Navigating Fixed Income Markets During a Chaotic Year

Simon Turner

Wed 22 Apr 2026 7 minutesFor bond investors, the first few months of 2026 have been chaotic to say the least. It has been a year in which duration, inflation sensitivity, and market structure have mattered again, often brutally.

The global backdrop is unusual. Sovereign and corporate borrowers are still coming to market in enormous size, policy rates are no longer moving in lockstep across major economies, and the recent oil price shock has forced headline inflation back into the fixed income conversation just as many investors had begun to relax about it.

Should we expect more of the same for the rest of the year? Or will 2026 continue to challenge fixed income investors in new and surprising ways?

An Abundance of Supply

Like all markets, bond market pricing is determined by demand and supply.

Importantly, global bond supply is historically high right now.

The OECD expects governments and corporations to borrow US$29 trillion from markets in 2026, with net sovereign borrowing projected to climb to nearly US$4 trillion, the second-highest level on record.

That scale matters because bond markets are not absorbing new paper in the benign conditions of 2015 or 2019, but in a world of higher real rates and more price-sensitive buyers.

Investors Demanding Fair Compensation

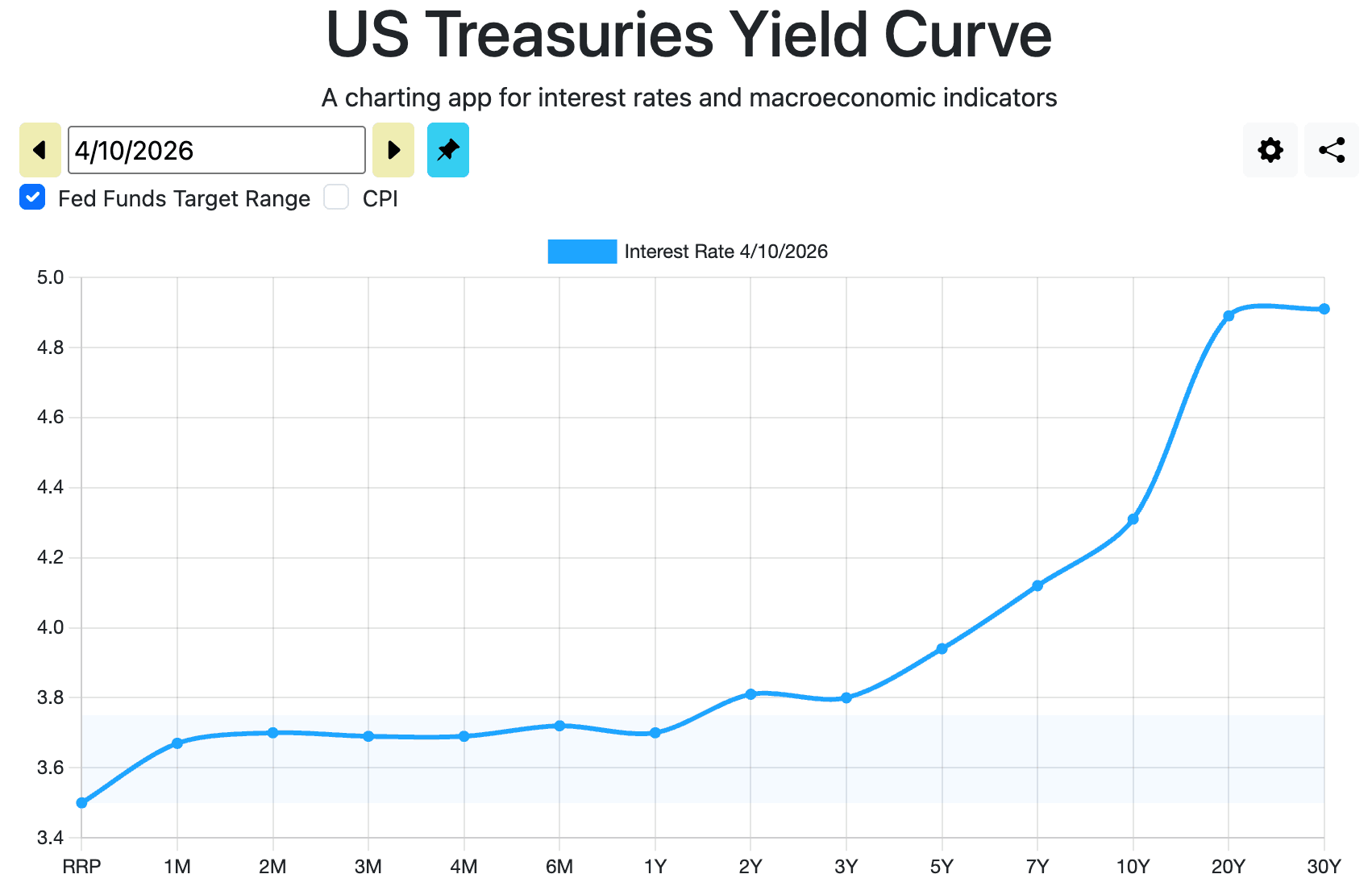

The US still sets the emotional tone for global duration, and the signal from US Treasuries has been clear.

Having been inverted (short-term rates higher than long-term rates) for much of the past couple of years, the yield curve is now upward-sloping and steeper than investors have been used to for some time.

As shown below, the 3-year Treasury yield is 3.8% versus 4.9% for the 20-year equivalent.

At the same time, the recent US Treasury auction evidence has been less than reassuring: the US Treasury’s 8th April sale of US$39 billion in 10-year notes cleared at 4.28%, supported by only middling demand.

That’s a strong signal that investors are again demanding compensation for duration and supply risk, especially at the long end.

