Australian vs Global Bond Funds: Currency Changes Everything

Sara Allen

Thu 26 Feb 2026 8 minutesFollowing the exchange rate might be popular for those planning future international travel, but those planning their portfolios should not forget currency either. A shift in the exchange rate can mean an instant shift in the value or performance of your portfolio, depending on whether you have hedged any of your international exposures.

Currency can also be a source of volatility in the traditionally defensive part of your portfolio, fixed income, and can change your performance expectations. It is something you will need to factor in when planning your fixed income allocations between Australian and global bond funds from a risk and performance perspective.

Just like exchanging one currency for another when travelling, the rate could be favourable or unfavourable when it comes to investing in bonds, which can shift your returns.

Here are the basics to help you plan.

Currency Changes Overall Returns

The exchange rate changes the overall value of your returns when you have investments in another currency, for example, holding US Treasuries or UK Gilts.

Picture it this way.

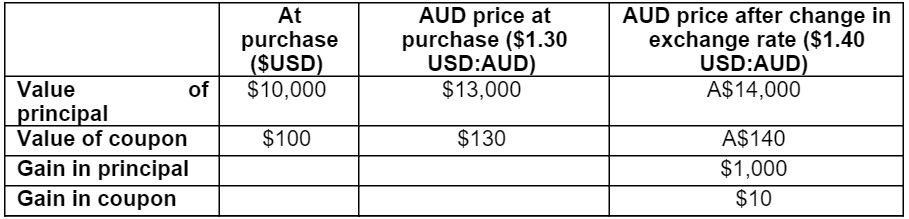

You purchase a bond for US$10,000 and it pays coupons of US$100. If the US dollar strengthens against the Australian dollar, then the value of your investment converted back into Australian dollars is now worth more. You are effectively receiving a higher yield, and the return of your principal at the maturity date is higher than your initial investment converted back into Australian dollars.

Here is an example of what that might look like. To keep it simple, 1 USD buys A$1.30 at the start and then the USD strengthens to A$1.40.

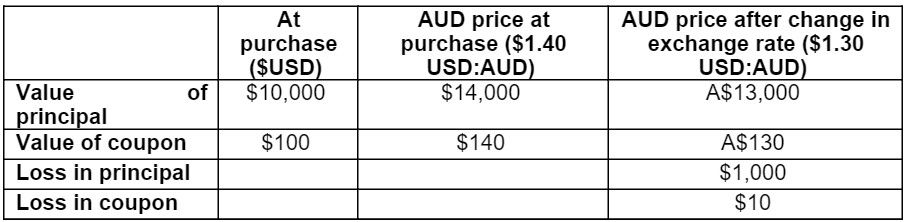

It can work the other way as well, which is why many international fund managers, across all asset classes, often hedge their investments back to the Australian dollar to reduce the risk of loss if the exchange rate depreciates.

Flipping the previous example would look like this.

This is a risk Australian investors do not take on if they simply use Australian bond funds, because they reflect the local macroeconomic environment.

The A$10,000 principal of an Australian bond remains the same amount at the maturity date of the bond, regardless of what the Australian dollar is doing against other currencies. The coupon payments also remain at the amount they were set at.

What fluctuates is the market value and yield of the bond over time based on a range of drivers. However, if you hold the bond until maturity, those fluctuations will not necessarily result in a real loss.

The story does not end as simply as this, though. The relationship between bonds and currency becomes more complex. The good news is that this is where fund managers come in, so the next part is primarily for your understanding.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

The Relationship between Currency, Interest Rates and Bonds

Both bonds and currencies are closely tied to interest rates.

For example, in a rising interest rate environment, the price of an existing bond will fall to allow its yield to align more closely with prevailing market rates. Conversely, in a falling interest rate environment, the price of that same bond will rise so its yield remains in line with market rates.

