-zdalarekmzl2x534cuyn.png)

Collins Foods: Why Value is on the Menu

While Collins Foods (“Collins”) may not be a household name, step inside a KFC restaurant somewhere in Australia and you have a one-in-three chance of being in a Collins-run establishment. The company opened its first Australian KFC location in 1969. After four decades of expansions, diversifications, restructurings, and a stint under private equity ownership, Collins listed on the ASX in mid-2011. Since listing, its Australian KFC business has grown substantially.

Sources: Collins Foods, Contrarius Research

KFC Australia

Collins doesn’t own the KFC brand. That privilege belongs to NYSE-listed Yum! Brands (“Yum”), a company about 60x larger. Collins is a KFC franchisee. So, while Yum controls the KFC brand, menu, marketing, and sets the operating standards, Collins is entirely focused on restaurant operations. It identifies suitable sites, develops and fits-out the physical restaurants, hires and trains staff, and operates the restaurants—from managing suppliers to frying chicken, from serving customers to cleaning the floors. Yum receives royalties, while Collins retains the restaurant operating profits. For a franchisee like Collins, the name of the game is “operational excellence”.

How has Collins performed over the past 15 years? In short, it has been operationally excellent. Consider the following three metrics: growth, profitability, and return on investment.

Growth: As seen above, Collins has increased its Australian KFC restaurant numbers from 119 to 290, an increase of over 6% per annum. In addition, the average sales per restaurant rose by nearly 4% per annum. Revenue has thus lifted by 10% per annum since listing, climbing from $300 million to $1,150 million.

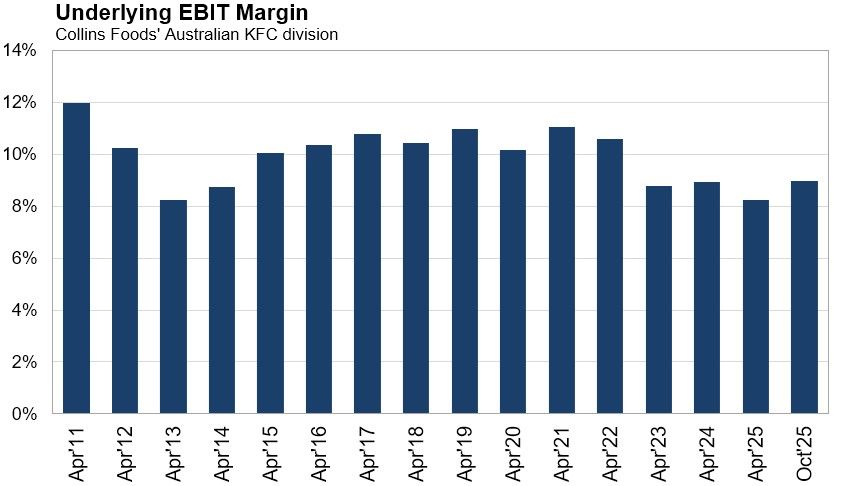

Profitability: Despite having a lot more locations, volatile food prices, rising wages, and the entrance of new competitors over the years, Collins has generated a fairly steady EBIT margin of between 8~11% over time, averaging about 10%.

Sources: Collins Foods, Contrarius Research

Return on Investment: We estimate that Collins’ Australian KFC business generated an average underlying return on company-wide equity of 15% per annum over the past decade. This is a healthy rate of return, and may actually understate Collins’ performance given the other investments it was making during the period (more on this below).

Collins is clearly a highly competent KFC franchisee and knows how to run a quick service restaurant. It also likely benefits from the fact that Yum operates in the fiercely competitive US fast-food market, facing off with formidable peers like Chick-fil-A, Popeyes, Raising Cane’s, and Wingstop. The challenging environment forces Yum to keep its eye on the ball, ensuring its menu remains appealing and its marketing effective. Innovations and learnings in the US can be applied to the Australian market, giving Collins an edge over domestic peers.

