Why Shorting is a Bad Idea for Most Investors

Simon Turner

Wed 6 May 2026 7 minutesIn recent years, shorting has migrated from the realms of professional hedge fund management into reach of individual investors en masse. That’s not necessarily a good thing.

Rather than offering investors a sophisticated edge, in reality, shorting often represents an expensive wager against the long-run direction of markets wrapped up in additional layers of timing risk, borrowing risk, and behavioural risk.

What is Shorting?

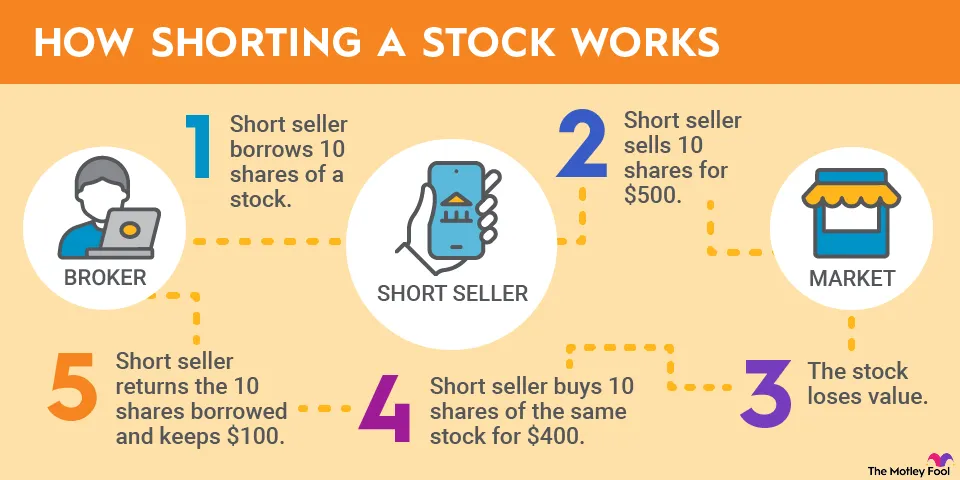

Shorting involves borrowing shares from a broker (in return for interest), selling them at the current price, and buying them back later at a lower price to return to the lender.

The intention of this strategy is to profit from the difference between the current price and the, hopefully, lower future price.

It sounds so simple. But…

The Trend is Your Friend

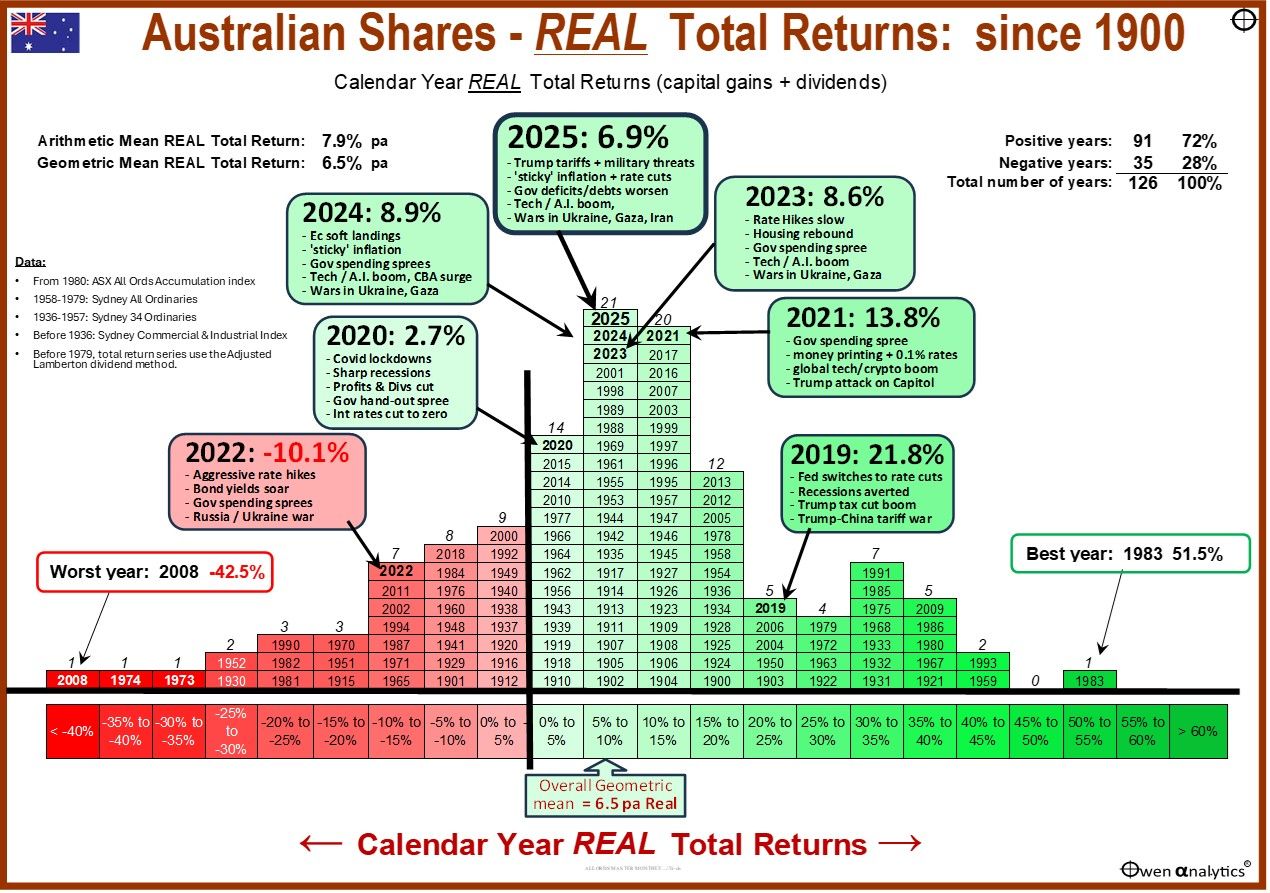

The number one reason why shorting is a bad idea for most investors is because global and domestic equities have exhibited a powerful upward bias over the long-term.

