New Rules: Semiconductors Move From Cyclical To Structural

Billy Leung

Tue 19 May 2026 8 minutesThe first phase of the AI trade was about compute, but the second phase is being driven by constraints. Over the past two years, leadership was concentrated in a small group of AI chip designers and hyperscalers as demand for training and inference accelerated, which made sense in the early stages of a new technology cycle. As AI systems scale, however, the limits of the existing infrastructure are starting to show. Memory supply is tightening, storage demand is rising sharply, and electricity requirements for data centres are climbing at a pace the grid was never designed to handle1. These are not isolated developments, but early signals that AI is moving beyond a pure compute story and into a full infrastructure build-out across both semiconductors and physical assets.

Memory is the first visible pressure point

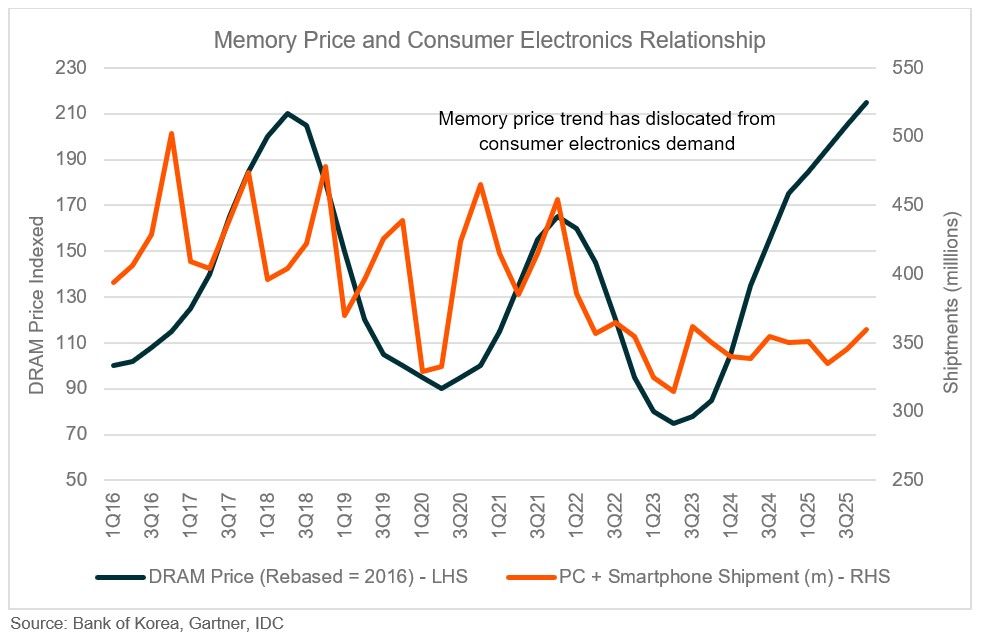

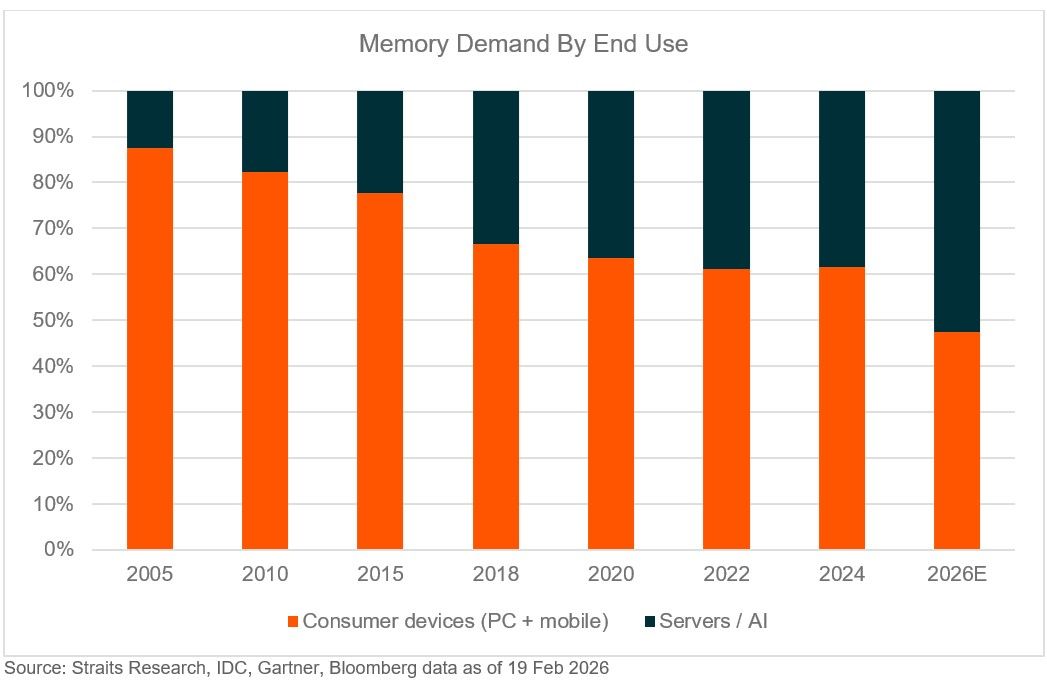

