The Longer-Term Consequences of the US–Israel–Iran War

Simon Turner

Sun 3 May 2026 7 minutesBy now, most of us have realised that the US-Israel-Iran war will have longer-term consequences beyond recent volatility. It’s accelerating a structural shift in global markets defined by tighter energy supply, more persistent inflation, and the fragmentation of trade and capital flows.

The upshot is that investors who continue to rely on the low inflation, low interest rates, and global integration of recent years, risk being structurally mispositioned. Investors need to be ready for a world in which high and unpredictable geopolitical risk is embedded as an unfortunate, but constant, risk.

A Structurally Tighter Oil Market

The oil market is the poster boy of geopolitical risk at times like this.

For good reason.

The Strait of Hormuz remains the critical artery of global oil supply, with close to one fifth of the world’s traded crude passing through it. Any sustained disruption, even if partial, has immediate implications for both spot pricing and the forward curve.

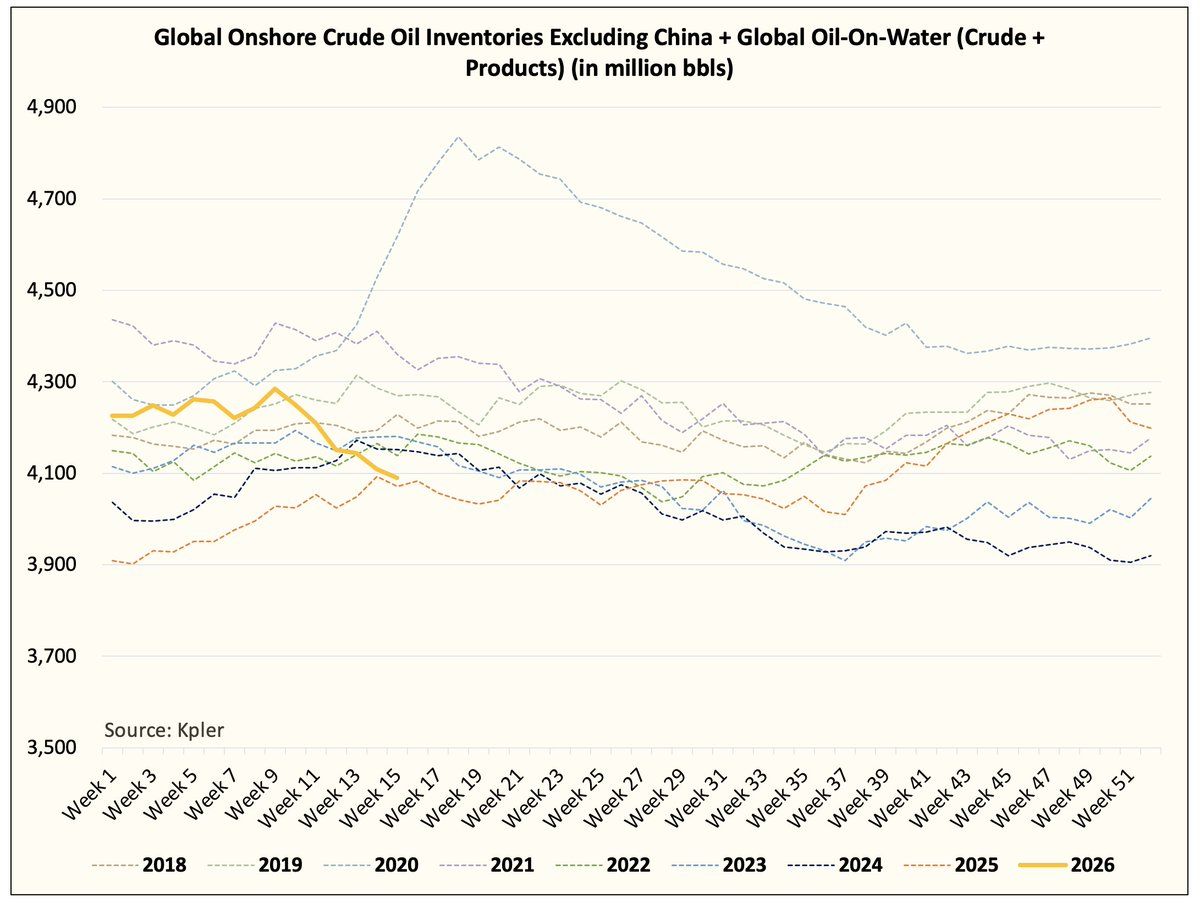

Recent estimates suggest that a significant portion of oil inventories have already been drawn down as a result of the war.

Each additional week of disruption in the Strait of Hormuz compounds that drawdown and tightens the global balance further.