It is natural to wonder about saturation. The roughly 830 KFC restaurants spread across the country places Australia near the top of the list in terms of locations per capita. KFC is the lucky country’s third-largest fast-food chain by number of locations, trailing only Subway and McDonald’s. But it is also a far less competitive fried chicken market. While Chick-fil-A’s revenues are multiples of KFC’s US revenues (even with fewer locations), KFC’s chief competitors in Australia like Red Rooster and Oporto are significantly smaller.

Sources: Company filings and disclosures, Contrarius Research

In recent years, Collins has demonstrated that it can continue to roll out profitable Australian restaurants with attractive economics. The company aims to open 7~10 new restaurants annually with over 50 locations in its development pipeline. With further room to grow, the virtuous cycle of investment, network expansion, and attractive financial returns may continue for some time. Applying a long-term average ASX company valuation multiple (a conservative approach, in our view), we value Collins’ Australian KFC business (inclusive of debt) at roughly the same amount as the current market capitalisation of the entire company. If correct, this implies that by buying Collins’ shares today, one is getting Collins’ European KFC business for free.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

KFC Europe

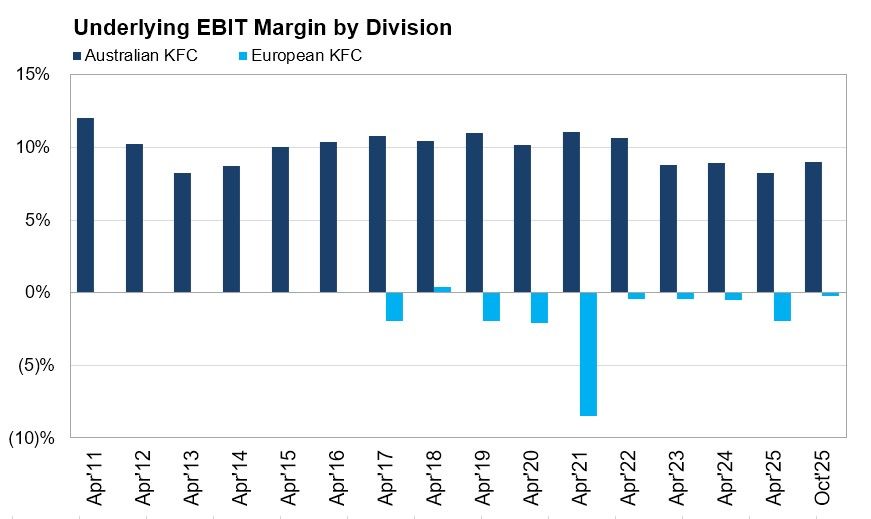

Collins first entered the European market by acquiring a handful of KFC restaurants in Germany and the Netherlands in 2016/2017. Further acquisitions have since followed and new restaurants have been rolled out, expanding its portfolio to about 80 restaurants across the two countries. Despite reaching this sort of scale, Collins has been unable to replicate its Australian division’s profitability. In fact, it has consistently lost money in Europe (see chart below). This has weighed on company-wide returns and likely been a source of repeated disappointment for investors.

Sources: Collins Foods, Contrarius Research

After a phase of rapid (unprofitable) expansion in the Netherlands, Collins is shifting gears by moderating restaurant roll-out plans, closing underperforming locations, and emphasising profitability over growth. In addition, it will hand back the marketing responsibilities in the region to Yum, allowing it to refocus on what it does best, i.e. operating restaurants efficiently. These are sensible and necessary strategic moves given the lengthy period of poor results.

Interestingly, weak results in the Netherlands have been masking very promising results in Collins’ other European market, Germany. In the year ended April 2025, Collins revealed that restaurant-level profitability across its 16 German locations rivalled those of its Australian division. A recently announced acquisition is expected to add a handful of similarly-profitable restaurants and lift its German location count to 25. There are plenty of reasons for optimism in this market. Firstly, KFC is significantly under-penetrated in Germany with only 217 locations in a country of 80 million people, compared to 1,400 McDonald’s and 750 Burger Kings. Secondly, Yum recently reacquired the German master franchise rights from an operator that severely dropped the ball in another region, suggesting weak leadership in the German market for the past two years. Yum appears best placed and highly incentivised to rectify this. Thirdly, the passing of a recent avian flu scare and the lowering of VAT for dine-in food purchases may benefit results in the near-term. Overall, Collins’ prospects in Germany look bright.

