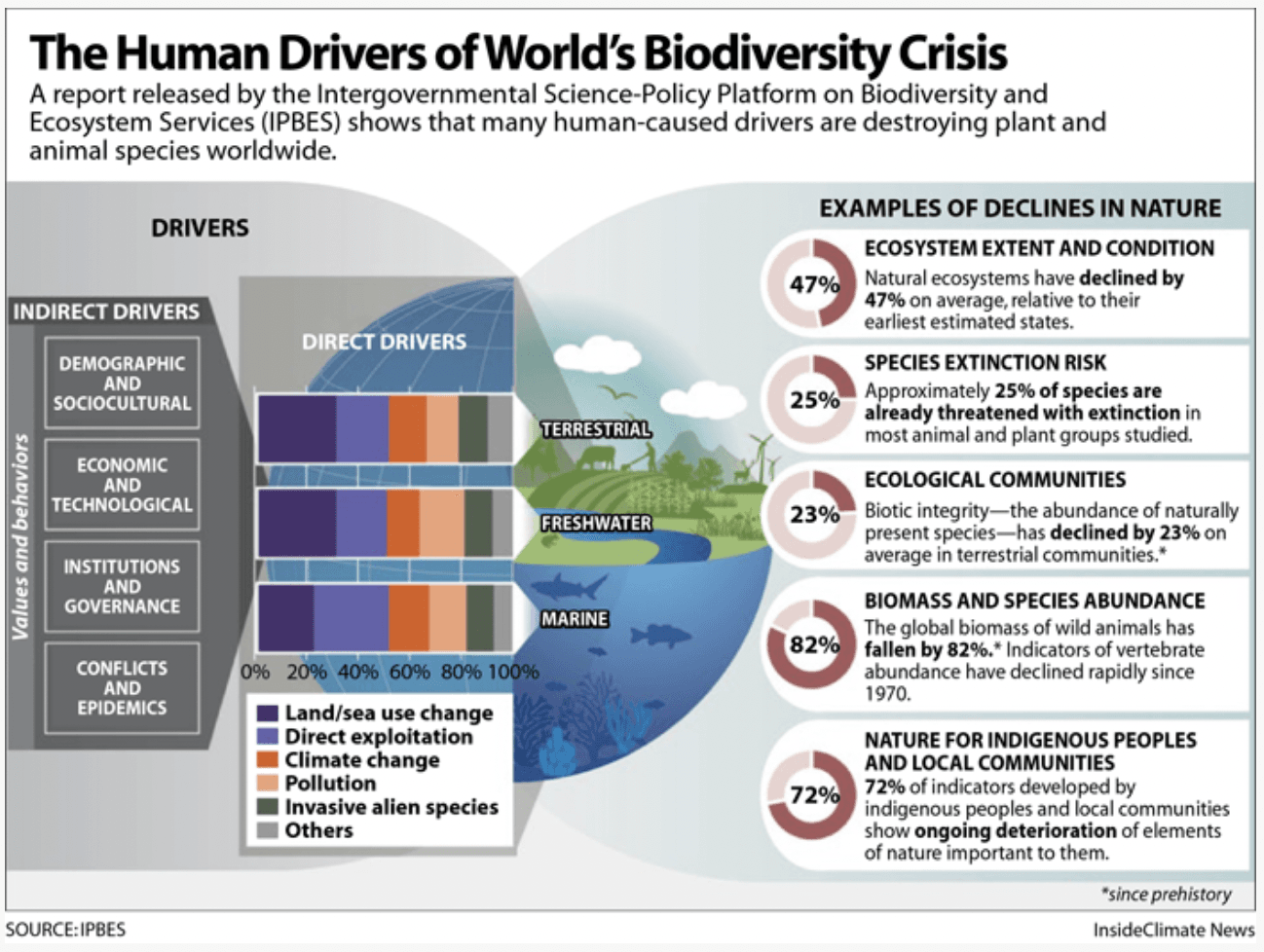

Most people would agree humans are dependent on nature for our long-term health and prosperity. Yet, the biodiversity crisis driven by the tragedy of the commons has ravaged the natural world.

The IPBES Global Assessment warns that around one million species (25% of all species) are threatened with extinction, many within decades. The list of biodiversity challenges goes on:

Whilst most management teams probably view this as a sad state of affairs with moral implications for poachers and the like, few will be viewing it as the balance-sheet issue it really is.