Central Bankers as Focused on Inflation as Ever

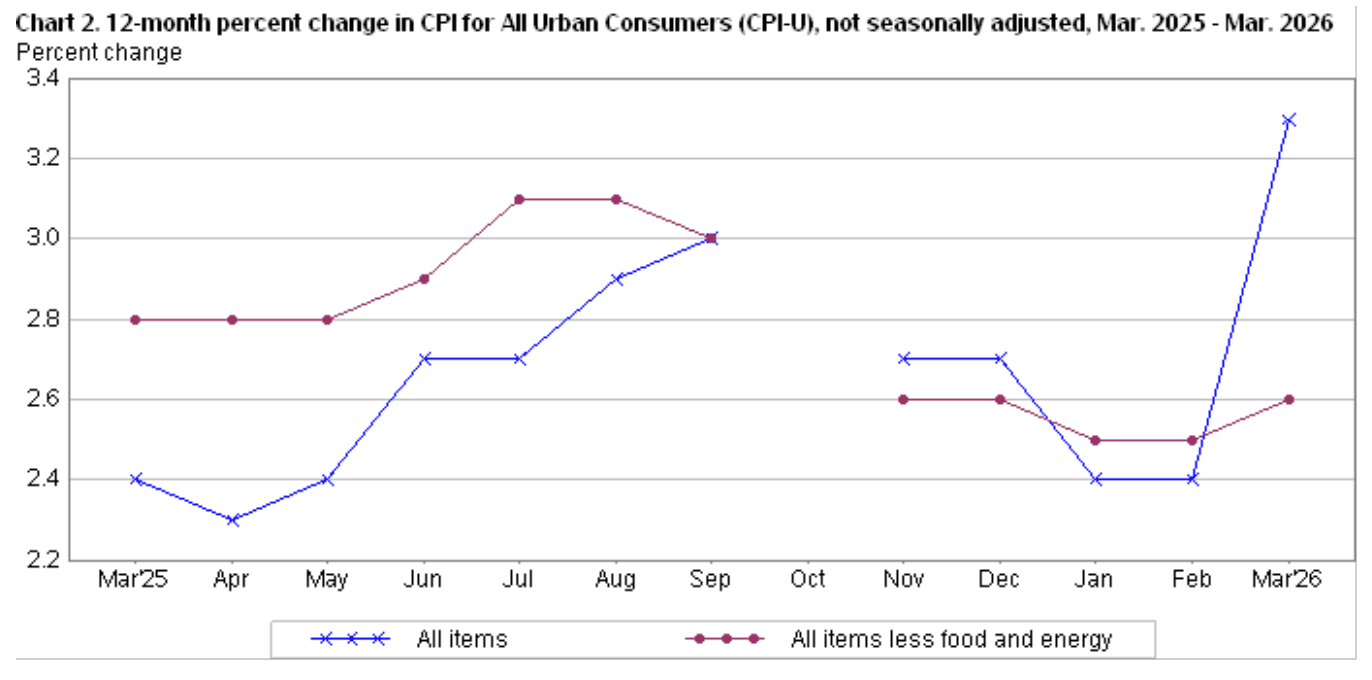

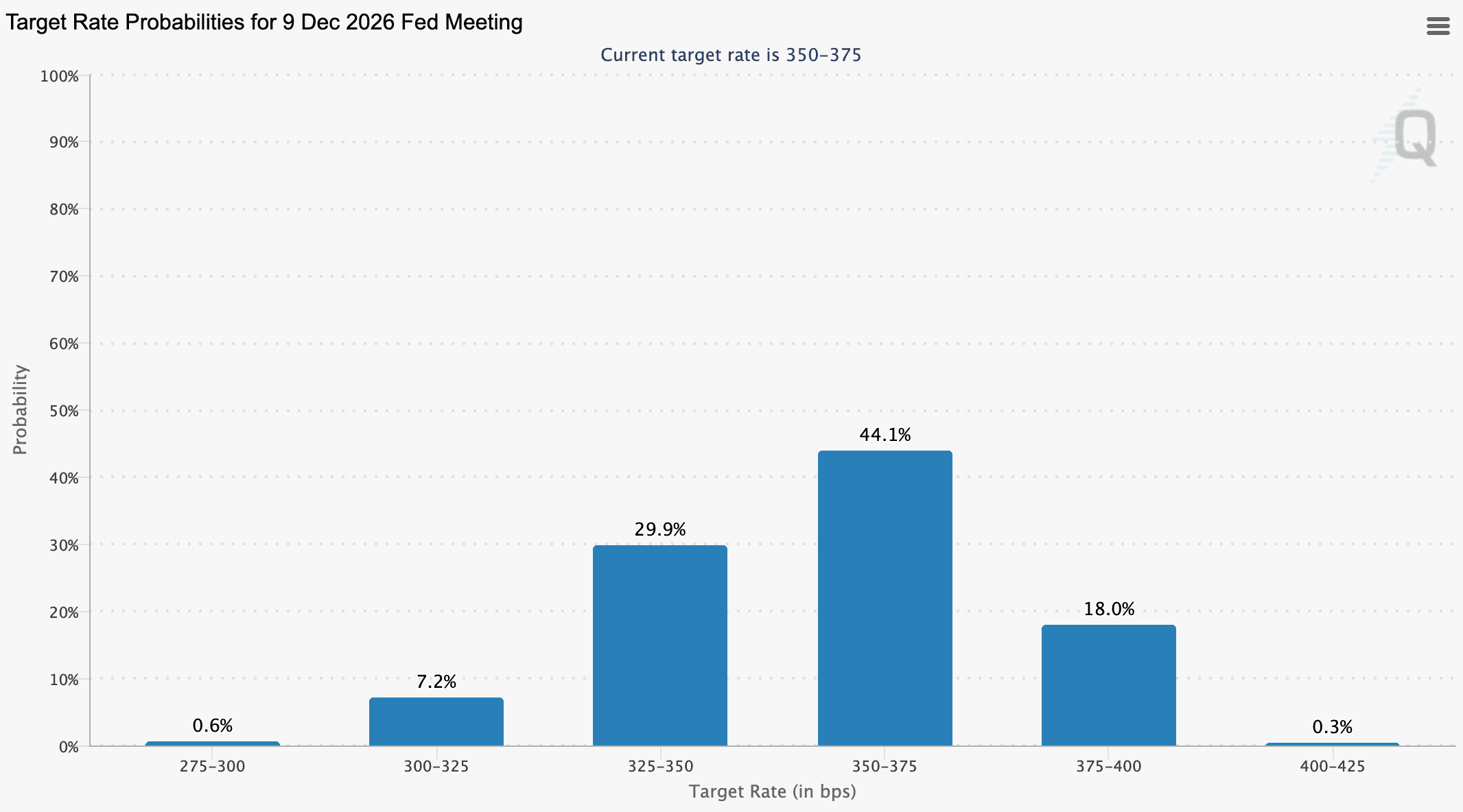

Then there’s the recent inflation flare-up, which has re-entered the bond market’s equation in a more specific way than the usual hand-waving about geopolitics.

To that point, the US Bureau of Labor Statistics reported that the CPI rose 0.9% in March and 3.3% over the year, while core CPI rose 0.2% in the month.

This matters for fixed income markets because it has made the Fed’s job less straightforward, particularly with the recent oil price surge. Whereas the Fed was previously widely expected to cut rates multiple times before the end of the year, markets are now pricing in a 44% chance that rates remain stable.

In other words, the market has shifted from debating how fast Fed policy is likely to be eased to how long nominal yields must stay restrictive even if growth softens.

That’s a dramatic shift with broadly bearish implications for global bond (and equity) investors.

Europe is in a different, albeit equally challenging situation.

The ECB’s March 2026 projections put euro area headline inflation at 2.6% in 2026, before easing to 2.0% in 2027, while the deposit facility rate has remained at 2.0%.

That leaves Europe with lower nominal yields than the US, but not necessarily a cleaner fixed income story, because inflation has not vanished and growth remains vulnerable to the same energy and confidence shocks hitting the rest of the world.

For global bond investors, that regional divergence is important.

It means there’s no longer a single, easy macro trade for developed market bond investors.

It also means the case for active duration and currency management is now stronger than it was when most major central banks were moving in broad synchrony.

