Winning the Investment Game: 6 Powerful Rules That Remove Emotion from the Process

Simon Turner

Sun 7 Jun 2026 7 minutesIf you’re like most investors, you’re probably overwhelmed by the constant availability of real-time data, macro narratives, and algorithmically amplified sentiment. It’s a lot, and it’s coming at us twenty-four hours a day, seven days a week. Worse, our emotions drive us to react to all this noise by sabotaging our investment plans at exactly the wrong moments.

The consequences are hard to understate. It’s no surprise that, on average, individual investors keep underperforming the market and the funds they invest in.

Understanding these challenges is valuable for investors. Knowing how to bypass them with a simple operating system is much more valuable.

Weighed Down by Emotions and Information

The cost of investors being overwhelmed by their emotions combined with information overload can be quantified in terms of performance.

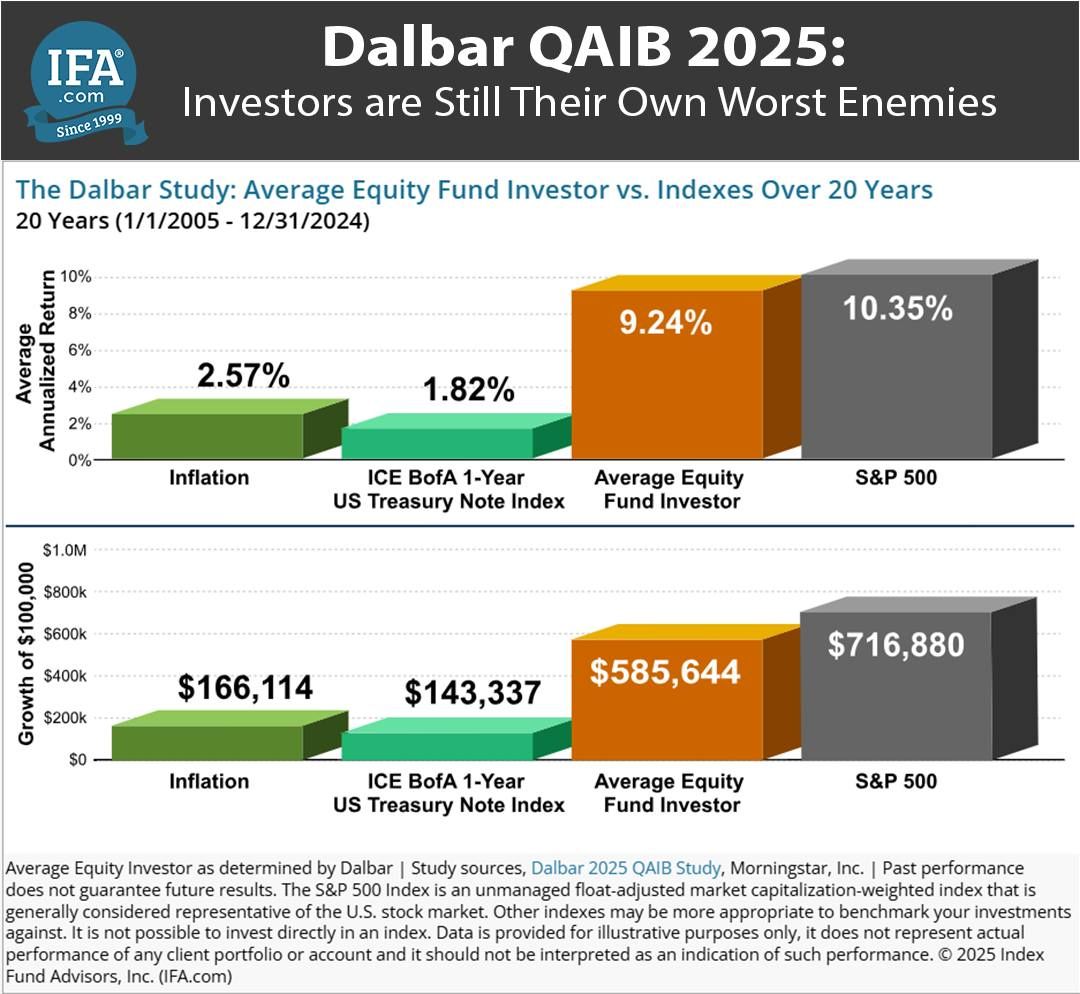

DALBAR’s long-running Quantitative Analysis of Investor Behaviour shows that US equity fund investors have underperformed the S&P 500 by over 1% p.a. over the long term due to poor timing decisions.