Pollination, water regulation, soil health, fisheries, and disease control are forms of natural infrastructure that the global economy can’t replicate at scale.

In other words, this matters for all companies. When nature degrades, supply chains become more unpredictable and volatile, while insurance losses become less diversifiable.

Of course, the fundamental issue is that nature creates value for all but that value isn’t being effectively priced by markets. Hence, everything nature delivers to humanity is being captured for free but is ignored on corporate balance sheets.

As the Taskforce on Nature-related Financial Disclosures has been saying for years, nature is a set of ‘dependencies, impacts, risks and opportunities’ that capital providers should be able to assess and price.

None of this is new news. The fact that this is still an emerging theme speaks to the nature of this systemic risk: it is largely ignored and invisible in the corporate world.

Climate Risk Translates into Healthcare Outcomes

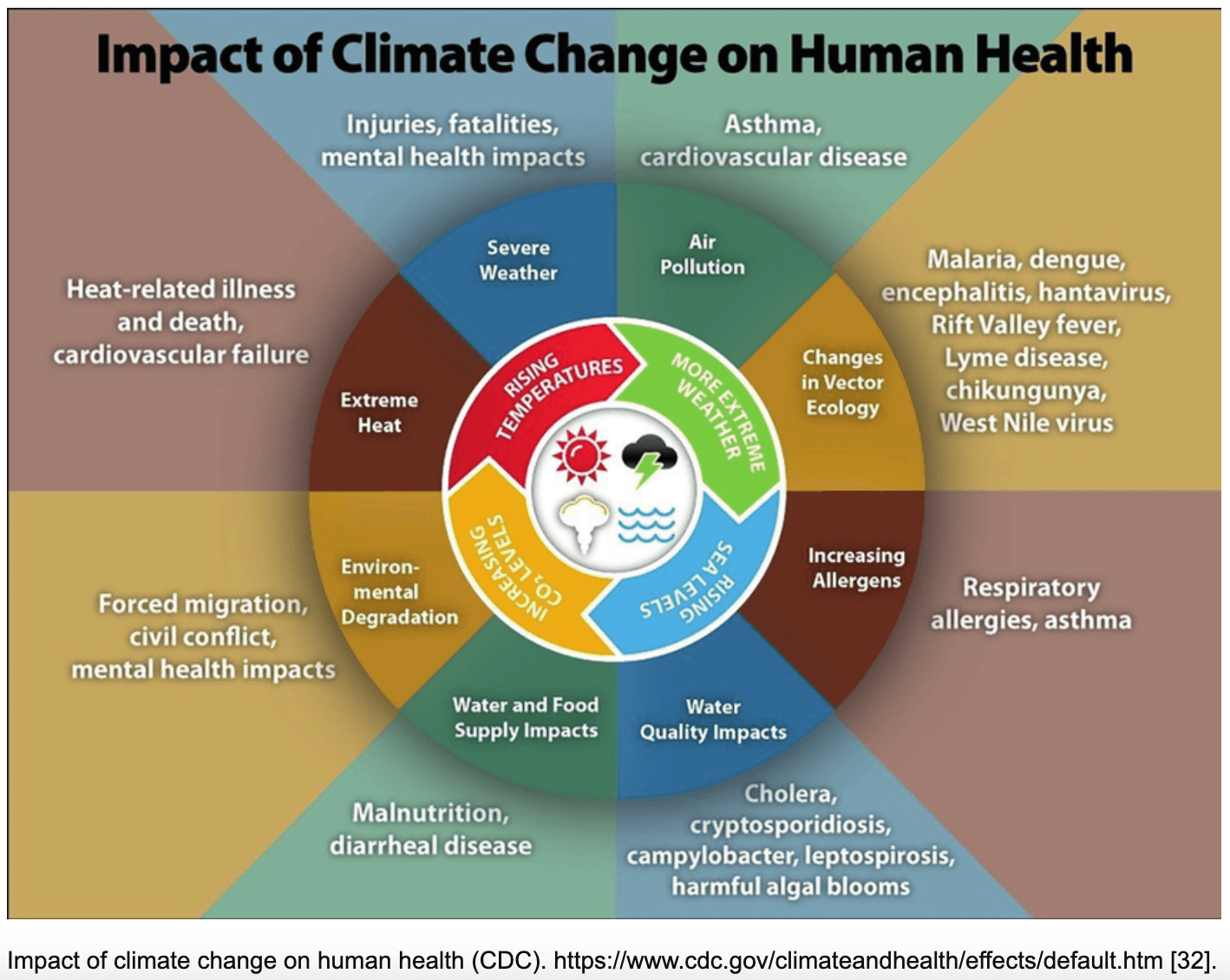

Then there’s climate change. This is a more familiar corporate risk, but is often treated as an isolated theme rather than a systemic amplifier.