This backdrop is changing the way markets price geopolitical risk.

Oil is no longer being valued purely on cyclical demand expectations. Instead, a structural geopolitical risk premium is being embedded across the futures market, reflecting the growing awareness that supply disruption is now a persistent feature of the system.

The longer-term oil price outlook is adjusting to this unfortunate reality.

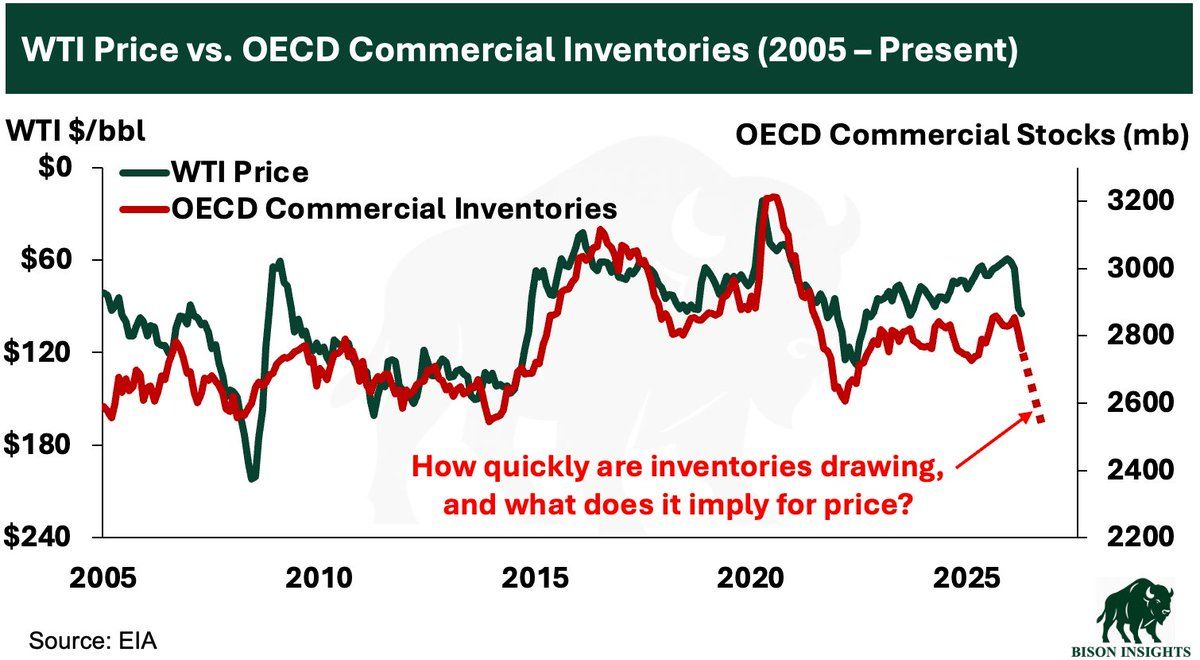

Historically, there has been a close relationship between OECD commercial inventories and oil prices (see chart below), with lower inventory levels corresponding to higher and more volatile pricing regimes. If inventories continue to fall, the implication is clear: the floor for oil prices rises, and with it the baseline for global inflation.

This marks an important shift for investors.

Energy exposure has arguably evolved into a structural allocation for all portfolios seeking resilience to rising geopolitical risk and further supply-side shocks, both of which are more likely.

In addition, renewables and nuclear energy are likely to benefit from a tighter oil market as the value of alternative energy sources increases. Ensuring your portfolio is exposed to benefit from future energy demand which is consistent with the energy transition remains a worthy consideration.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Inflation is No Longer Transitory

A rising oil price has major economic ramifications as it remains one of the most important input costs in the global economy. As energy prices rise, they feed directly into transportation and manufacturing costs, and ultimately consumer prices.

The RBA has already emphasised that ‘persistent supply shocks can entrench inflation expectations.’

This has become a very real risk, particularly given Australian inflation remains above the central bank’s 2-3% target band, and the transmission from higher energy costs to broader price pressures is already visible in key sectors.