The clearest signal that the AI cycle is entering a new phase is coming from the memory market. In past cycles, memory demand was dominated by consumer devices, which made pricing highly cyclical and tied to handset and PC shipments. This time, the strongest demand is coming from AI servers, where memory and storage requirements are materially higher than in traditional workloads2. As a result, memory pricing is starting to move independently of consumer device volumes, signalling a shift away from the old consumer-driven cycle and toward a more structural, infrastructure-led demand profile.

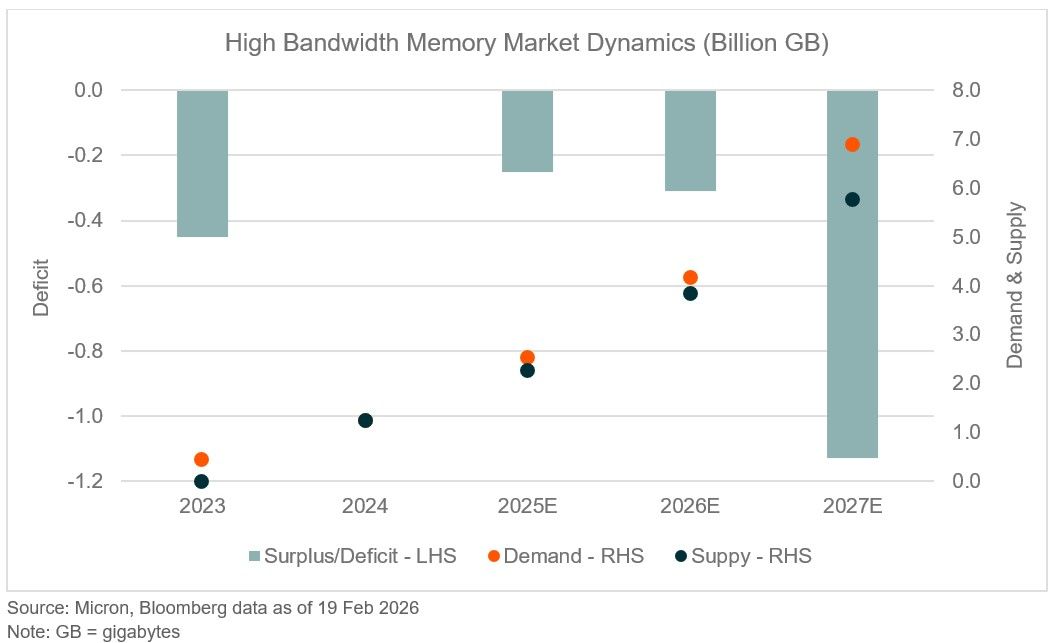

High-bandwidth memory (HBM) sits directly alongside advanced GPUs and custom accelerators, which means it scales with the complexity of the models themselves. As model sizes increase and inference becomes more widespread, memory capacity is emerging as a key limiting factor. Supply is expected to remain tight through at least 20273, while the HBM market is projected to grow at close to an 80% annual rate over the next several years4. At the same time, enterprise Solid State Drive (SSD) demand linked to AI inference is forecast to expand at roughly 50% per year, with storage requirements in AI servers growing more than twice as fast as in traditional systems5.