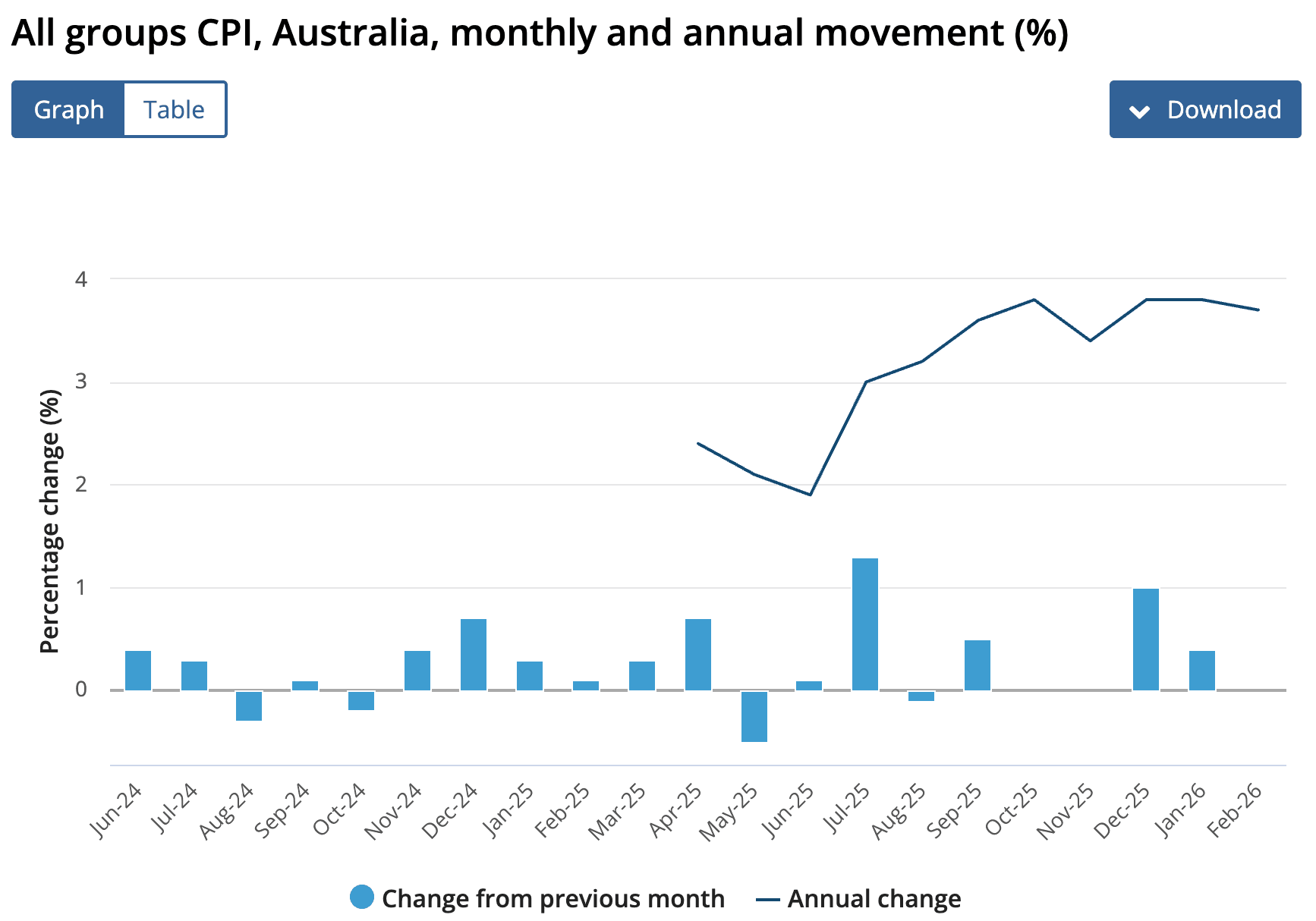

Australia’s bond market is living through its own version of the same problem, with a more acute domestic inflation wrinkle.

The ABS reported that consumer prices rose 3.7% in the year to February 2026, with trimmed mean inflation at 3.3%.

The stickier detail is housing-related inflation. It rose 7.2% over the year, and electricity prices were up 37.0% as rebates rolled off.