Morningstar’s ‘Mind the Gap’ study reached a similar conclusion, estimating a behavioural penalty of roughly 1.6% p.a. for the average investor.

Clearly individual investors are not benefitting from the advantages offered by the expanding universe of ETFs and managed funds.

The problem is that individual investors are not always aware of their emotional biases and the detrimental impact they are having on their portfolios.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

The Operating System that Addresses the Challenge

So, what’s an investor to do?

The answer is to have an operating system that pre-empts and addresses these challenges.

Here are six simple operating system principles that empower investors to rise above the noise:

1. Create a proactive asset allocation plan aligned with your goals.

The first principle is that allocation decisions should be pre-committed in a well-thought-out investment plan rather than reactive.

This is particularly important since asset allocation is the main determinant of portfolio returns.

To that point, Vanguard’s ‘The Global Case for Strategic Asset Allocation’ found that more than 90% of portfolio return variability is explained by asset allocation rather than security selection or market timing.

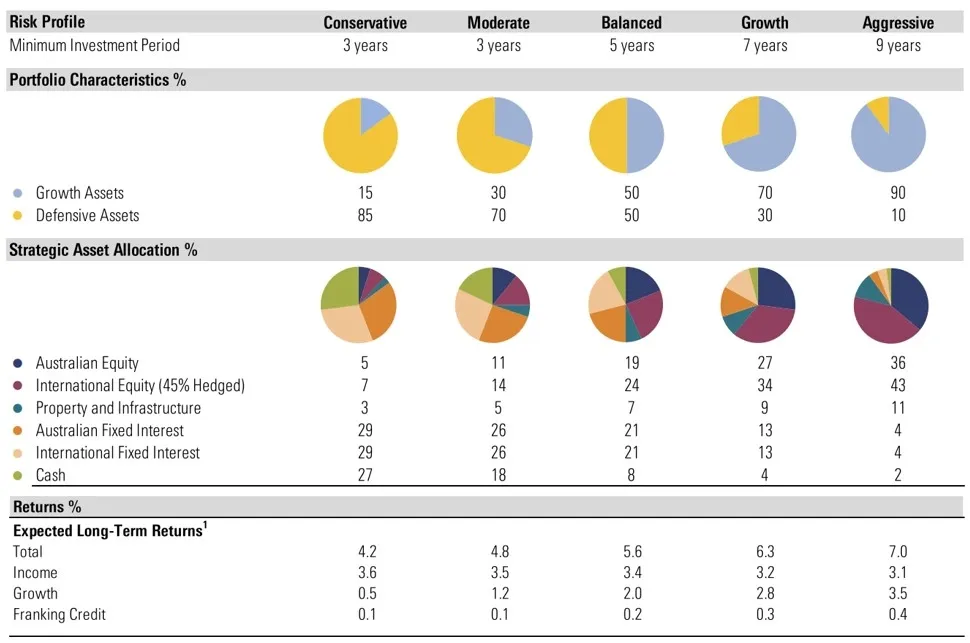

Here are Morningstar’s asset allocation guidelines for various types of investors:

You’ll notice that aggressive investors are guided to be primarily exposed to growth assets such as Australian and international equities, whereas conservative investors are mainly directed towards Australian and international fixed interest and cash.

The important thing is to match your asset plan with your personal goals, risk profile, and time horizon.

You’ll also want to commit to your plan regardless of what happens in markets.

Case in point: during the volatility of 2022, when global equities fell sharply and bond markets delivered their worst drawdown in decades, investors who maintained diversified allocations recovered meaningfully in 2023 as both equities and fixed income rebounded. Investors who deviated from their plans and sold their risk assets late in 2022 missed that recovery. That move would have been catastrophic to their subsequent returns.

The key takeaway is that your target allocation should be defined in advance and adhered to regardless of what’s happening in markets.

Your plan should also leverage the benefits of diversification.

Whilst the correlations between asset classes increases during times of market stress, diversified portfolios generally experience lower drawdowns and are thus more resilient.

The other great benefit is that diversified investors tend to be less reactive during market sell-offs in the knowledge that their portfolio was created to navigate events like this.