Pricing is already responding to these pressures. DRAM and NAND average selling prices are expected to rise by roughly 70–80% into 2026, driving a step-up in margins and earnings across memory suppliers6. The effects are not confined to the memory companies themselves. In some enterprise hardware products, memory now accounts for roughly 10–25% of the total bill of materials7, so rising DRAM prices are beginning to squeeze margins and influence build decisions. On the consumer side, memory availability has started to constrain low-end handset production as supply is increasingly prioritised toward AI and data centre customers.

When a single component begins to affect both enterprise margins and consumer output, it is a clear signal that the constraint is real. Memory is no longer just participating in the AI cycle but is shaping the pace and direction of the entire build-out.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Semiconductors are becoming infrastructure

The memory shortage also highlights a broader shift across the semiconductor sector. It is no longer behaving purely like a cyclical technology segment tied to consumer demand and is increasingly taking on the characteristics of core infrastructure within the AI build-out.

Every AI system depends on a stack of semiconductor components, including compute chips, high-bandwidth memory, advanced packaging, interconnects, and storage. As AI demand accelerates, pressure moves through each of these layers, and the opportunity is no longer confined to one company or one segment. Instead, it is spreading across the entire semiconductor supply chain.

This cycle also differs from past memory booms. Capacity growth has been more measured, while technology transitions are limiting effective supply increases. Capital intensity in NAND is expected to remain lower than in DRAM over the next few years, and revenue per unit of capacity is projected to rise into the second half of the decade. That combination supports stronger pricing and a longer earnings cycle, making semiconductors look less like a short-term consumer rebound and more like a multi-year infrastructure build-out8.

As demand becomes more closely tied to data centre build-outs than to handset refresh cycles, the semiconductor sector begins to take on the characteristics of infrastructure. Revenue streams become increasingly linked to capital expenditure cycles, and the investment horizon shifts from short consumer-led swings to longer, more structural build-outs.

Power is the next constraint

As AI systems scale, the next bottleneck moves beyond the server and into the grid. AI workloads consume far more electricity than traditional computing tasks, and data centre capacity is being expanded rapidly to meet demand.

Global investment in power infrastructure has already reached around US$1.5 trillion per year, while data centre capital expenditure is expected to approach US$3 trillion by the end of the decade. Electricity demand from data centres is projected to increase by more than 100 gigawatts over the same period, requiring new generation capacity, grid upgrades, cooling systems, and energy storage. In other words, AI is not just a technology cycle. It is an energy and industrial cycle as well9.

The same logic that drove the first phase of the AI trade is now pushing capital into physical infrastructure. As compute and memory scale, power becomes the next binding constraint. Data centres cannot operate without reliable electricity, and the scale of AI workloads is forcing utilities and grid operators to accelerate investment.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