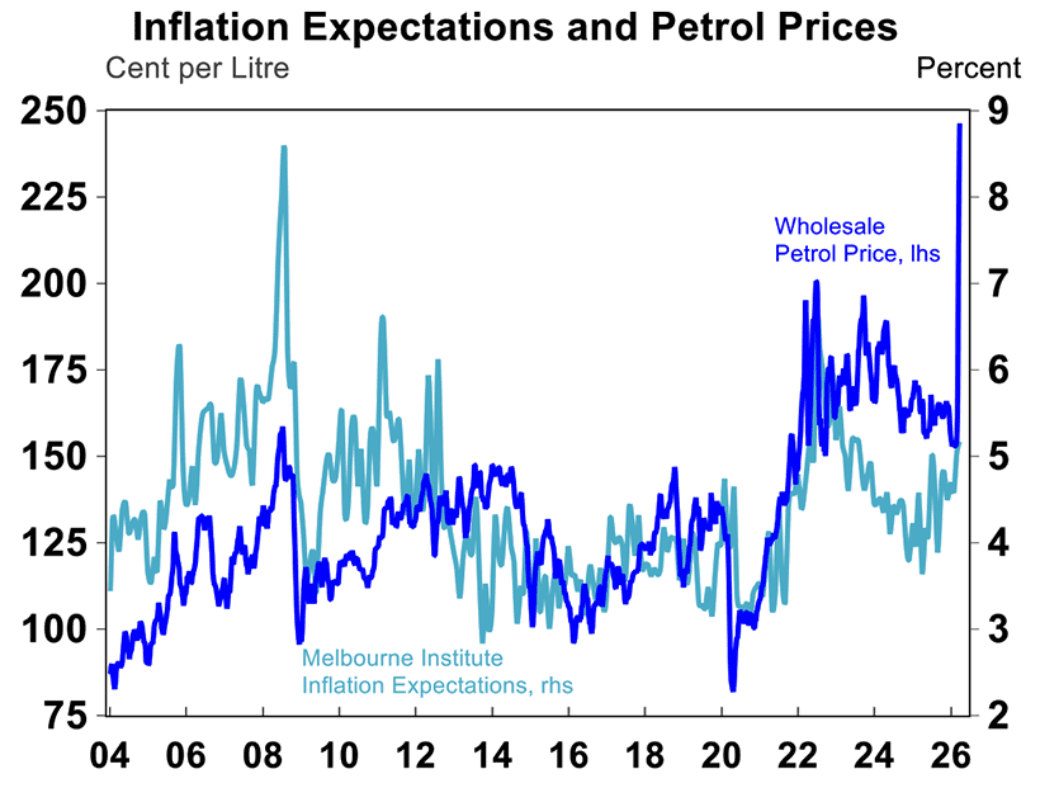

The correlation between petrol prices and inflation expectations is an ominous signal of what’s to come.

The implications for monetary policy are significant.

The RBA and other central banks may be forced to maintain tighter settings for longer, even as growth slows.

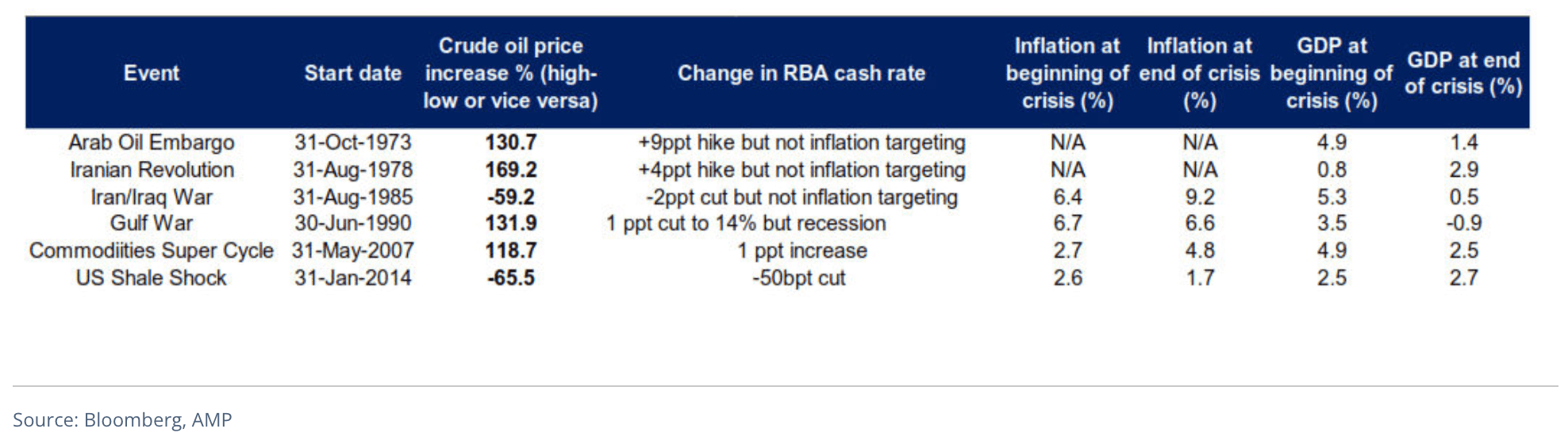

This raises the risk of stagflation. While the current environment differs from the 1970s in terms of globalisation and financial system depth, the underlying dynamic of supply-driven inflation is comparable. That’s worrying.