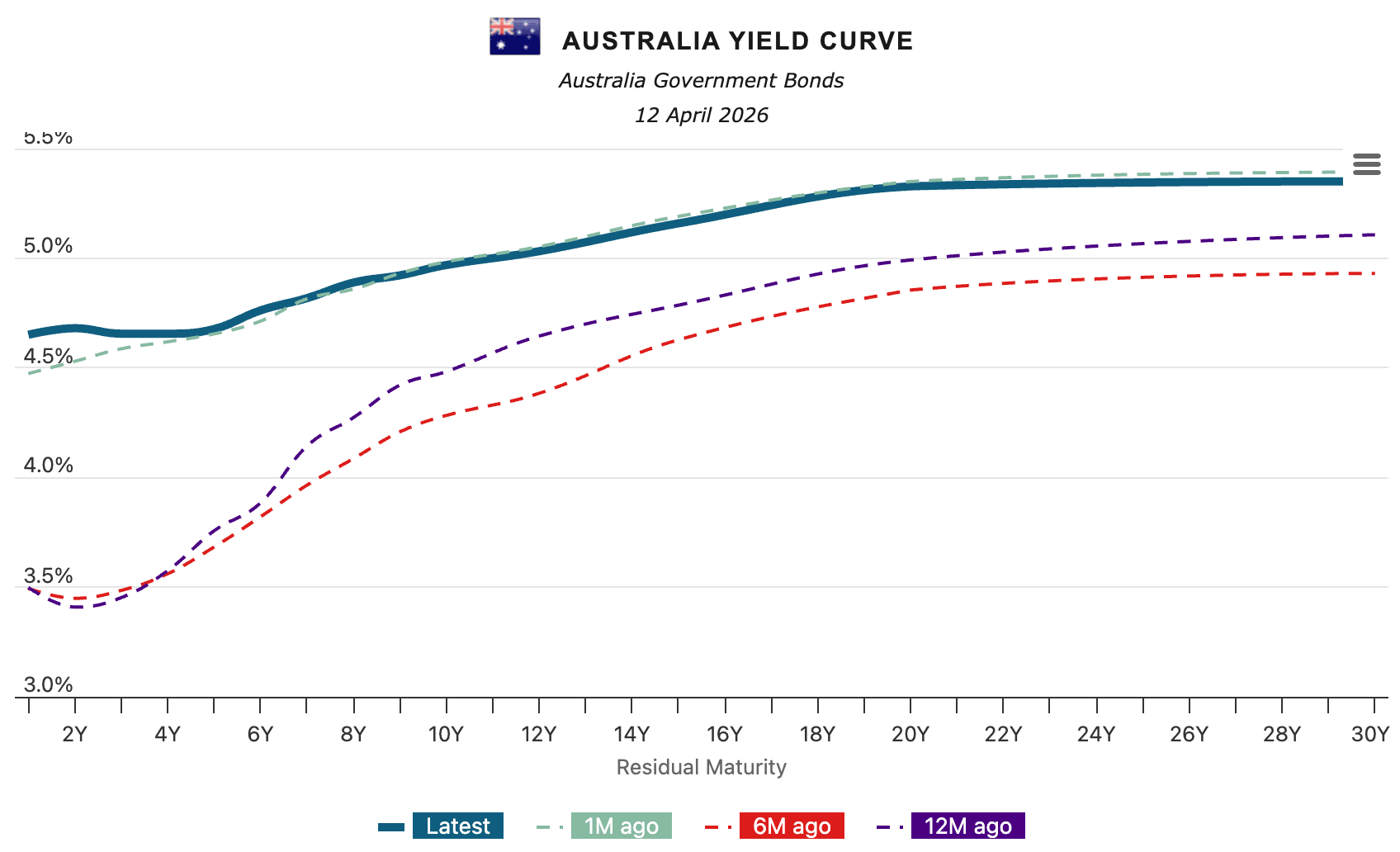

This is the main reason why Australian front-end yields remain elevated in a global context. The Australian Government 2-year bond yield is at 4.7% versus 5.0% for the 10-year, as shown below.

Rather than indicating a strong underlying economy, the local yield curve is a demonstration of how stubborn domestic inflation is proving to be.

Supply is also part of that domestic picture.

The Australian Office of Financial Management initially said Treasury Bond issuance for 2025-26 was expected to be A$150 billion, then revised its forecast down to A$125 billion.

That reinforces the broader point that fixed income markets are being asked to digest a lot of paper at yields that are high enough to attract buyers, though not always high enough to make them indiscriminate.

The upshot is that investors who think of government bonds as a ballast may be missing how much macro and fiscal arithmetic now shapes term premia.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Fixed Income Markets Remain Solid at Face Value

