Investors are familiar with the positives of adding global equities to their portfolios. Think diversification, exposure to some of the biggest companies in the world and the potential to access different growth themes.

In the desire to be sure you’ve captured the likes of Nvidia and Amazon in the portfolio, it’s easy to suddenly find that you are not as diversified as you hoped and subject to risks you hadn’t planned for, beyond the usual concerns of investing in equities.

In this article, I’ll explore five key mistakes that investors in global equity funds can make and how to avoid them and the ways to manage these risks.

1. Currency risk

Investors often forget that when they invest in international equities, either directly or via a managed fund, they are buying in the local currency of those equities. This will affect the value of any dividends or income you might generate from those investments, or the value of the principal you’ve invested.

If the Australian dollar takes a hit against other currencies after you’ve already invested, this could be good news – your income will convert higher and the value of your principal converted back will be higher. However, if the Australian dollar gains, your returns and principal will look lower.

Some investors might want currency exposure in their portfolio and use it as a deliberate part of their strategy. Investors who are concerned about currency risk may choose to hedge their portfolio. This is where the fund manager will dedicate an allocation towards currency derivatives or other types of currency trading to reduce the impact of currency movements on the portfolio.

Some fund managers will offer both unhedged and hedged forms of their strategy to allow investors to make the choice as to whether they would like the currency exposure, or not.

For example, Claremont Global offers the Claremont Global Fund Active ETF (ASX: CGUN) in a currency-hedged format, the Claremont Global Fund (Hedged) Active ETF (ASX: CGHE). The hedged format uses derivatives only for currency hedging to a minimum of 90% of the gross asset value of the fund.

Alternatively, investors may choose to add a separate currency investment to help manage their exposure.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

2. Tax implications

The tax arrangements on foreign investments can be more complicated compared to simply investing in Australian assets.

You’ll be taxed on your returns both locally and internationally, because the companies you invest in will be subject to their local regimes.

In some cases, you may receive a foreign tax offset on your Australian tax return for tax you’ve paid on returns from international equities – the advantage of using managed funds is that this will be outlined in your annual statement if applicable and in Australian dollars so you won’t have to work out each individual equity gain.

Remember that franking credits only apply to local equities (and only if those local companies offer franking).

When you sell your investments, these are still subject to capital gains tax, which may also be applicable in the countries of origin for the investments.

You’ll also need to consider how currency may have changed your returns, either creating a larger gain or diminishing your returns.

Some funds may require you to fill out forms for tax withholdings in other countries. For example, US investments may require you to fill out a W-8BEN form that identifies you as a foreign investor to the US Internal Revenue Service (IRS) and allows you to claim tax treaty benefits.

Funds that are domiciled in Australia usually allow you to avoid needing to fill out these forms, for example, Australian listed ETFs like Betashares Nasdaq 100 Equal Weight ETF don’t require a W-8BEN form to be completed, you’d just need to follow other typical investment requirements, such as declaring your Australian tax file number.

3. Concentration and ‘Diworsification’

To the logophiles among the InvestmentMarkets readers, my apologies for ‘Diworsification’. For everyone else, this is a descriptor coined by American fund manager Peter Lynch to explain how an attempt to diversify doesn’t add value to a portfolio, making it worse, because of factors like excessive correlation, a lack of quality or flattened returns due to too many stocks.

Sometimes adding global equities for diversification doesn’t achieve what you’d normally hope for and this comes down to the concentration in the market.