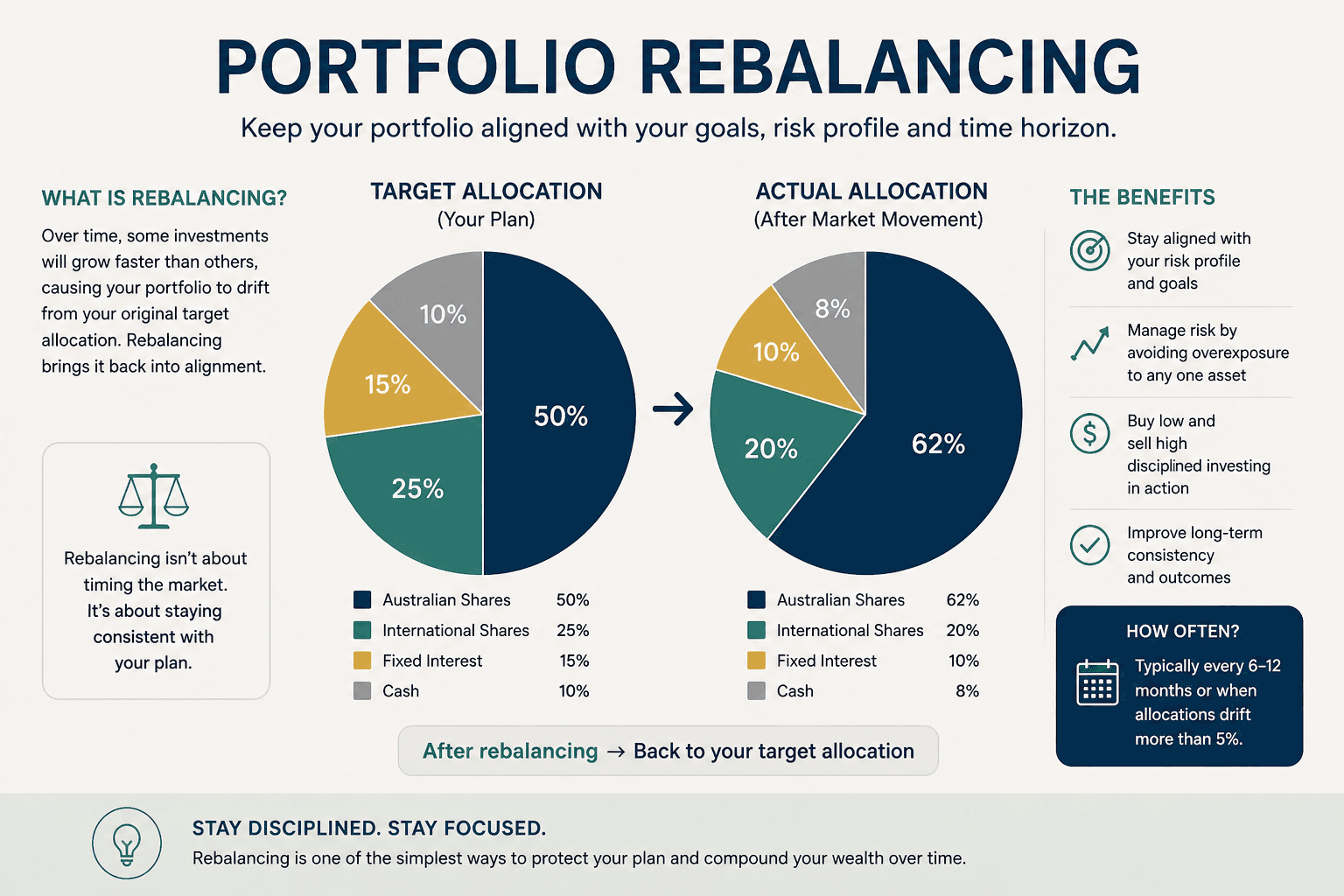

2. Systematically rebalance.

The second principle is that portfolio rebalancing should be regular and systematic.

At its core, rebalancing is the act of restoring a portfolio to its intended shape. But its deeper function is behavioural.

In short, a rebalanced portfolio systematically sells what has outperformed and buys what has lagged.

Disciplined rebalancing captures mean reversion across asset classes over time.