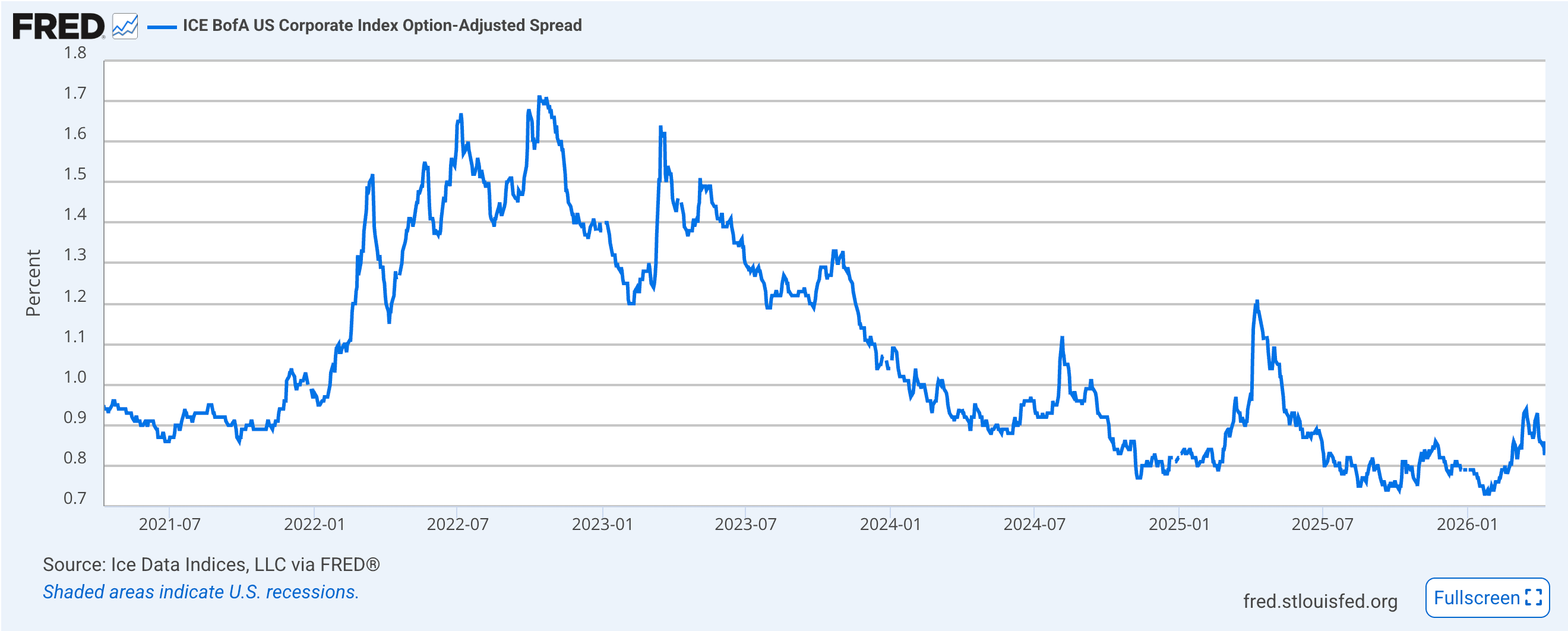

What’s most striking amidst so much noise is that credit markets have not yet cracked.

The RBA noted in its February Statement on Monetary Policy that corporate bond spreads in Australia and other advanced economies are little changed at very low levels.

In the US, the ICE BofA US Corporate Index option-adjusted spread and the BBB spread are both still sitting near historically tight territory.

That tells investors two things.

First, all-in yields in credit remain attractive largely because government bond yields are high, not because spreads are offering enormous protection.

Second, the margin for error is arguably thinner than headline running yields might suggest. If economic growth weakens materially or refinancing stress reappears, spread income could prove less generous than today’s carry implies.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

How to Outperform in Fixed Income

The key takeaway is that the next phase of global fixed income performance is less likely to be won by broad, undifferentiated bond exposure, and more likely by being precise about the true nature of bond risks investors are exposed to in this strange new world.

With policy uncertainty still high and inflation shocks no longer hypothetical, extending duration aggressively just because yields look better than they did in 2021 is probably not a prudent response.

The more compelling opportunity is to separate carry from conviction.

High-quality short and intermediate duration exposures now offer real income again, while selective additions to longer duration make more sense when they are tied to a view on slowing growth or disinflation rather than to nostalgia for the old bond bull market.

Credit Still has a Role to Play

Credit still has an important portfolio role to play, but investors should recognise that much of today’s appeal comes from higher base yields, rather than expected duration-driven outperformance.

This is a year when fixed income funds and ETFs are more likely to drive portfolio outcomes for the investors who understand exactly which risks they are being paid to take, and which they are accepting for free.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.