A two-layer AI infrastructure opportunity

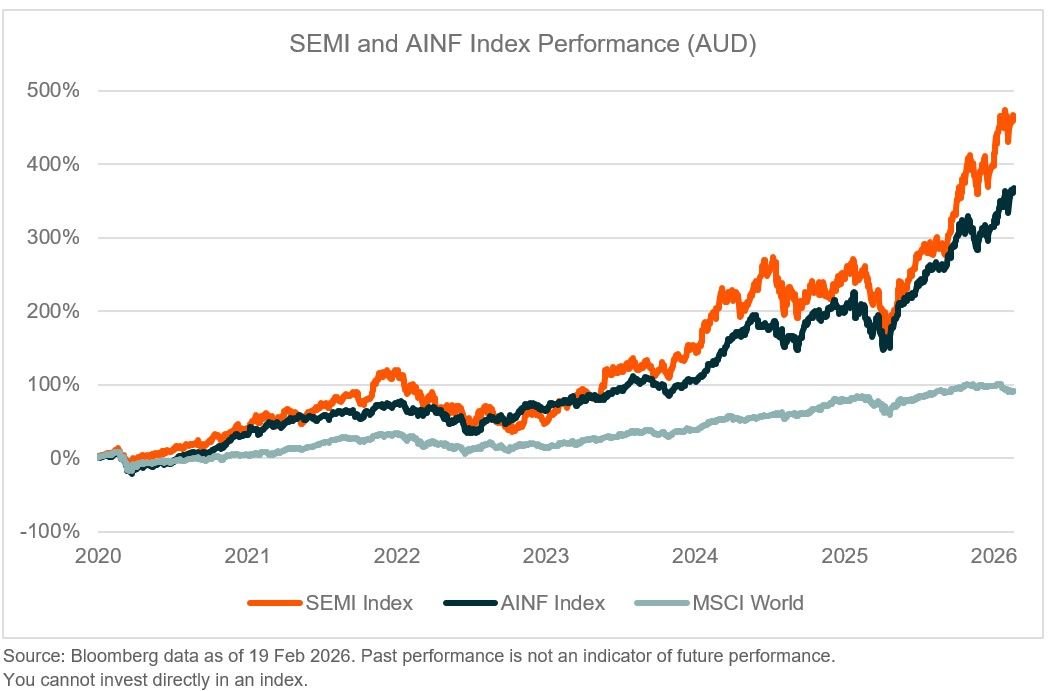

The AI build-out is now spreading across two distinct layers. The first is the digital layer, which sits within the semiconductor ecosystem and includes memory, foundries, chip designers, equipment, and advanced packaging. This is the foundation of AI compute, and the area where the first phase of the AI cycle was concentrated, represented across the semiconductor value chain in exposures such as the Global X Semiconductor ETF (SEMI).

The second is the physical layer, which allows that compute to operate at scale. This includes electricity generation, grid upgrades, data centres, cooling systems, and the broader industrial capacity required to support them. As AI workloads grow, this layer becomes just as critical as the chips themselves, which is the focus of the Global X Artificial Intelligence Infrastructure ETF (AINF).

Memory shortages are the clearest signal that the system is already under pressure. Demand is running ahead of supply across multiple parts of the stack, forcing capital to move beyond compute and into the infrastructure required to support it. For investors, the implication is that the AI opportunity is broadening. It is no longer confined to a handful of chip designers, but now spans both the semiconductor value chain and the infrastructure that powers it.

The next phase of the AI cycle sits at the intersection of semiconductors and physical infrastructure. As the bottlenecks move from compute to memory, and from memory to power, the opportunity naturally extends across both layers of the AI build-out.

About the Author: Billy joined Global X in 2024 and is responsible for investment research and ETF analysis in the technology sector. Billy has over a decade of experience in financial services, focusing on equities and technology, previously working as Equity Analyst at Optiver in Sydney, and was the Director of Equity Research for China Internet at Haitong International in Hong Kong. Billy has been a top ranked equity analyst for regional software and internet by Asiamoney. Billy holds a Bachelor of Commerce from the University of Melbourne and is a qualified CPA Australia.

1Schneider Electric, The 5 trends that will shape the scale of AI in 2026, 15 Dec 2025

2The Straits Times, Rampant AI demand for memory is fuelling a growing chip crisis, 16 Feb 2026

3McKinsey, Generative AI spurs new demand for enterprise SSDs, 3 Dec 2024

4SemiAnalysis, Scaling the Memory Wall: The Rise and Roadmap of HBM, 11 Aug 2025

5Rand Technology, How AI Is Reshaping the Memory Supply Chain, 10 Dec 2025

6S&P Global, AI Memory boom squeezes legacy DRAM supply, 29 Jan 2026

7Wccftech, Memory & NAND Prices Surged over 90% In Q1 2026, 9 Feb 2026

8Astute Group, AI-driven memory crunch set to reshape electronics market, 14 Feb 2026

9McKinsey & Company, The next big shifts in AI workloads and hyperscaler strategies, 17 Dec 2025

Disclaimer: This document is issued by Global X Management (AUS) Limited (“Global X”) (Australian Financial Services Licence Number 466778, ACN 150 433 828) and Global X is solely responsible for its issue. This document may not be reproduced, distributed or published by any recipient for any purpose. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.