We Road Test ChatGPT’s Financial Planning Capabilities

Simon Turner

Mon 2 Mar 2026 8 minutesOne of the great emerging benefits of AI is that it allows self-directed investors to take better control of their financial destinies. With its fast-improving capabilities, valuable financial advice may be available at your fingertips. Or so the theory goes.

We decided to road test ChatGPT’s financial planning capabilities for a guide as to how valuable they are for investors at this juncture.

The Test Subject: Maxine Schubert

Meet Maxine Schubert. She’s a 53-year-old Brisbane-based accountancy business owner, earning $150k+ most years. She has a high tolerance for risk, a strong belief in global equities, and plans to retire at 60. She’s a single parent to a 15-year-old son and wants both growth and certainty as her retirement approaches.

Maxine’s Current Financial Position

- $1.0m in her principal residence in Brisbane, which is debt-free.

- $400k in her superannuation fund.

- $400k in her personal share portfolio which has been consistently underperforming.

- $200k in her cash management account

Maxine’s trigger for taking financial action was seeing a close friend face financial devastation after a divorce. Her lesson was clear: confidence in the future is not a plan.

Maxine’s Core Objective

Maxine’s goal is to maximise her net worth over the next 7 years without taking risks that could compromise her retirement security or family stability. She wants to keep her home while optimising her $1.0m of investable assets.

ChatGPT’s Advice for Maxine Analysed

So we asked ChatGPT to put together a customised financial plan for Maxine.

Here are its responses and our analysis of its responses…

The Plan

Maxine does not need clever ideas. She needs structure, diversification, and time in the market. By replacing underperformance with a disciplined global ETF approach, and by steadily reducing risk as retirement nears, she can pursue strong growth while protecting the life she has built for herself and her son.

Our take on ChatGPT’s take:

It’s simple but it’s strong. ChatGPT has highlighted exactly what Maxine needs to change in her financial set-up, and it has communicated it clearly.

Plan Score: 10/10.

Step 1: Fix What Is Broken First

Maxine’s consistently underperforming share portfolio is the biggest drag on wealth growth. The issue is not markets, it is process.

Action:

Gradually exit most individual shares over several months to manage tax and timing risk.

Retain a small satellite allocation (no more than 5–10%) if she enjoys stock picking.

Replace complexity with a rules-based ETF investment plan.

Cash should also be split between 6–12 months of essential living and business costs, which is kept untouched, and the remaining surplus to be deployed progressively into investments.

Our take on ChatGPT’s take:

ChatGPT has correctly highlighted the biggest issue which is that Maxine’s stock portfolio keeps underperforming. She’s a busy professional so the fundamental issue here is the amount of time she has to manage it effectively. ChatGPT’s suggestion of maintaining a small stock portfolio is slightly at odds with Maxine’s personal profile, although it’s qualified with an ‘if she enjoys stock picking’.

ChatGPT’s recommendation of simplifying her equity exposure into an ETF structure is prudent, while maintaining a cash buffer is also solid financial planning.

Step 1 Score: 8/10.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Step 2: Build a Simple, Global ETF Portfolio (growth with discipline)

Given her high risk tolerance but short runway (7 years), a sensible starting mix is ‘growth with airbags’: roughly 75% growth assets, 25% defensive. She can implement this using ETFs.

The structure below reflects high risk tolerance, but acknowledges that retirement is only 7 years away.

Target allocation (excluding the family home):

Growth assets: ~75%

ETF plan:

20% Australian equities (Home-market exposure, dividends, franking benefits in taxable structures) – e.g. iShares Core S&P/ASX 200 ETF (IOZ).

45% Global developed equities (Main growth engine, broad global diversification) – e.g. Vanguard MSCI International Shares ETF (VGS).

10% Emerging markets (Higher-growth tilt, higher volatility) – e.g. Fidelity Global Emerging Markets ETF (FEMX).

5% Global small caps (Diversifies away from mega caps, long-run return potential) – e.g. Vanguard MSCI International Small Companies ETF (VISM).

Defensive assets: ~25%

15% Global Fixed Interest (Shock absorber, dry powder for rebalancing during equity drawdowns) – e.g. Vanguard International Fixed Interest Index ETF (VIF).

5% Australian Corporate Bonds (Adds more predictable maturity profile and income focus) – e.g. Betashares 2029 Fixed Term Corporate Bond ETF (29BB).

Our take on ChatGPT’s take:

On balance, ChatGPT’s proposed 75% growth / 25% defensive split aligns with Maxine’s goals and risk tolerance. That’s a solid starting point and an effective interpretation of Maxine’s personal story.

ChatGPT’s proposed plan is well-diversified by region and industry, and is focused on low-cost ETFs rather than managed funds. This is a good match for Maxine given her stock portfolio has long underperformed: i.e. her tolerance for an underperforming managed fund is likely to be low.

However, ChatGPT’s plan lacks exposure to thematic managed funds targeting themes such as technology, real assets (including gold), and property. Arguably, a growth-focused portfolio should include some thematic exposure (say 10%), and managed funds often have the edge over ETFs in these specialised sectors. So that’s arguably a weakness in the ChatGPT plan.

Step 2 Score: 8/10.

Step 3: Use Superannuation Aggressively but Intelligently

Maxine earns at least $150k most years, so super is her best tax lever if cash flow allows.

Action:

Maximise concessional contributions each year (currently $30,000 including employer amounts).

Check eligibility for carry-forward concessional contributions, as her balance is under $500k.

Invest super using a similar growth-oriented ETF mix, gradually reducing risk as age 60 approaches.

