The Misunderstood Miner

Chris Watson

Tue 24 Feb 2026 8 minutesOpen a financial news app and you’ll be greeted with headlines of quarterly earnings misses, monthly economic data prints, and excitement about a 10-week trading update, with share prices swinging around in response. A focus on the short-term—next year’s earnings or the next Fed meeting—is a hallmark of investment markets. It is also, in our view, a potential pitfall for investors because it can take one’s attention away from the major structural changes underway that may ultimately have a greater impact on future investment returns. Think of the airline passenger noticing the left-to-right bumps from turbulence while forgetting that they are travelling forward at 900 kilometres per hour. Companies or even whole industries may be undergoing significant changes in plain sight, that go largely unnoticed as the next earnings report takes the spotlight. A great illustration of this, in our view, is the transformation happening at South32, a meaningful position in the Contrarius Australia Equity Fund.

Background

In 2015, BHP spun out a collection of mining assets that it no longer wanted into a new entity called South32. These assets were burdened with some combination of higher costs, shorter mine life, riskier jurisdiction, or thornier rehabilitation issues. A truly diversified miner, South32 had so many moving parts that the market likely found it overwhelming to monitor and difficult to value. First impressions matter, and many market participants likely continue to view South32 as a complicated mix of BHP’s leftovers. Look more closely, and one finds a company undergoing a transformation.

Simplification

We’ll start with the most obvious change: simplification. Gone are South32’s coal mining operations in South Africa and Australia. These required significant reinvestment, carried meaningful rehabilitation costs, were the biggest source of greenhouse gas emissions, and, in the case of the Australian assets, were sold at a reasonable price. Gone too are its manganese refineries in Tasmania and South Africa as well as a Colombian nickel operation struggling to compete with Indonesian producers. Company-wide staff numbers are down from over 15,000 to about 8,000. These actions go a long way towards simplifying a complex company, however simplification is only part of the story.

Portfolio Shifts

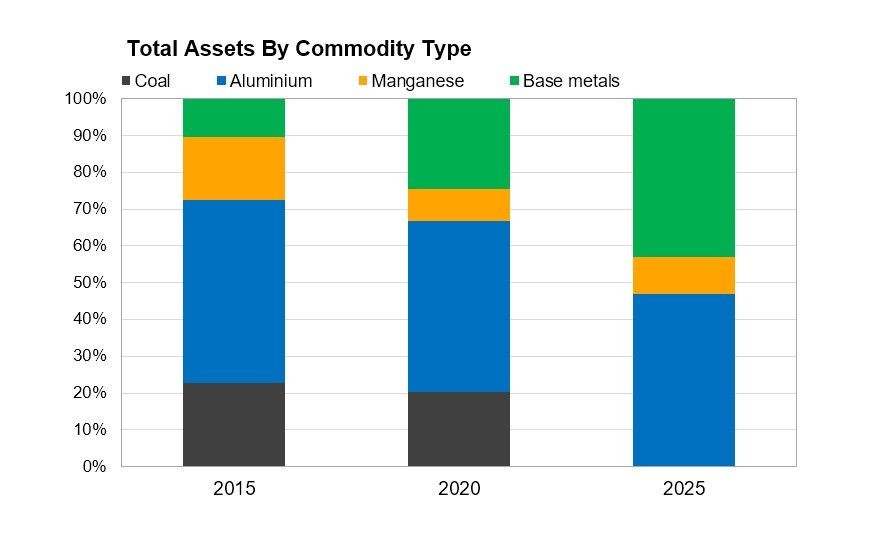

Since 2015, South32 has added three base metals operations to its portfolio—Hermosa, Ambler, and Sierra Gorda—which share crucial common characteristics. All three have long potential operating lives, are located in favourable jurisdictions, and are focused on the metals required for decarbonisation (e.g. copper, zinc and silver). Grouping the assets on South32’s balance sheet by commodity type, one can clearly see the shift away from carbon-intensive assets and towards “green metals” over time, a trend that is likely to continue as investment in these three assets progresses.

This pivot is timely. The global energy transition is creating a synchronized boom in green metal requirements that existing supply chains appear ill-equipped to meet. Copper and aluminium—key components in electricity grids, EVs, and renewables—are facing looming structural deficits. Industry forecasts suggest a copper shortfall of millions of tonnes by 2030, while the aluminium market is expected to tighten significantly as early as 2026 due to power constraints and rising demand from the auto and solar sectors. Silver has been in a structural deficit for a number of years driven by rising industrial demand, notably from silver-intensive solar panels. By divesting coal and adding to its copper, zinc, silver and aluminium investments, South32 has repositioned its portfolio for a decarbonising world.

At the same time, demand is being fuelled by the advancement of AI technologies, of which a metal such as copper is a physical enabler. It is estimated that data centres require roughly 27 tonnes of copper per megawatt of capacity for cooling and power distribution. Ultimately AI-driven productivity gains may translate into stronger economic growth, which we think bodes well for South32’s growing exposure to copper, zinc, silver, and aluminium.