When it comes to currency, countries with higher interest rates are typically more attractive to investors and, as a result of increased demand, their currencies may appreciate. By contrast, lower interest rates are generally less appealing to investors, which can lead to currency depreciation.

Currency traders often watch interest rates and central bank decisions to form a view on the strength of an economy and how demand for investment may translate into exchange rate movements.

Taking this a step further, government bond yields, such as the 10-year US Treasury yield, are often monitored as a way of forecasting future central bank decisions. Based on these expectations, investors may decide to buy or sell bonds in a particular country.

A very simplified summary would be:

When rates rise, bond prices fall (but yields rise) and foreign investors may find this attractive. Increased demand can push up the value of the currency against others with less attractive interest rates.

When rates fall, bond prices rise (but yields fall) and foreign investors may find this less attractive, so they move their capital elsewhere. The resulting change in capital flows can reduce the value of the currency against others with more appealing interest rates.

There is clearly much more that drives currency, interest rates and bond yields, but the key point is that a relationship exists between them and it can influence performance and volatility across markets.

Using Currency to Enhance Performance

Given that fixed income is typically the defensive component of a portfolio, there can be additional nuance in how and when international bonds are used.

For example, investing in economies that typically have stronger currencies relative to Australia can help buffer against domestic inflationary pressures.

The A$100 coupon you receive from an Australian government bond may not stretch as far when global inflation rises. However, this may be offset by gains in the US dollar, which can benefit from the same inflationary forces and rising interest rates. In that case, the coupon from a US Treasury bond may be worth more in Australian dollar terms.

You can offset the risk that the exchange rate depreciates by diversifying international fixed income exposure across multiple regions. Alternatively, you may choose a hedged fund to reduce the impact of currency movements on investment returns.

When fund managers use hedging, they typically focus on the relationship between currency movements, interest rates and bond yields to manage returns or identify opportunities. This may involve the use of forward contracts or currency options.

It is important to remember that hedging is designed to smooth volatility. As a more complex strategy, it can involve higher fees compared to unhedged approaches. Hedged funds can offer diversification beyond Australian bonds while minimising currency movements. Investors who wish to deliberately incorporate currency risk as part of their strategy may therefore be better suited to an unhedged international bond allocation.

The relationship between bonds, currency and interest rates can also be used by fund managers to pursue additional sources of return.

For example, if bond traders see interest rates rising in one country and anticipate that the currency will follow, they may purchase assets such as bonds in that currency to benefit from the appreciation.

Alternatively, if they anticipate interest rate cuts and a weakening currency, they may sell assets in that economy to avoid potential losses and reallocate capital to more attractive opportunities.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Your Portfolio and Currency Considerations

While investors typically consider a wide range of risks when constructing portfolios, it can be easy to overlook risks within defensive assets, particularly currency risk. Currency movements can have a significant impact on the performance of international bonds, and research suggests exchange rates are one of the key transmission channels for volatility in this asset class.

This does not mean you should avoid international bonds or rely solely on Australian bond funds to reduce risk. It does mean you need to consider how international bonds fit within your portfolio and the extent to which currency exposure is desirable or necessary.

For some investors, currency exposure may be a deliberate strategy to seek higher income, recognising that adverse movements can also occur if foreign currencies depreciate against the Australian dollar.

For those seeking diversification benefits but concerned about currency risk, hedged funds may be preferable, alongside a higher allocation to Australian bonds.

A key takeaway is that fixed interest should not be viewed as a set-and-forget allocation simply because it plays a defensive role. It requires strategy and planning to identify the most appropriate funds and allocations.

As always, speaking with an expert can make a meaningful difference, particularly in the complex world of bond markets.

Currency can influence performance in many ways. Understanding the level of exposure you are willing and able to manage will shape how you use international bonds and balance them with Australian bond allocations. With a wide range of fixed interest investment options available in Australia and ongoing global change, this remains a more dynamic investment area than many investors expect.

Disclaimer: This article is prepared by Sara Allen. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.