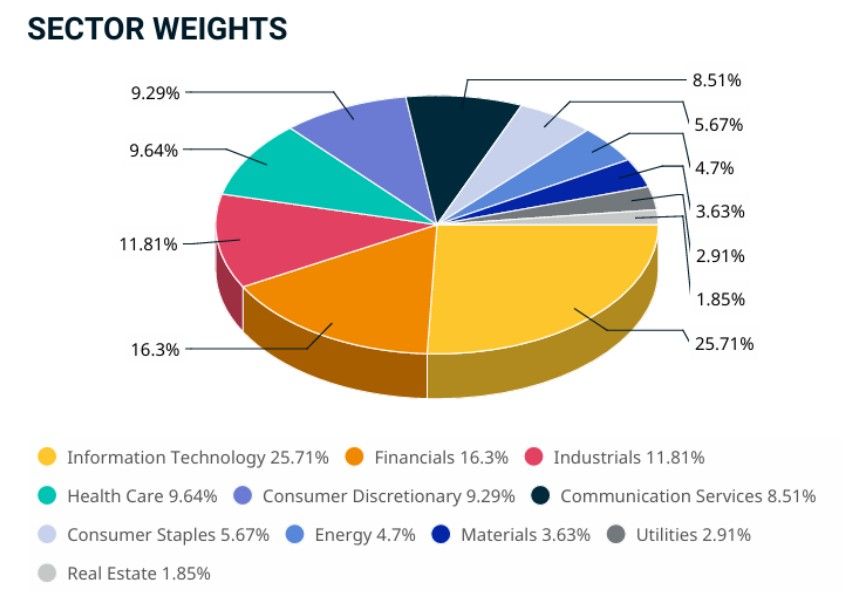

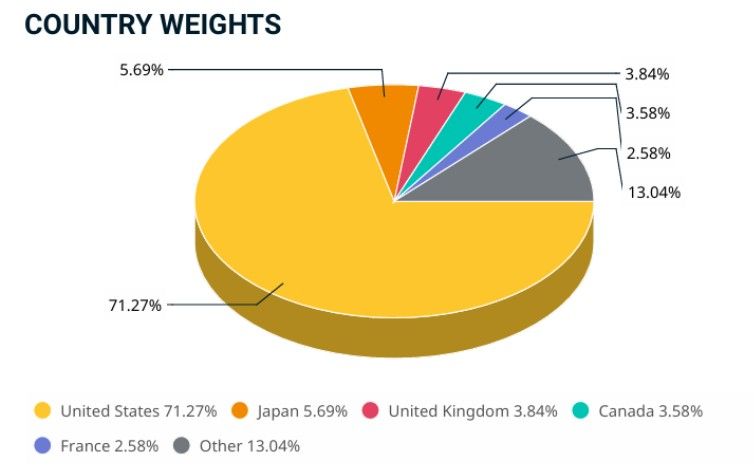

Consider that indices are usually weighted by market capitalisation (that is how large a company is) and the US holds 18 of the 20 largest companies in the world, according to Forbes. The US dominates over 70% of the MSCI World Index which holds 1,311 companies.

If you look at the sector breakdown too, you’ll find that over ¼ of the index is directed to information technology companies, but also that the top 10 companies are dominated by the Magnificent Seven and represent close to a quarter of the index so will have an undue influence on the returns of the index.

Source: MSCI World Index factsheet dated 31 March 2026

If you already had exposure to the Magnificent Seven and wanted to diversify your exposure, you’d find that simply adding a broad-based index would build your concentration risk and, while it does add many stocks to the mix, it wouldn’t be offering adequate diversification.

You can avoid this by taking the time to look through the investments within the global equity funds you want to use to avoid doubling-up on investments and understanding whether there is a concentration and you are happy to have that concentration in your portfolio. After all, concentration can be a good thing in some circumstances. Investors would have been happy to be concentrated in the Magnificent Seven and other US large-cap tech over the past few years, but might be more concerned about valuations now.

Some investors might choose to reduce concentration risk by using equal-weight indices instead of market capitalisation weighting so that there isn’t undue influence from just a few stocks. An example of this is the Betashares S&P 500 Equal Weight ETF (ASX: QUS).

Or they may choose global equity funds which can complement each other by investing in different regions or assets. For example, using a fund like Fidelity Asia Active ETF (ASX: FASI) which focuses on investing in Asian companies, alongside a more traditional developed market index like VanEck MSCI International Value (AUD Hedged) ETF (ASX: HVLU) which will still be more concentrated towards US large-cap tech.

4. Geographic risks

Not all economies operate in the same political and legal framework as Australia and this can change the types of risks involved in investing in companies listed in those countries.

When people consider geographic risks, they have typically in the past considered emerging market countries where there can be rapid change and political turbulence that flows through to companies. It’s worth remembering developed countries can also have periods of turbulence and disruption.

Going further, geographic risk doesn’t just relate to where a company is domiciled and listed. It can also be about where and how it conducts its business.

If you look at current world events, companies that operate in countries with a greater oil dependency or the need for fertilisers for crop production will be challenged, whether they are listed in the United States or United Kingdom. Stating the obvious, those companies that operate in conflict zones will also be challenged.

A country’s economic situation can also influence market performance so having too much exposure to one region can cause problems too.