In reality, climate change is deeply connected to the global economy, and particularly to human health outcomes. For example, rising air pollution is associated with rising asthma and cardiovascular disease incidence. Extreme heat is associated with heat-related illness and cardiovascular failure. The list goes on.

There’s no shortage of voices highlighting these connections between climate change and the things that matter for investors.

The RBA has warned that climate change could affect asset prices by reducing future cash flows and increasing volatility, with implications for collateral values and lender losses.

APRA’s climate guidance also warns that climate risk belongs inside existing governance and risk management, rather than being treated as a discretionary ESG overlay.

The World Bank has also tied climate impacts directly to poverty outcomes, noting that without action climate change could push around 100 million more people into extreme poverty by 2030.

The issue for investors is that rising poverty is linked to weaker health systems, lower productivity, higher migration pressure, and political instability, all of which could widen equity market risk premia.

It’s hard to know when this systemic risk will impact investment markets given the long-term timeframes involved, but it’s important to understand that it is structural in nature and on the rise.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Inequality Amplifies Systemic Risks

The missing link that makes climate and nature risks even more systemic is inequality.

This is a significant issue, and it is becoming more significant each year.

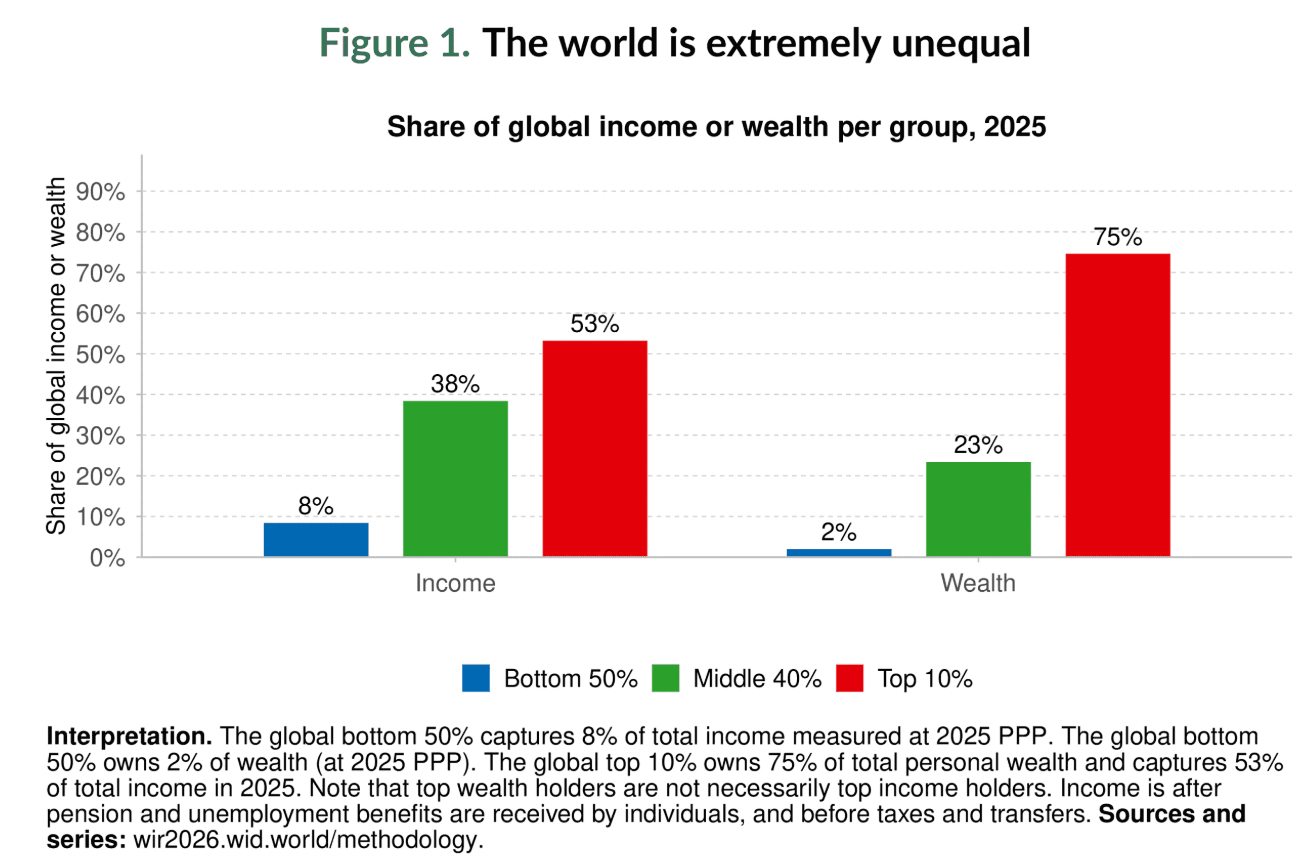

By way of background, the World Inequality Report estimates that the richest 10% of the population receive 52% of global income, while the poorest half receive only 8-8.5%.

This extreme inequality is amplifying the risk of coordination failure at a global level. Highly unequal societies tend to find it harder to sustain long-horizon policies that require near-term sacrifice for shared future benefits.

Inequality can also harden political polarisation, reduce institutional trust, and increase the odds of policy whiplash, all of which are likely to make the global decarbonisation pathway less orderly.

In other words, rising inequality could amplify the above-mentioned systemic risks, thereby turning a managed transition into a disorderly one. Markets are arguably priced for the former.

Geopolitical Fragmentation Acts as an Accelerant

Rising geopolitical fragmentation is acting as an accelerant of all these interconnected systemic risks.

When trust between countries and regions breaks down, cooperation on climate finance, technology transfer, biodiversity protection, and even shared externality measurement standards becomes harder.

Rising fragmentation makes supply chains less efficient and more shock-prone, which can amplify inflation volatility and raise the political appeal of protectionism.