Higher inflation expectations change the role of fixed income in a portfolio context.

Long-duration government bonds, which performed strongly in a disinflationary world, have become more vulnerable to rising policy rates.

In this environment, the prudent emphasis arguably shifts towards shorter-duration exposures, inflation-linked securities, and actively managed income strategies that can adjust to changing rate expectations.

Defence and Real Assets in a Structural Upcycle

At a fundamental level, the conflict is accelerating a broader repricing of geopolitical risk. Sadly, conflict tends to lead to more conflict, and the risk of a rise in terrorism has surely risen as a result of events in Iran.

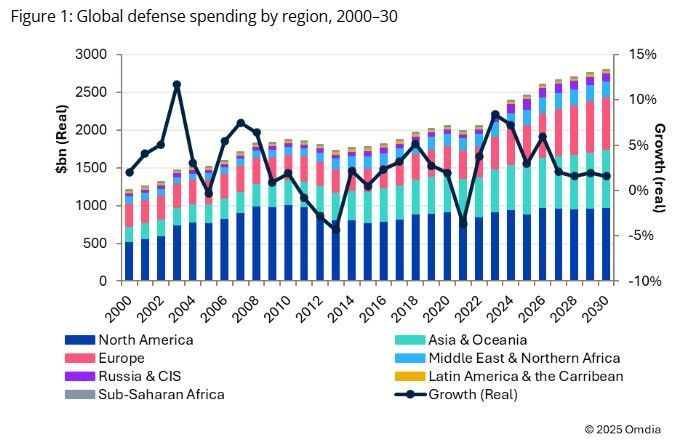

The global defence sector is a key beneficiary.

Defence spending has been rising steadily since 2022, with NATO members and other developed economies committing to sustained increases in military budgets. This reflects a reorientation of fiscal priorities towards national security.

As a result, funds and ETFs exposed to defence, infrastructure, and real assets are likely to benefit from long-term spending commitments and inflation-linked revenue streams. By contrast, those that rely heavily on global supply chains or low input costs may face ongoing pressure.

Real assets more broadly, including infrastructure and defensive property segments, take on renewed importance. Assets with pricing power and contractual revenue linked to inflation are valuable anchors within portfolios seeking to preserve real returns.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Currency Dynamics Are More Complex

In the previous decade, characterised by relative stability and synchronised global growth, currency effects were often secondary. That’s no longer the case.

Currency has re-emerged as a meaningful driver of returns.

For Australian investors, the interaction between the Australian dollar and the US dollar is particularly important.

On one hand, the US dollar has historically strengthened during periods of global uncertainty. On the other, elevated and rising US debt levels and Trump’s spend-heavy policies introduce questions about the durability of that safe haven status.

At the same time, Australia’s position as a commodity exporter creates a countervailing force. Higher resource prices may support the Australian dollar, even as global risk sentiment deteriorates. The result is a more nuanced environment in which binary hedging decisions are less effective.

Partial hedging strategies, which balance the benefits of diversification with the risks of currency volatility, may offer the most robust approach in this chaotic market.

Fragmentation Reshaping Global Diversification

One of the most underappreciated consequences of the war is the fragmentation of global trade and capital flows. The world is moving towards a more regionally aligned system, in which economic relationships are increasingly shaped by geopolitical considerations.

On that note, IMF research suggests that rising geoeconomic fragmentation could materially impact the global economy over the long term.

The implication is that traditional diversification may not provide the protection it once did. Broad global indices may be masking concentrations in regions or sectors that are vulnerable to disruption. For example, most global ETFs are heavily overweight US big tech.

Intentional diversification is becoming more important as a result.

Active global equity funds, particularly those that incorporate geopolitical analysis into their portfolio construction, may offer a more resilient approach than purely passive exposures.

An Evolving Role for Gold

Gold has historically performed well during periods of geopolitical stress, rising inflation, and US dollar weakness. So, it’s a perfect match to the current macro environment.

It serves two roles: it acts as a hedge against systemic risk, and as a store of value in a world where fiat currencies may be subject to greater volatility.

So, the role of gold ETFs and funds within portfolios is to provide stability when other assets are under pressure.

Major Changes Afoot

The implications of the US–Israel–Iran conflict signal the emergence of a new investment era in which geopolitical risk, energy security, and inflation volatility are central drivers of returns.

Portfolios that incorporate real assets and resources, manage duration risk carefully, remain flexible on currency exposure, and diversify with intent are more likely to withstand the challenges ahead. Disciplined portfolio construction and a willingness to adapt are emerging as the defining characteristics of successful investors in this new world.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.