The S&P 500’s 10-year return is still above 10% p.a., while the All Ords has historically rewarded patient owners with an average real return of 8% p.a. since 1900.

In a market that tends to rise over long horizons, betting on declines is much harder than just buying productive assets and letting compounding do the work.

You’re effectively swimming against the tide.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Understanding Your Downside Risk

Beyond investing against the long-term trend, there’s an even bigger challenge to be aware of when shorting.

When you buy (go long) a stock, fund, or ETF, the worst-case loss is the capital you invest in it.

In contrast, when you go short, the upside is capped at 100%, but the downside can keep running indefinitely.

For example, if you short a stock at $5 that runs all the way to $25, you’ve generated a 400% loss.

FINRA states this plainly in its margin disclosure: ‘You can lose more funds than you deposit in the margin account, and the firm can liquidate positions without contacting you.’

Moreover, a short thesis can be fundamentally right and yet still fail because the timing is wrong, the market squeezes higher, or you’re forced out before the share price eventually falls.

The challenge is that shorting requires precision in a world that rarely offers it. A bad company can remain expensive for years. A promotional stock can rise on excitement long after valuation has ceased to matter.

Warren Buffett has long been sceptical for exactly this reason, warning that short selling ‘has ruined a lot of people’ and that it is ‘a very, very tough business because of the fact that you face unlimited losses.’

Even if one treats that as a veteran’s caution rather than a fact, it captures a truth that ordinary investors should respect: being early on a short can be indistinguishable from being wrong.

There’s a personal story to add here.

Earlier in my career, I worked for a London-based hedge fund which aimed to generate market-neutral returns by hedging its long book against a short book that reduced its net market exposure (longs minus shorts) to under 20%. For the first few years, the fund’s performance was solid, and importantly, uncorrelated with the broader market direction.

But then, one of our team members presented an extremely confident short thesis on a German silicon producer by the name of Wacker Chemie. It was decided that this was such a strong thesis that we would go all-in with a short that represented 5% of our fund assets. The analyst believed the stock price would fall by 80%+ which would generate a 4% return for the fund.

The problem was the timing of the short thesis was completely wrong and the stock more than doubled in a matter of weeks due to an expanding global silicon shortage, which was at odds with the thesis.

The fund eventually bought the stock back at almost triple the price it had short-sold it. It was a disaster for the year’s performance and had long-term ramifications in the form of fund outflows.

All of this resulted from one overconfident short position.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

It’s the Same but Different with Short ETFs

These days, shorting as a strategy is available to investors via funds and ETFs.

Whilst the risks of investing in a portfolio of shorted stocks are less extreme than shorting individual stocks, it shouldn’t be confused with a long-term allocation.

Products such as BetaShares Australian Equities Bear Hedge Fund (BEAR) seek returns negatively correlated to the Australian share market ‘on a given day’. That wording is the point. These are daily tactical instruments rather than core holdings.

The performance record shows why. As at 31st March 2026, BEAR’s since-inception return has been -7.9% p.a.

Of course, this is intentional. This product is designed for short bursts of protection as opposed to wealth creation across a normal investment cycle.

And just like shorting individual stocks, even if you are directionally correct about a market decline, a jagged path can still damage your return by forcing you to exit your position at the wrong moment.

This is why inverse and geared products so often disappoint investors who hold them too long. The problem isn’t just being wrong on direction. It is also being wrong on path, volatility, and time horizon.

A Defined Role to Play for Informed Investors

None of this means there is no place for shorting in markets. There is for investors who understand the high and unique risks of the strategy.

In some situations, it can help with price discovery, and can be useful in specialist strategies.

The VanEck Australian Long Short Complex ETF (ALFA), for example, is an actively managed, systematic long-short strategy designed to outperform the S&P/ASX 200 over the medium to long term after fees and costs.

That’s a very different proposition from a retail investor deciding to short a stock or sit in a bear ETF for months. In effect, it outsources the complexity to a process built for it. Even then, it remains a specialist satellite idea rather than an obvious core holding for most portfolios.

Short Strategies Make Investors Feel Cleverer Than Patient

Shorting is a bad idea for most investors because it tempts them to feel clever when they should be patient. It rewards contrarian theatre more than disciplined wealth building. And it distracts from the simple truth that decades of market evidence keep reinforcing: owning diversified productive assets is easier, more robust, and more repeatable than trying to monetise market declines.

So, bear ETFs should be regarded as trading tools rather than long-term investments. To build sustainable resilience, the better answer is a diversified portfolio built from diversified ETFs and funds. These products allow investors to compound their returns with breadth and cost efficiency, and without the constant maintenance and emotional stress that shorting requires.

Funds Mentioned

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.