On that note, the IMF has warned that the economic costs of rising fragmentation could be material, with estimates ranging from 0.2% of global GDP in mild scenarios up to 7% in more extreme ones.

Hence, rising geopolitical fragmentation is a big deal for investors.

It also changes the investment opportunity set. In particular, higher defence spending, duplicated industrial capacity, and higher energy security costs are already reshaping which sectors are long-term winners and losers.

Investor Takeaways

For investors, the question is how to position your portfolio without pretending you can diversify away these deeply entrenched systemic risks. In other words, how can you make your beta more resilient?

The key is to be aware of these systemic risks and be intentional about side-stepping them.

For example:

To reduce your exposure to climate risk and high-carbon business models, ETFs such as BetaShares Global Sustainability Leaders ETF (ETHI) and BetaShares Australian Sustainability Leaders ETF (FAIR) are solid options.

If you want a more explicit transition tilt, VanEck Global Clean Energy ETF (CLNE) can provide this.

If you’re concerned about how climate shocks and transition costs may destabilise the bond market, consider a green bond option such as BetaShares Global Green Bond Currency Hedged ETF (GBND).

If you think geopolitical fragmentation will structurally raise defence demand, it may be prudent to allocate to defence-themed exposures such as BetaShares Global Defence ETF (ARMR) and VanEck Global Defence ETF (DFND).

None of these funds will solve the glaring global systemic risks, but they make explicit what is otherwise implicit.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Be Conscious for Your Portfolio and the Market

It’s time to treat climate, nature, inequality, and geopolitical fragmentation as linked variables, rather than separate themes. It’s important to be aware that these largely invisible market foundations are gradually being degraded. Because it won’t matter until it suddenly will.

So stress test your portfolio against scenarios where these systemic shocks cluster rather than diversify.

Focus on funds and ETFs that can articulate their exposure to physical climate risk, transition risk, and nature dependencies, and that are already utilising credible disclosure frameworks rather than marketing language.

Avoid building a portfolio that relies on permanent policy paralysis to drive its near-term returns, because the longer collective action fails, the higher the probability of an abrupt, disorderly correction.

Finally, remember that protecting your beta, and everyone else’s, is ultimately about protecting the preconditions for compounding. Those preconditions include social cohesion and the health of the natural world, not just interest rates and earnings.

Funds Mentioned

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.