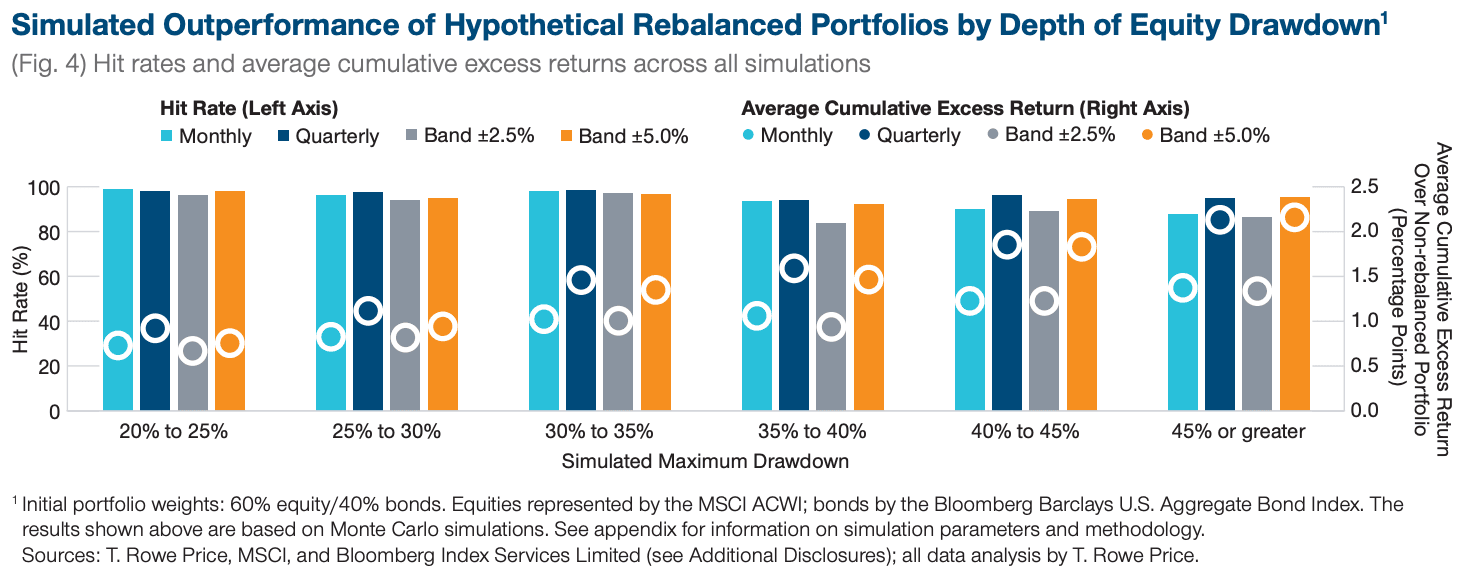

That translates into improved performance. T. Rowe Price research shows that rebalancing resulted in an average 1% p.a. additional performance over ten years.

There are two main rebalancing approaches to be aware of: time-based rules, such as annual rebalancing, or tolerance bands, such as rebalancing when an asset class deviates by more than 5% from its target weight.

For most investors, an annual rebalance is the optimal and simplest approach.

3. Volatility integrated as part of the journey.

The third principle is that volatility should be viewed as a normal part of investing rather than a signal to sell.

This is so important. There’s extensive research showing that retail investors react to short-term market moves by selling, often locking in losses.

So, an effective operating system requires predefined holding periods and clear expectations about the role of each allocation, including during market selloffs.

4. Focus on costs.

The fourth principle is cost discipline, which remains one of the few variables that investors can control with certainty.

This is a big deal because fees can erode retirement balances by tens of thousands of dollars over a working lifetime.

The rule is not to avoid fund and ETF fees entirely, but to ensure that each allocation justifies its cost through a clear portfolio function. This shifts the decision from an emotional reaction towards a rational assessment of value.

5. Tax efficiency integrated into the plan.

Tax awareness is also important since capital gains tax and franking credits have a major impact on after-tax outcomes.

Capital gains realisations tend to spike during periods of market stress, suggesting that investors often crystallise losses or gains at suboptimal times.

A rules-based approach to holding periods and rebalancing can reduce unnecessary tax events, improving net returns over time.

6. Automate monthly investing.

There’s one final principle that allows investors to bypass the problems their emotions pose: automating their investing each month.

Automated investing on a monthly basis is arguably the most accessible edge available to most investors for the simple reason most investors fail at being consistent.

A well-constructed portfolio that receives irregular contributions is like a high-performance engine that rarely gets fuel.

In contrast, an unexciting, diversified portfolio that’s topped up automatically generally outperforms over the long term.

Hence, automating your investing before you spend is a game-changing habit for investors focused on wealth accumulation. Even small, regular contributions make a significant difference over the long term.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Simple Repeatable Rules = the Way Forward

These six rules are the practical application of decades of behavioural finance research distilled into a simple system.

The reason it’s so effective is because portfolio performance is largely determined by process and mindset rather than products.

Hence, investors who build and adhere to this evidence-based operating system are more likely to capture the returns that markets offer. That’s the closest thing to a structural edge available to most investors. In contrast, those who rely on discretion and emotion are likely to continue paying the behavioural penalty.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.