The Major Shift in Fund Management Isn’t What You Think

Simon Turner

Mon 20 Apr 2026 7 minutesThe decade-long narrative in funds management has been that passive investing is winning at the expense of active management. It’s hard to argue with that. Fees have fallen, passive fund transparency has improved, and cost-focused investors have taken advantage of the opportunity.

Yet this one-dimensional framing of the industry’s recent journey misses another important structural shift unfolding beneath the surface: not active versus passive, but listed versus unlisted. Understanding this distinction is becoming more important for ETF and fund investors.

The Rise of ETFs

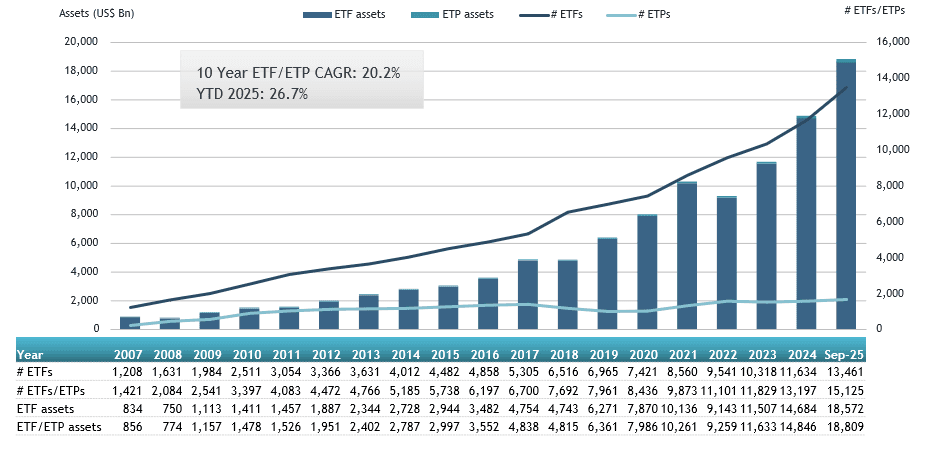

The rise of ETFs has been undeniable. Global ETF assets have surged past US$14 trillion with a growth rate of over 20% p.a., while in Australia the ETF market has grown to well over A$200 billion, expanding at a pace that continues to outstrip traditional managed funds.

The rapid growth has illustrated the importance of cost and efficiency as drivers of investor behaviour.

On the surface, this appears to confirm the unequivocal triumph of passive investing over active.

However, a closer examination reveals a more nuanced reality.

While passive strategies continue to dominate net inflows, the fastest-growing segment of the ETF market has actually been active ETFs. This segment has expanded rapidly in both number of funds and AUM (assets under management) in recent years.

That’s an interesting development in a passive market which has been growing its market share at the expense of the actively managed market.

Digging a little deeper into this, here are the top ten active and complex ETFs by flows for the year to the end of February 2026:

As you can see, these ETFs have all enjoyed remarkably strong inflows over the past year.

But this trend warrants interpretation.

According to Marc Jocum from Global X, whilst active and complex ETFs now account for more than one-third of the ETF sector’s market cap, they represent just 20% of its AUM and 14% of its recent inflows.

In other words, a significant proportion of funds entering the active ETF AUM have not come from new capital, but from existing unlisted strategies being converted listed structures.

In some cases, entire funds have migrated into active ETF wrappers, effectively relabelling products rather than attracting new assets.

Hence, part of the growth attributed to active and complex ETFs of late reflects structural change rather than a decisive shift in investor preference.

