How well is your fixed income investment portfolio expected to perform during an economic shock? Have you considered what could happen to your portfolio if the wrong things happen at the right time? How defensive will your fixed income investments be in the next economic crisis?

Most people's understanding of investment risk is incomplete, and it usually stays that way until a loss of capital, or an unplanned, excessive volatility event forces the question. Why is it that people tend to ask the most questions about their investments only after a bad experience? It is better to learn to swim before jumping into the deep end. Understanding risk before you invest is safer, in the same way that learning to swim reduces your risk of drowning.

This paper sets out a framework for understanding the risks investors are exposed to and closes by connecting that framework back to the specific risks embedded in fixed income instruments.

The three risks every investor carries

Investment risk can be separated into three categories: the unavoidable erosion of inflation, the possibility of a permanent loss of capital, and volatility, which is not itself a permanent loss but can turn into one if it is misunderstood or mistimed.

Inflation risk: the unavoidable loss

Inflation is a permanent, unavoidable loss of purchasing power. It is not measured in a negative return on a statement, but the cost is real, and it is realised every time you make a purchase or pay tax.

In Australia, cumulative inflation between 1976 and today has been substantial: prices today are roughly 7.9 times higher than they were fifty years ago, and the purchasing power of a dollar has fallen accordingly. Put another way, around 13 cents in 1976 bought what $1.00 buys today. Averaged over that period, the annual inflation rate has run at roughly four percent, meaning an after-tax return needs to clear that bar just to preserve wealth, before any real growth begins. (Note: these figures are a close estimate based on published CPI series; the precise cumulative and average figures should be sourced directly from the Australian Bureau of Statistics or RBA inflation calculator accordingly.)

There are only two effective ways to mitigate the permanent loss of wealth caused by inflation:

Invest for growth by taking on planned, understood investment risk; and

Spend less.

Permanent loss of capital risk

Permanent loss of capital is frequently confused with volatility, but the two are distinct. Permanent loss typically results from overallocation of capital to a single investment, investment type, or market, without planning for what happens if the worst case occurs. To understand where this risk comes from, it helps to separate it into three sources.

Risk is only harmful when it is unplanned or not understood before you invest.

Three sources of permanent loss

Systemic risk

A single institution's or sector's failure cascades through the wider financial system.

Example: the 2008 collapse of Lehman Brothers, which triggered a global financial crisis as losses spread through interconnected institutions.

Systematic (market) risk

Broad, economy-wide factors that affect nearly every asset at once: inflation, interest rate cycles, recessions, geopolitical shocks, pandemics.

This risk cannot be diversified away, because it does not come from any single holding, it comes from the market itself.

Unsystematic (specific) risk

Risk that is unique to a single company, fund, or industry: poor management decisions, financial instability, product failures, or sector-specific regulatory change.

Example: recent Australian fund collapses, including First Guardian, Shield Master Fund, and Australian Fiduciaries, reflect failures specific to those funds rather than a system-wide event.

This is the one category of the three that diversification can meaningfully reduce.

The distinction matters because the correct response differs by category. Diversification across companies, funds, and sectors reduces unsystematic risk. It does very little for systematic risk, which requires asset allocation and hedging instead, and even less for systemic risk, which is best managed by never being so concentrated in one institution or counterparty that its failure would be catastrophic to your financial position.

Mitigations specific to permanent loss of capital:

Set a maximum allocation to any single investment, fund manager, or counterparty, and hold to it even when a position is performing well.

Diversify across investments, companies and sectors to reduce unsystematic risk specifically, recognising this step does not protect against systemic or systematic shocks.

Hold a portion of the portfolio in assets with low correlation to your core holdings, as a partial hedge against systematic risk.

Before investing, write down what a total loss of the position would mean for your overall financial position, and only proceed if that outcome is survivable.

Unplanned excessive volatility event risk

Volatility itself is not a permanent loss of capital. An asset's price can fall sharply and recover fully, in which case an investor who held on experiences no lasting damage. The risk lies in being forced to sell during the decline, which converts a paper loss into a permanent one.

It is useful to think of a price cycle as a clock face: 12 o'clock represents the cyclical peak of an asset's valuation, and 6 o'clock represents its trough. Investors most often buy in when prices are above 9 o'clock, on the way up toward the peak, and are then forced to sell once prices fall back below 4 o'clock, near the bottom, crystallising a loss that a more patient or better-timed investor would never have realised.

Australian bank shares are a useful illustration: a stock like Commonwealth Bank can fluctuate more than fifty percent from peak to trough over a short period without any of that volatility representing a permanent loss of capital for an investor who was not forced to sell at the low point.

Mitigations specific to volatility risk, distinct from those above:

Buy when prices sit below the 3 o'clock to 9 o'clock band on the cycle, rather than chasing prices already near the peak.

Maintain a cash or liquidity buffer outside the volatile position, sized to your near-term spending needs, so a market downturn never forces a sale.