Summary

Collins is an excellent operator of KFC restaurants in Australia, but has struggled to replicate this success in the Netherlands or with other brands like Taco Bell. This has disappointed investors so much so that the market appears to be valuing its European division at zero (or perhaps less). We disagree with this appraisal, and instead believe there is significant optionality. Weakness in the Netherlands has hidden solid results in Germany, where Collins may have found its second high-returning avenue for capital investment, and one with an enormous runway. Continued profitable growth in Germany and improvement in the Netherlands both look probable to us, which could see earnings per share grow faster than the market expects. Choosing a bundled ‘Family Feast’ at your local KFC effectively means getting an extra side or two for free; we believe the same logic applies to Collins Foods today. In our view, investors are paying for the Australian operations and getting the entire European division—and its long-term growth potential—thrown in for free. At quarter-end, Collins is a Top 10 position in the Contrarius Australia Equity Fund.

Disclaimer: This article is based on a commentary prepared by Contrarius Investment Advisory Pty Limited (“Contrarius Australia”, AFSL 506315), investment manager of the Contrarius Australia Equity Fund (the “Fund”, ARSN 664 226 331). Equity Trustees Limited (“Equity Trustees”) (ABN 46 004 031 298), AFSL 240975, is the Responsible Entity for the Fund. Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT). Information is valid as at 31 March 2026. This information is general in nature and has been prepared without taking into account your personal objectives, financial situation, or needs. Before acting on this information, you should consider its appropriateness and should read the relevant Financial Services Guide (FSG), Product Disclosure Statement (PDS) and Target Market Determination (TMD) available at www.contrarius.com.au. The article is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, neither Contrarius Australia, Equity Trustees, nor any of their related parties, directors or employees, nor InvestmentMarkets (Aust) Pty. Ltd. as publisher, provide any warranty of accuracy or reliability in relation to such information, or accept any liability to any person who relies on it. Interested parties should seek independent professional advice prior to acting on any information presented. Past performance is not a reliable indicator of future performance. Funds managed or distributed by Contrarius Australia may have a position in any of the securities referred to in this article, and such positions are subject to change at any time without notice.

Chris Watson

Director at Contrarius Investment Advisory Pty Limited. Chris joined Contrarius Australia in January 2021. Chris was previously a director of Contrarius Investment Advisory Limited ("CIAL") in the United Kingdom from June 2017 until June 2018. He was employed by CIAL as an investment analyst from April 2012 until June 2018. Chris also previously worked for Allan Gray Ltd, South Africa’s largest privately-owned investment firm. He holds a Bachelor of Business Science (Quantitative Finance) from the University of Cape Town, and is a CFA and a CMT charterholder.

Author

Chris Watson

, Contrarius

Related Articles

-l7rg6lkopgoa2x6pxhua.png)

-4jjuh9ocumc2do1vonr2.png)

Investments You May Like

Contrarius Australia Equity Fund - Class A

The Fund employs Contrarius’ valuation-based, contrarian investment philosophy and aims to achieve long-term returns higher than the benchmark.

Contrarius Australia Balanced Fund

An actively managed asset allocation fund that invests in a portfolio of equities, fixed income and commodity-linked investments from Australia and globally. The Fund employs Contrarius’ valuation-based, contrarian investment philosophy.

Contrarius Global Equity Fund

The Fund employs Contrarius’ valuation-based, contrarian investment philosophy and aims to achieve long-term returns higher than the benchmark, without greater risk of loss.

Categories

Recent Articles

View all articles-lisv9065yh8k53n9c0n5.png)

-v8lxc7275hr89z0hzkrz.png)

-ulhzagvbsmdk2tc72zgj.png)