As mentioned in the last point, international equity indices typically have a US bias.

Source: MSCI World Index factsheet dated 31 March 2026

As the saying goes, when the US sneezes, the world catches a cold, so it can be valuable to see what options you have for managing disruptions in the US in other parts of your portfolio and adding exposures to other regions so your global equities aren’t just US equities.

You can’t always avoid geographic risk, but what you can do is take the time to understand the geopolitical environments you are investing in and what this might mean for the companies in your portfolio and your eventual returns. You may choose to offset traditionally more volatile markets (which can come with high-growth) with those that have demonstrated stability and consistency over the long-term.

When adding to your global equity exposure, consider your existing investments and what would complement these. For example, if you hold a US dominated portfolio, you may wish to add Europe or Asian focused funds for diversification or to change the geographic risks.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

5. Valuation risk

This is a challenge often associated with passive investing – the risk that the underlying investments in a fund are trading above their intrinsic value, driven by market sentiment. As passive investments focus purely on index weightings and maintaining these, investors can be highly exposed to bubbles and market volatility.

For example, there are concerns about stretched valuations in US large-cap stocks and many index funds are weighted in favour of these rather than markets where there may be better value and opportunity.

Investors concerned about this could consider styles focused on quality and value, along with contrarian active management. For example, the Antipodes Global Value Active ETF (ASX: AGX1) which focuses on value equities or the Contrarius Global Equity Fund which takes a contrarian view against the market in its selection.

They may also choose to add selective tilts to funds that invest specifically in markets where there might be better value.

True global diversification

Risks are an inescapable part of investing, so investors shouldn’t shy away from global investing on the basis of challenges like currency, tax or a US bias.

It comes down to understanding the underlying investments, how they work alongside each other and with other parts of your portfolio and whether they actually achieve what you need when you add them.

It’s also helpful to remember that, just as concerns like currency risk can be a problem if you aren’t aware of them, for some investors, they can be a strategic exposure in the portfolio that can be useful when accounted for carefully in the full context of your portfolio. The biggest mistake at the end of the day is failing to take the time to invest carefully and do your research with your goals and strategy in mind.

Funds Mentioned

The Fund’s objective is to provide an attractive risk-adjusted return in excess of the Benchmark over a rolling 5-7 -year period.

Retail Investor

Availability

Open for investment

The Fund’s objective is to provide an attractive risk-adjusted return in excess of the Benchmark over a rolling 5-7 -year period that is hedged for foreign currency exposure.

Retail Investor

Availability

Open for investment

QNDQ aims to track the performance of the Nasdaq-100 Equal Weighted Index (before fees and expenses). The Index provides exposure to 100 of the largest non-financial companies listed on the Nasdaq market, with each holding in the Index weighted equally.

Retail Investor

QUS aims to track the performance of the S&P 500 Equal Weight Index (before fees and expenses). The Index provides exposure to 500 leading listed US companies, with each holding in the index weighted equally.

Retail Investor

The Fund provides investors with the potential for long-term capital growth by investing in a concentrated number of companies located in Asia, as well as companies located elsewhere that derive a significant proportion of their earnings from Asia (Asian Securities)

Retail Investor

HVLU gives investors a diversified portfolio of 250 international developed market large- and mid-cap companies, with high value scores as calculated by MSCI at each rebalance with returns hedged into Australian dollars. HVLU aims to provide investment returns before fees and other costs which track the performance of the Index.

Retail Investor

The Fund employs Contrarius’ valuation-based, contrarian investment philosophy and aims to achieve long-term returns higher than the benchmark, without greater risk of loss.

Retail Investor

Availability

Open for investment

Funding Stage

Unlisted Mature Fund

The Antipodes Global Value Active ETF is an exchange traded managed fund quoted on the ASX, otherwise known as an active ETF, offering investors access to a long only global securities portfolio via a single trade. The fund's fundamental, pragmatic value-focused approach focuses on buying great but undervalued companies and building a concentrated portfolio of at least 30 holdings.

Retail Investor

Disclaimer: This article is prepared by Sara Allen. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

-zdalarekmzl2x534cuyn.png)

-l7rg6lkopgoa2x6pxhua.png)

-4jjuh9ocumc2do1vonr2.png)

-v8lxc7275hr89z0hzkrz.png)

-ulhzagvbsmdk2tc72zgj.png)

-weh3swd4zyleexypgsv3.png)