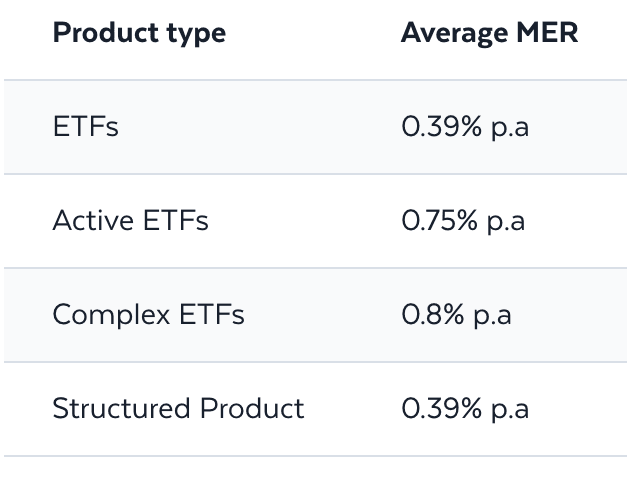

Given the average fee for an active ETF is 0.75% p.a. versus 0.39% p.a. for ETFs in general, how can we reconcile growth in active ETFs, and the growing interest amongst managers of unlisted private capital in converting their existing funds to active ETFs?

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

What’s Going On?

At this point, we probably need to question the widely accepted view that investors are abandoning active management in favour of passive strategies.

In many cases, they aren’t.

They’re just demanding different ways of accessing active strategies, including within the private markets.

In short, the appeal of listed vehicles is rooted in their continuous pricing, intraday liquidity, and immediate access, all of which have become increasingly valuable in a market environment defined by speed and uncertainty.

The ability to adjust positions quickly, respond to macro developments, and maintain flexibility are significant benefits for most investors.

The ETF boom has also injected new dynamics into this picture.

Market pricing can diverge, for example, from underlying asset values, particularly in more specialised exposures such as thematic or credit-focused ETFs.

Discounts and premiums can emerge, and volatility can be amplified by flows rather than fundamentals.

These are features of a system that prioritises liquidity.

Unlisted funds, by contrast, operate with different constraints and advantages.

Their periodic pricing mechanisms and longer investment horizons can dampen short-term volatility and allow managers to take a more patient approach, particularly in less liquid asset classes. This structural difference has become increasingly important as investors expand into private markets, real assets, and credit strategies that are less compatible with daily liquidity.

Back to the recent industry shift. Listed structures, including active ETFs with exposure to private markets, are gaining share because they better align with current investor preferences, although unlisted strategies continue to play a critical role where liquidity is less important than access or time horizon.

So, the rapid expansion in the number of active ETFs reflects growing demand for strategies that go beyond traditional index tracking, although their growth has also been shaped by the migration of existing funds into listed formats. This has created the appearance of innovation, even where the underlying investment approach remains unchanged.

The Important Question

Knowing this, the question for investors is: when allocating to an active ETF, are you accessing genuinely new sources of return that you couldn’t access through another, potentially cheaper, product?

This question is increasingly important in a market where structure and strategy are becoming more intertwined while investors are becoming more informed and demanding.

The issue is: low cost by itself is no longer enough to attract new assets. Investors expect transparency, consistency, and a clear articulation of how a strategy fits within a broader portfolio.

Context also matters. The seemingly never-ending expansion in the number of ETFs is creating new layers of complexity. This is increasing the burden on investors to distinguish between substance and structure.

They also need to understand that the debate between active and passive fails to account for the ways in which strategies are being repackaged, redistributed, and accessed.

It’s important to consider the role of structure within a portfolio:

Listed vehicles excel in providing liquidity, flexibility, and real-time pricing, making them well suited to core exposures and tactical adjustments.

Unlisted funds, by contrast, offer access to opportunities that require patience, illiquidity, and a longer investment horizon, particularly in asset classes such as private credit and real assets.

The most effective portfolios recognise that these characteristics are complementary rather than competing.

The objective is to deploy each where it is most effective.

Seen in this light, the apparent dominance of passive investing is arguably less definitive.

Yes, ETFs continue to attract the majority of flows. But the migration from unlisted to listed structures represents a reconfiguration of the investment ecosystem, one that emphasises accessibility and flexibility without fundamentally altering the underlying sources of return.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Structural Context Matters

Fund and ETF investors need to be alert to the way the fund management world is evolving. Success depends on understanding the structural context in which investment philosophies are expressed. Labels such as active and passive remain useful, but they no longer tell the whole story.

This is a longer-term theme. The maturing of the industry will be shaped by the interaction between structure and strategy, and the ability of investors to navigate that relationship with clarity and discipline. In other words, the debate has moved on, even if the headlines haven’t.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.