-zdalarekmzl2x534cuyn.png)

Want an Extra 1.5% p.a. in Returns? Why Investor Psychology Destroys More Wealth Than Fees

These days, most investors are well-trained to minimise their fund and ETF costs. It’s been drilled into their minds that an apparently small fund fee difference can create an enormous performance drag over the long term. Hence, management expense ratios, brokerage fees, and tax leakage dominate product comparisons and marketing narratives.

If only more investors had a mirror handy. Because, in reality, the most persistent and destructive cost most investors bear is almost always behavioural. Investors’ timing decisions, driven by emotion rather than discipline, have a far greater impact on long-term outcomes than fees ever could.

Mind the Gap

The data doesn’t lie.

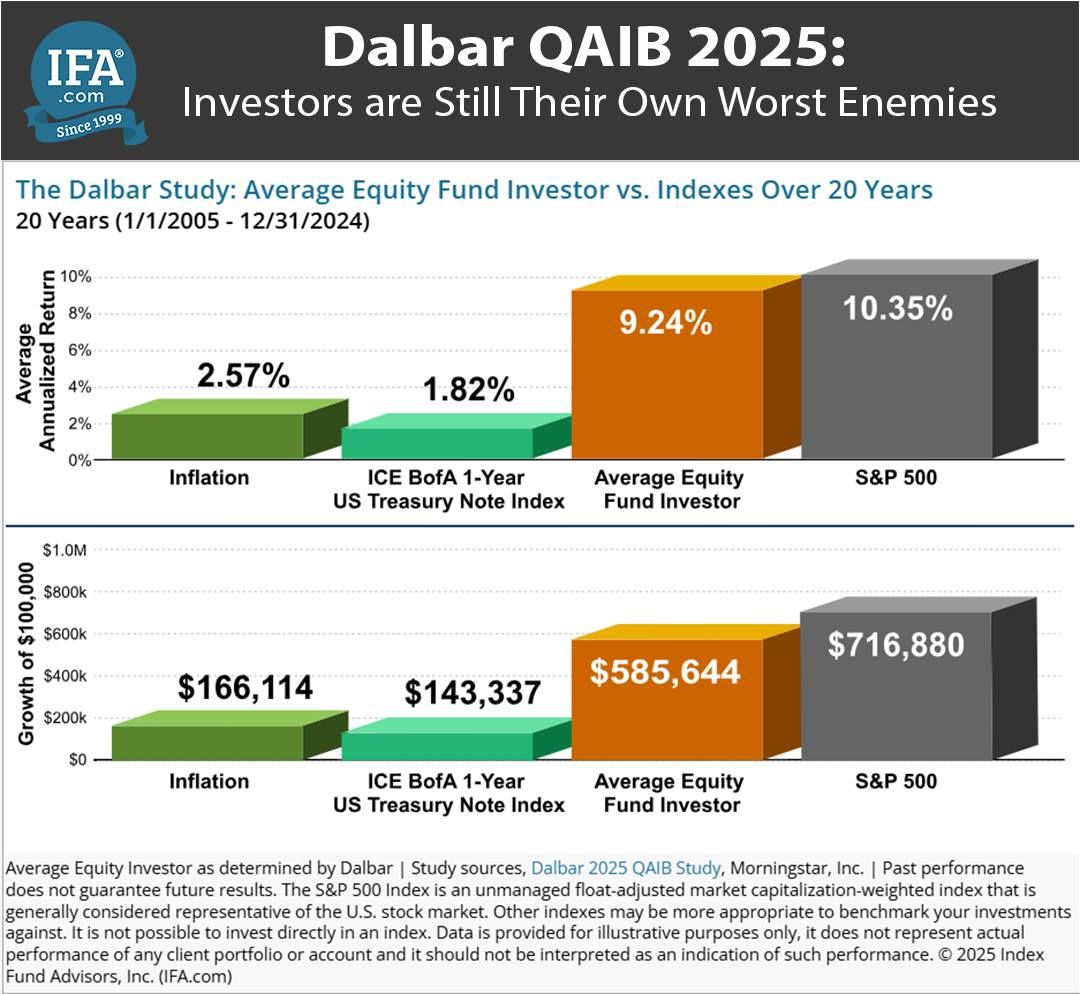

DALBAR’s annual Quantitative Analysis of Investor Behavior consistently finds that the average equity fund investor underperforms the funds they invest in. In the 2025 report, it showed that US equity investors underperformed the S&P 500 index by over 1% p.a. over the past twenty years due to mistimed entries and exits.

1% p.a. may not sound like a lot. But thanks to the power of compounding, it translates into a more than $130k difference in end portfolio value over twenty years. That’s a significant difference considering the portfolio’s starting value was $100k.

While DALBAR’s data is US-centric, similar behavioural gaps have been observed in Australia.

Vanguard’s long-running research into investor outcomes, highlights that behavioural coaching alone can add up to 1.5% p.a. to investors’ net returns by preventing common mistakes such as performance chasing and panic selling. By helping investors stay calm during bouts of volatility, these gains come from avoiding emotion-driven mistakes.

While we’re on the subject, the research highlights there’s a wider range of performance-enhancing gains on offer for investors who are willing to control their emotions while following a prudent investment plan:

