Passive Is Winning the Flows — But Active May Be Gaining the Edge

Jarrad Stuart

Thu 26 Feb 2026 5 minutesPassive investing has reshaped global equity markets over the past decade. Record inflows into low-cost ETFs have led many investors to question whether active management still has a meaningful role.

Yet beneath the surface, market structure is evolving in ways that may increasingly favour genuinely skilled, high-conviction active managers.

For independent investors, the key question is no longer active versus passive — but where each approach is most likely to add value.

The Structural Shift Few Investors Are Talking About

Passive investing succeeds because of its simplicity, cost efficiency and broad market exposure. However, the rapid growth of index-linked capital is also influencing how markets behave.

When capital flows are driven primarily by index weights rather than fundamental analysis, several second-order effects tend to emerge:

- increasing concentration in mega-cap stocks

- more price-insensitive buying

- wider valuation dispersion across the market

- declining research coverage in smaller companies

These dynamics do not eliminate inefficiencies — they tend to relocate them, often away from the largest index weights and into less trafficked parts of the market.

In our assessment, some of the most compelling opportunities are emerging in parts of the market that sit well outside the largest index weights.

Concentration Risk Is Quietly Building

One of the defining features of current equity markets is the degree of index concentration.

Today, the largest handful of companies represent an historically elevated share of major global equity indices — levels not seen in decades. In the U.S. market in particular, a small number of mega-cap companies have driven a disproportionate share of recent index returns and index weight.

While this has benefited passive investors during the upswing, it also introduces a less discussed risk: portfolios that appear diversified may in reality be heavily dependent on a narrow leadership group.

History suggests that periods of elevated concentration are often followed by phases where market leadership broadens — environments that have traditionally been more supportive for active stock selection.

For investors, it is worth asking: how diversified is your global equity exposure in practice?

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Where We Continue to See Inefficiencies

Despite the growth of passive investing, several areas of the global equity market remain structurally under-researched and, in our view, more prone to mispricing.

These include:

Under-followed global mid-caps

Many high-quality businesses outside the major indices receive limited sell-side coverage and relatively low passive ownership.

Corporate inflection stories

Companies undergoing strategic, operational or capital allocation change are often slow to be correctly priced by the market.

Businesses with improving unit economics

Markets can lag in recognising durable improvements in underlying profitability.

Periods of elevated dispersion

The dispersion across global equity returns in recent periods has been meaningfully higher than the ultra-low volatility environment of the 2010s — a backdrop that has historically rewarded selective, high-conviction stock pickers.

Importantly, these opportunities tend to sit away from the largest index weights where passive capital is most concentrated.

What Sophisticated Allocators Are Focusing On

Another notable shift is how experienced investors are assessing emerging managers.

While long track records remain valuable, many allocators are placing increasing weight on:

- clarity and repeatability of process

- evidence of downside discipline

- portfolio concentration with risk awareness

- alignment between managers and investors

- consistency of execution

The pressure is increasingly on strategies that resemble the index but charge active fees. In a world of transparent beta and low-cost passive exposure, genuine differentiation matters more than ever.

Managers that can demonstrate disciplined portfolio construction and consistent outcomes — even over shorter periods — are increasingly attracting attention from selective allocators.

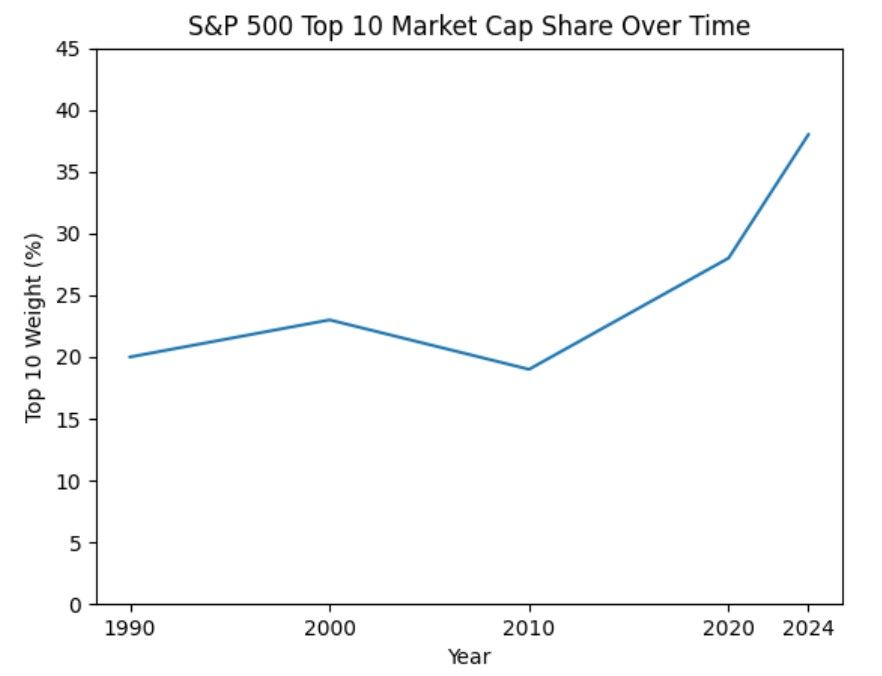

Concentration at Multi-Decade Highs

Recent data shows that the share of the S&P 500 captured by its top 10 stocks has climbed sharply from roughly 19 % in 2010 to around 38 %-40 % by early 2025 — among the highest levels observed in more than a century.

Today, a handful of mega-cap names — including Nvidia, Apple, Microsoft and Amazon — account for roughly 40% of the index’s market capitalisation, exposing broad passive investors to concentrated drivers of performance.

Even more extreme concentration is evident in growth-focused benchmarks, where the top ten companies can comprise over 60% of total index weight.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

The Outlook: A Barbell Market

Passive investing is unlikely to reverse its structural growth. Low-cost beta exposure has earned a permanent place in portfolios.

However, the industry increasingly appears to be moving toward a barbell structure:

- ultra-low-cost passive at one end

- highly differentiated, high-conviction active at the other

- continued pressure on benchmark-aware strategies in the middle

For investors, the opportunity may lie in combining both approaches thoughtfully rather than viewing them as mutually exclusive.

Final Thoughts

The narrative that passive investing has made active management obsolete is overly simplistic.

In reality, the very forces driving passive growth — concentration, price-insensitive flows and widening dispersion — may be creating a more favourable environment for disciplined, high-conviction global equity managers than many appreciate.

In our experience managing a concentrated, benchmark-agnostic global equities strategy — including a strong inaugural year — the current environment has reinforced the value of disciplined stock selection and downside risk control.

For investors reviewing their global equity exposure, it may be prudent to reassess where true diversification and active edge can still be found.

Disclaimer: This article is prepared by Jarrad Stuart. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Jarrad Stuart is Managing Director and Portfolio Manager at Sharpbridge Funds Management, specialising in global equities with a focus on high-conviction, benchmark-agnostic investing. His investment approach emphasises disciplined portfolio construction, downside risk management and identifying under-researched global opportunities.