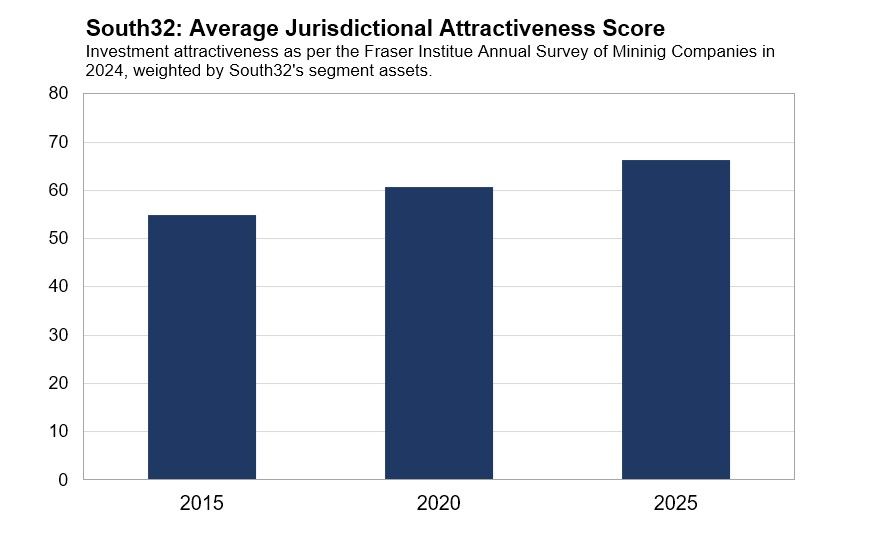

Pleasingly, these changes have been accompanied by a tangible upgrade to the location of the company's portfolio of assets. While ranking the attractiveness of a given mining jurisdiction is inherently subjective, one approach is to use the most recent Investment Attractiveness Index Scores from the Fraser Institute’s Annual Survey of Mining Companies. Weighted by assets, South32’s average score has improved significantly over the past decade, as shown in the chart below. Continued investment in attractive jurisdictions such as Alaska and Arizona should result in further improvement. Interestingly, using the same approach, South32’s score of 66 compares reasonably well with our estimates for Rio Tinto (68) and BHP (70).

The Future

The bulk of South32’s growth capital expenditure is being directed towards its Hermosa asset in Arizona, which offers multi-decade exposure to critical minerals within a single US-based district-scale asset. Hermosa hosts a number of large high-grade polymetallic deposits as well as potential exploration upside. Of these, the “Taylor” zinc-lead-silver project is currently under construction and has attractive forecasted economics (particularly at the current silver price) with an estimated initial operating life of 28 years. It is the first mining project admitted to the FAST-41 permitting process, and appears to have leveraged US policy support regardless of which party occupies the White House. The US regulatory environment appears more of a tailwind than a headwind these days, with bipartisan support for domestic production and a decoupling from Chinese supply chains. Hermosa looks set to become South32’s flagship asset.

Ambler Metals, of which South32 owns 50%, holds high-grade polymetallic deposits in Alaska. The Trump administration’s recent approval of the Ambler Access Road goes a long way to securing project viability. Ambler’s copper-zinc “Arctic” project is the most advanced with very attractive forecasted economics and a 13-year mine life, within a broader district that holds a lot of potential.

South32 acquired a 45% interest in the Sierra Gorda copper mine in 2021. The Chilean mine has been producing copper since 2014, but owing to its enormous resource base still has a 24-year expected operating life. In addition, recent exploration results suggest meaningful resource upside potential, along with an option to process surface stockpiles. The operation is investigating increasing annual output with study results expected soon.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Conclusion

South32’s unique expansion potential in critical metals is in our view particularly attractive given that it aligns the company with strong secular trends: the green energy transition, AI led productivity improvements, and the continued industrialization of the developing world. Despite its transformation and attractive future prospects, after taking its Taylor project into account, we estimate that South32 is trading on a single digit multiple of underlying earnings at current spot prices. This is before considering the upside potential from Ambler Metals, a Sierra Gorda expansion, or further commodity price upside. In a market otherwise starved of high quality, long-life, near-term growth options, it is our view that South32 is truly a misunderstood miner.

Disclaimer: This article is based on a commentary prepared by Contrarius Investment Advisory Pty Limited (“Contrarius Australia”, AFSL 506315), investment manager of the Contrarius Australia Equity Fund (the “Fund”, ARSN 664 226 331). Equity Trustees Limited (“Equity Trustees”) (ABN 46 004 031 298), AFSL 240975, is the Responsible Entity for the Fund. Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT). Information is valid as at 31 December 2025. This information is general in nature and has been prepared without taking into account your personal objectives, financial situation, or needs. Before acting on this information, you should consider its appropriateness and should read the relevant Financial Services Guide (FSG), Product Disclosure Statement (PDS) and Target Market Determination (TMD) available at www.contrarius.com.au. The article is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, neither Contrarius Australia, Equity Trustees, nor any of their related parties, directors or employees, nor InvestmentMarkets (Aust) Pty. Ltd. as publisher, provide any warranty of accuracy or reliability in relation to such information, or accept any liability to any person who relies on it. Interested parties should seek independent professional advice prior to acting on any information presented. Past performance is not a reliable indicator of future performance. Funds managed or distributed by Contrarius Australia may have a position in any of the securities referred to in this article, and such positions are subject to change at any time without notice.

Chris Watson

Director at Contrarius Investment Advisory Pty Limited.

Chris joined Contrarius Australia in January 2021. Chris was previously a director of Contrarius Investment Advisory Limited ("CIAL") in the United Kingdom from June 2017 until June 2018. He was employed by CIAL as an investment analyst from April 2012 until June 2018. Chris also previously worked for Allan Gray Ltd, South Africa’s largest privately-owned investment firm. He holds a Bachelor of Business Science (Quantitative Finance) from the University of Cape Town, and is a CFA and a CMT charterholder.