Source: Vanguard

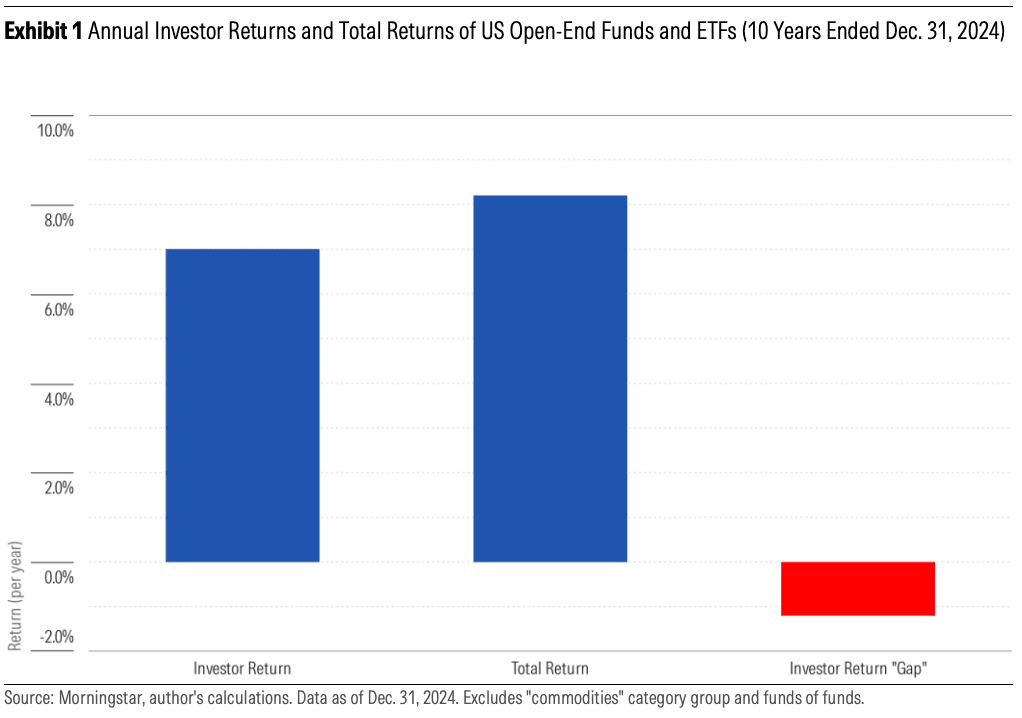

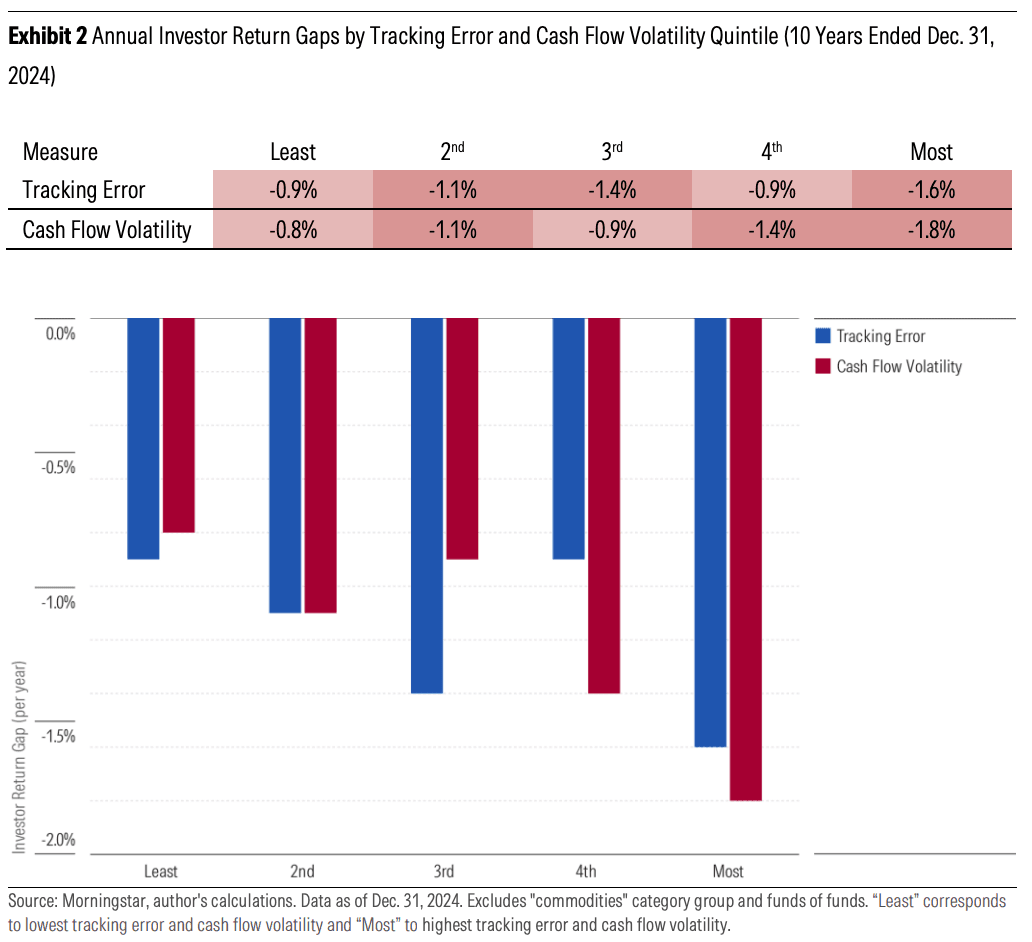

Morningstar’s 2025 Mind the Gap study concurred. It identified a 1.2% p.a. ‘investor return gap’ over the ten years to December 31st, 2024, with larger gaps in more volatile asset classes.

Importantly, the Morningstar study revealed that the gap widens in periods of market stress, when emotional decision-making becomes more pronounced.

These findings challenge a myopic focus on fees at the expense of investors mastering their own behaviour.

While reducing fees is undeniably beneficial for long-term returns, the marginal gains from selecting a fund with a 0.2% p.a. fee over one charging 0.6% p.a. pale in comparison to the gains won by avoiding poor timing decisions.

Of course, for many investors changing their behaviour is easier said than done. Many are at the mercy of their emotional biases, whether they like it or not.

In particular, investors tend to trade excessively which causes them to underperform.