Match the investment's expected holding period to your own timeline, so a temporary decline does not collide with a need for the funds.

What this means for fixed income specifically

The framework above applies to any asset class, but fixed income carries its own version of each risk, and a fixed income investor should translate the general framework into these specific terms before allocating capital.

Interest rate risk (a form of systematic risk): bond prices move inversely to interest rates, so a rate rise reduces the market value of existing fixed income holdings, even where the issuer's creditworthiness is unchanged. This risk is readily evident in the prices of listed fixed income investments.

Credit risk (a form of unsystematic risk): the risk that a specific issuer defaults or is downgraded, directly reducing that holding's ability to pay coupons or return principal. This risk isn't readily evident until after the fact and usually plays out during times of economic shock.

Duration risk: longer-dated bonds are more sensitive to interest rate movements than shorter-dated bonds, amplifying the systematic risk described above.

Reinvestment risk: when a bond matures or is called, proceeds may need to be reinvested at a lower prevailing rate, eroding the income the portfolio was built to deliver.

Liquidity risk: some fixed income instruments, particularly private credit and unlisted notes, cannot be sold quickly without a price concession, which matters directly for the volatility mitigation of maintaining a separate liquidity buffer.

A fixed income investor applying the framework above should therefore ask, for every holding: what is its duration and interest rate sensitivity, what is the credit quality of the issuer, how easily can it be sold if needed, and does its maturity profile match a point in time when the funds are actually needed.

How are fixed income returns generated and paid

Most fixed income investments generate returns by lending or investing capital from investors and achieving a higher return on that capital (after costs and losses) than what they are paying their investors.

Fixed income investments come in various forms, both listed and unlisted, and can include, amongst others:

Bank term deposits (usually fixed terms, with very limited variables).

Government and corporate bills, notes and bonds (usually fixed terms, with limited variables).

Funds (often highly variable terms).

Investment terms can be fixed or variable, as can interest payments.

Market sectors can include all asset classes and market segments: companies, consumers, real estate, and derivatives, with very different underlying risk and return profiles. For example, consumer home loans are very different to real estate development loans.

It is important for investors to understand that fixed income investments paying higher returns are likely achieving this by taking on higher risk, and that some fixed income investments carry equity-style risks in their underlying assets.

Conclusion

Inflation guarantees a loss of purchasing power that only growth-oriented investment and disciplined spending can offset. Permanent loss of capital comes from three distinct sources, systemic, systematic, and unsystematic, each requiring a different mitigation. Volatility is not itself a permanent loss but becomes one when an investor is forced to sell at the wrong point in the cycle. Understood and planned for in advance, each of these risks becomes manageable; left unexamined until after a loss occurs, each becomes a lesson learned the hard way.

The section below applies this framework to one fixed income instrument, so that a reader can see the checklist used in practice rather than only in the abstract.

Applying the framework: CRAFT Fixed Term Fixed Income Notes

CRAFT Fixed Term Fixed Income Notes offer a fixed interest coupon. The following sets out the note's key terms against this paper's own risk checklist and is explicit throughout about which figures come from independent, third-party market data and which are reported by CRAFT about its own book, since the two are not the same kind of evidence and should not be read as directly interchangeable.

Fixed term: 5 years, with an early redemption option available at 27 months, subject to an interest rate adjustment.

The note structure does not provide for voluntary suspension of interest payments or redemptions by the investment manager.

Credit risk (unsystematic)

CRAFT Fixed Term Fixed Income Notes underlying market segment and asset call (commodity supply chain finance loan receivables and investments) supports the real economy being the flow of essential materials, energy and food that societies must have to continue to function.

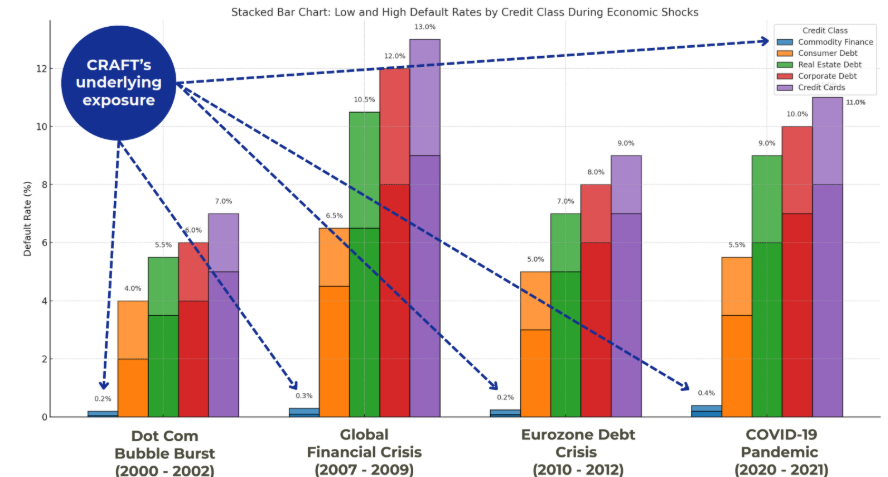

CRAFT's underlying asset class performs just as well during economic shocks as it does in normal markets. There are very few genuine risk-adjusted product opportunities available to investors that offer confidence in positive outcomes when markets are in turmoil. Most investment products are "risk-on" capital investments during market crises.

