Franking Credits Explained

Sara Allen

Thu 4 Jun 2026 5 minutesIf you want the possibility of a bonus tax refund, or a discount on your tax, then don’t forget to check your franking credits. If that concept sounds vaguely familiar, it should be – it’s an integral part of being an Australian income investor, particularly if you are a retiree.

More than 50% of Australia’s 200 largest companies pay either partially or fully franked dividends to investors. It’s a policy designed to prevent double taxation, but can also help boost your income stream at tax return time.

The concept of franking is not unique to Australia – but we are the only country where you can use that franking for a potential refund of tax.

Though franking is a popular concept, it’s often misunderstood. At a time when inflation is rampant and every dollar counts, now is a great time to think more closely about franking credits and what this means in your portfolio, whether you are income focused or not.

What are franking credits?

The simplest way to think of a franking credit is a credit attached to your dividends representing tax that was already paid on that dividend by the company. You can use it to potentially claim a discount on your own tax return or even claim a refund on that tax paid if you are a zero-tax investor, such as a retiree.

To explain that in more detail, it only applies to Australian listed companies and is based on the Australian tax they have paid on their earnings before paying out those earnings in the form of dividends to investors.

Not all Australian companies do this and franking credits can be partial or full based on where tax is paid. For example, companies like Macquarie Group have international income streams as well as Australian operations so pay tax in other economies than Australia.

This means that they pay a partial franked dividend rather than a full one – in the case of Macquarie Group, this was partial franking of 35% for its latest earnings. By contrast, a company like Commonwealth Bank generates its income in Australia so pays tax domestically and in turn offers fully franked dividends (100% franking credit).

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

How do franking credits work?

You can apply franking credits from dividends in your tax return.

For those who pay tax, this may mean a discount on your tax based on the difference between your marginal tax rate and the proportion of corporate tax paid (noting the full corporate tax rate is 30%).

For zero-tax investors like retirees, this instead means a refund of the tax paid on your behalf.

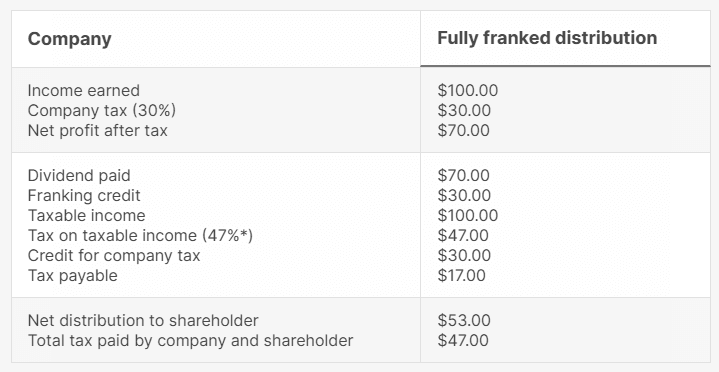

How this might look in practice for a tax-paying investor with a marginal tax rate of 47% follows – this is taken from the ATO:

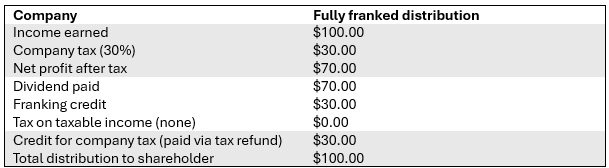

By contrast, a zero-tax investor would look different and would involve a refund. You can see in the example below, also edited from the ATO but using the same numbers as the previous article for consistency:

Can I still get franking credits outside of direct shares?

Franking credits apply to investments made in trusts, managed funds, ETFs and SMSFs if the underlying investments are direct Australian shares that offer franked dividends.

Each individual member’s allocation will be based on their proportion of the holding, and they will receive an annual statement outlining their entitlement.

In the past, trusts have sometimes created companies to distribute franked dividends to, which would have allowed them to take advantage of the flat corporate rate instead of an individual member’s marginal tax rate.

The recent Budget announcement proposed new rules whereby franking credits would no longer apply to corporate beneficiaries (so no tax refunds available if the credits were distributed to a company instead of an individual).

It’s also worth noting that a minimum 30% tax was placed on discretionary trusts from 1 July 2028 in the Budget announcement and this would require trustees to use franking credits to first satisfy the minimum tax liability before passing on credits to members. The credits the members of a discretionary trust then receive cannot be used for a tax refund. They can still be used for a discount for members with a higher marginal tax rate compared to the corporate tax rate.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Using franking in your investment portfolio

With many Australian companies offering some level of franked dividends, chances are, you already have exposure and the opportunity to make use of franking credits in your next tax return.

You can also find a range of managed funds that specifically target the use of franked dividends, so you don’t need to do the work researching. Some examples include Betashares Australian Dividend Harvester Active ETF (ASX: HVST), Plato Australian Shares Income Fund and Pentalpha Income for Life.

Using franking credits can be a critical component of an income strategy, and it can be valuable to speak to an expert to ensure you maximise this opportunity in your portfolio.

Whether you are a zero-tax investor or still paying tax, don’t forget to keep across the rules for applying franking credits using the Australian Taxation Office to avoid unexpected tax consequences.

Funds Mentioned

Disclaimer: This article is prepared by Sara Allen. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.