To that point, Barber and Odean’s study, ‘Trading Is Hazardous to Your Wealth’, found that the most active traders significantly lagged the market, primarily due to overconfidence and a tendency to react to short-term noise.

Recent CFA Institute research highlights loss aversion, recency bias, and herd behaviour as the dominant drivers of investors’ poor investment outcomes.

The upshot is that many investors are prone to selling after declines to avoid further losses, only to miss the subsequent recoveries. Then they re-enter markets after periods of strong performance. As a result, they keep buying high and selling low despite their better intentions.

Source: Pepperstone

The Australian market provides plenty of examples of investors destroying value en masse.

During the COVID-19 market shock in March 2020, for example, ASIC research showed a sharp spike in retail trading volumes, with many investors exiting positions near the bottom. A significant proportion of investors then re-entered the market during the recovery phase later that year, after prices had already rebounded.

This is the behavioural cost of unmastered emotional biases.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Important Implications

The implications are profound:

- It’s easy to undo a solid investment plan in seconds.

The benefits of diversification, income generation, and professional management can be materially undermined if investors intervene at the wrong moments. Exiting during drawdowns, rather than maintaining a long-term perspective, effectively converts a temporary mark-to-market loss into a permanent capital impairment.

- Emotional investors are vulnerable to missing the market’s best days.

The majority of market returns are generated during a relatively small number of trading days, often clustered around periods of heightened volatility. As shown below, missing just the ten best days can more than halve a portfolio’s value over a quarter of a century.

Hence, staying invested is a prerequisite for investment success.

- Self-awareness is an uncommon advantage and possibly the main edge available to individual investors.

The persistence of behavioural underperformance raises a critical question: why do investors continue to make the same mistakes despite the overwhelming evidence of the issue?

Part of the answer lies in the structural design of the investment industry.

Performance reporting is typically backward-looking and short-term, reinforcing recency bias. Media coverage amplifies market noise, while digital platforms make trading frictionless, encouraging activity rather than discipline.

There’s also a deeper cognitive dimension. Behavioural biases are rooted in evolutionary instincts that prioritise survival over rational optimisation. In other words, they are hard-wired into us, and thus challenging to become aware of and take control of.

Loss aversion, for instance, reflects a fundamental human tendency to weigh losses more heavily than gains. In financial markets, this leads to risk-averse behaviour at precisely the wrong time.

- Take proactive action to prioritise managing your emotions.

Addressing your emotional biases requires a shift in how you think about costs. Fees are explicit and controllable, but behavioural costs are implicit and require deliberate mitigation.

For example, consider automating your monthly investing to reduce your scope for emotional decision-making.

- Use managed funds and ETFs to your psychological advantage.

Outsourcing to professional managers is a powerful means of mitigating against the risks posed by your emotional biases.

The growing availability of diversified, professionally managed funds and ETFs provides the building blocks for strategies which enable unemotional investor behaviour aligned with their investment plans.

- Reframe risk.

Reframing the concept of risk is also part of mastering your emotional biases.

In particular, it’s important to understand that volatility is not the primary threat to long-term wealth. Behaviour is. Investors who internalise this distinction and structure their portfolios accordingly can materially improve their outcomes.

Time to Look in the Mirror

The evidence is unambiguous. Behavioural mistakes represent the largest and most persistent drag on investors’ returns. Reducing fees remains important, although investors who focus exclusively on costs while neglecting their own behaviour risk prioritising solving the wrong problem.

In short, the greatest edge an investor can achieve is behavioural. Those who can remain invested through volatile market conditions, resist the urge to chase performance, and adhere to a disciplined plan are far more likely to optimise their long-term returns.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

Related Articles

-l7rg6lkopgoa2x6pxhua.png)

-4jjuh9ocumc2do1vonr2.png)

Categories

Recent Articles

View all articles-v8lxc7275hr89z0hzkrz.png)

-ulhzagvbsmdk2tc72zgj.png)

-weh3swd4zyleexypgsv3.png)