For example, during the Global Financial Crisis, real estate-linked credit recorded default rates of 10.5%, around 35 times higher than CRAFT’s underlying credit market segment, which recorded default rates of 0.3%. In addition, defaults in CRAFT’s underlying market segment have historically shown a much lower correlation with actual write-offs or write-downs.

This chart shows why investors can be confident in the performance of CRAFT's underlying assets. It also shows how other asset classes perform during market crises.

The macro data presented here covers all markets (developed and developing) and all market participants (including established and start-up companies, as well as large, medium, and small enterprises).

The Lowest Default Credit Risk of All Lending Markets

Sources: WSJ / S&P Global (2024); S&P Default Studies (2023); FRED CRE Loan Delinquencies (2008–09); PayNet/Experian SME default trends (2024); ICC Trade Register, ADB (2021)

In normal market conditions, the statistical default rate for CRAFT’s underlying market segment is typically below 0.1% and has historically remained below 0.5% even during periods when other lending markets have experienced significant losses. Importantly, defaults in CRAFT’s underlying market segment have historically shown a low correlation with actual write-offs, which compares favourably with other lending markets where defaults are more likely to translate into realised credit losses, particularly during economic crises.

CRAFT’s own market segment performance is stronger again than the macro-level statistical data suggests. Within its lending universe, CRAFT deals only with large, established Tier 1 and Tier 2 companies in the real economy that operate sophisticated supply chains in developed Tier 1 markets, with no mainland China exposure. When CRAFT’s screening process is applied to this universe, no write-offs were identified over the relevant historical periods. This screening process is therefore a critical contributor to the observed zero-default and zero-write-off outcomes at the underlying asset level.

For these reasons, CRAFT Notes offer one of the stronger risk-adjusted return profiles in the fixed income market. They may provide an attractive alternative to bank hybrids and may also complement real estate-linked private credit within a diversified fixed income allocation.

Interest rate and duration risk (systematic)

Investors need to judge whether a fixed coupon interest rate of 8.00% pa, fixed for 5 years, offers a compelling return after adjusting for inflation, for the credit risk evidence set out above, and for the note's liquidity constraints described below.

Liquidity risk

Capital is committed for a minimum of 27 months before any redemption option applies, subject to the interest rate adjustment noted above, and the notes are unlikely to have a liquid secondary market in the way listed securities do. Applying this paper's own volatility mitigation, an investor should hold sufficient liquidity outside this position to cover any spending needs that might otherwise force an early or forced exit.

Reinvestment risk

At the 27-month early redemption point or at the 5-year maturity, proceeds would need to be reinvested at whatever rate then prevails, which may be higher or lower than the original 8% coupon.

None of the above is a statement that these notes are unsuitable; it is the same due-diligence checklist this paper sets out for any fixed income holding, applied consistently rather than waived for this instrument.

Disclaimer: This article is prepared by the CRAFT Fixed Income Team. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Retiring soon and wondering how to structure your investments? There are a range of strategies you can follow, from maintaining your existing approach to shifting into a new strategy. One approach investors use is known as the 3-bucket strategy.

When you are investing for income, you are looking for capital preservation, a level of growth and consistent income. But what if the fund you pick fails to deliver? Worse still, what if your money is lost?

The idea of regular, consistent payments is a critical part of an income-focused portfolio. Ensuring that a portfolio actually looks and works that way across extended periods can take a bit more planning. It’s not as simple as bunging everything into a bond and taking a monthly coupon.

Technology has made investing easier than ever. Australian investors can now buy shares, compare ETFs, research managed funds, watch market videos, read fund updates and place trades from their mobiles.

Since the 50% capital gains tax (CGT) discount was introduced in Australia in 1999, many investors have followed a relatively consistent wealth-building playbook: purchase residential property, absorb short-term cash flow losses via negative gearing, and rely on long-term capital growth supported by favourable tax treatment.

It’s almost a certainty that you have invested in a multi-asset portfolio or fund at some point in time. Most of us will spend our whole lives in one – your superannuation is run as a multi-asset portfolio after all. But when it comes to investing outside of super, many investors can also find plenty to like about these options as a wealth solution.

-eqdavf9r99ic9fe3htah.png?_a=BAMAAAcg0)

-pxiuel5d343plbjy7hdo.png)

-pjjqi0rs34lxn2sib3go.png)

-4n4hb2pbhnt1l9z5qcb0.png)

-x5zevcitnzrsy2mixx6e.png)

-b4y0oal84e0xcj53yoyy.png)

-qeo43sf8l7viuk3c6oqw.png)