The goal is to enter retirement with super structured so she is not forced to sell growth assets in a market downturn.

Our take on ChatGPT’s take:

ChatGPT’s advice is spot on here. Maxine’s optimal strategy is to maximise her super contributions in growth-oriented ETFs that align with her personal goals.

Step 3 Score: 10/10.

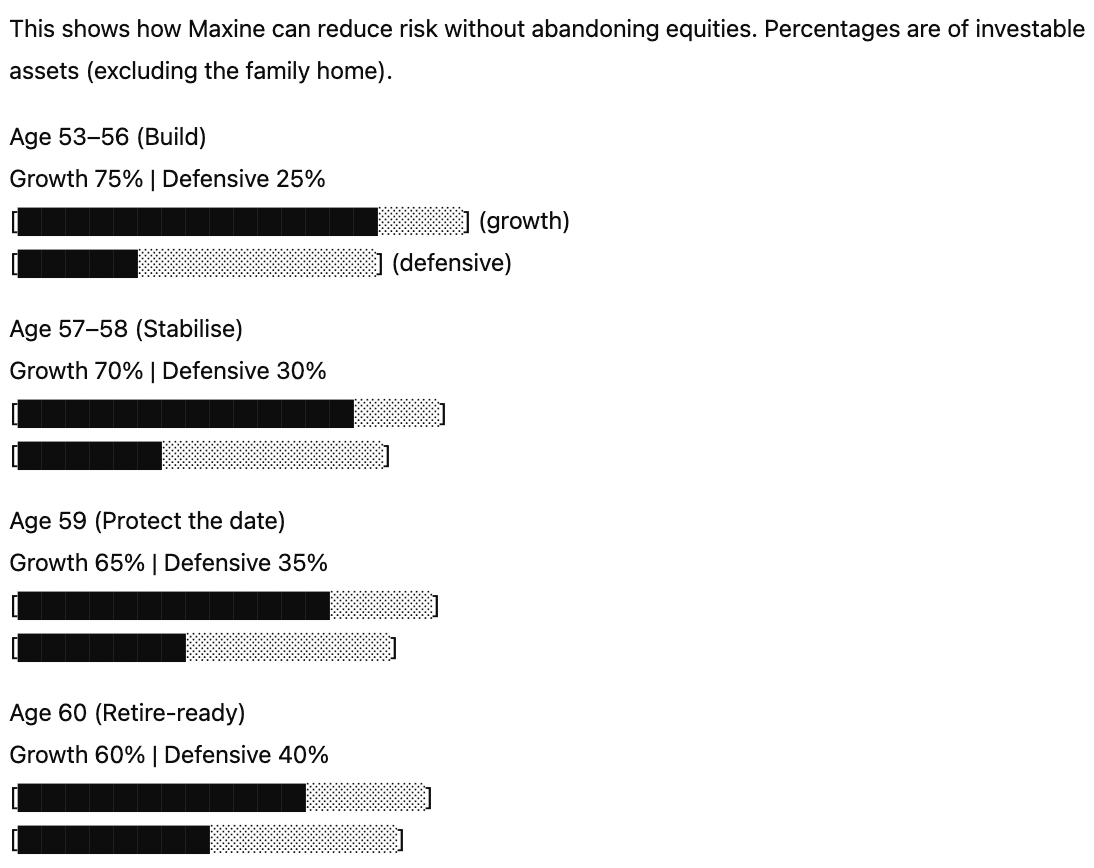

Step 4: The Retirement Glide Path (how risk reduces without panic)

Maxine’s risk should fall gradually, not suddenly.

This plan protects Maxine’s retirement date while keeping her long-term capital working.

Our take on ChatGPT’s take:

ChatGPT’s advice here should be taken with a grain of salt. It’s debatable whether a retirement-ready portfolio should be 60% invested in growth assets. By the age of 60, Maxine’s tolerance for risk is likely to have significantly fallen, not just because she’ll be older, but because she’ll be dependent on her investment portfolio by then. A more prudent split may be along the lines of 40% growth/60% defensive.

However, ChatGPT’s recommendation of incorporating a retirement glide path into her plan is a good one. It should be core to all long-term investment plans.

Step 4 Score: 6/10.

Step 5: Don’t Ignore Concentration Risk

Maxine’s $1m Brisbane home is a single-asset, single-city exposure. That is fine for lifestyle reasons, but it means her investment portfolio must provide diversification. Global equities and bonds do that job.

Downsizing or equity release can remain optional future levers, not assumptions baked into the plan.

Our take on ChatGPT’s take:

ChatGPT makes useful points here. Maxine’s property represents half her net worth, so her plan needs to be holistic and provide diversification into different assets with different drivers.

Step 5 Score: 10/10.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Annual Checklist

Each financial year Maxine should:

Maximise concessional super contributions.

Rebalance back to her target allocations.

Review insurance, will, and guardianship arrangements.

Stress test her plan against the risk of a 12-month income disruption.

Our take on ChatGPT’s take:

This is a solid annual checklist.

We would also add reinvestment of dividends and cash levels above her emergency buffer to ensure Maxine benefits to the full extent from compounding over the long-term.

Checklist Score: 8/10.

The Down Low on ChatGPT’s Financial Planning Capabilities

Overall, ChatGPT provided a solid financial plan (8.6/10 on average) for Maxine which is streets ahead of her current financial set-up. Whilst it isn’t perfect (like most human advice), and at times is slightly inconsistent, it nails all the core financial planning fundamentals, providing a simple, easy-to-understand plan tailored to each particular investor.

For most self-directed investors, this is now a financial planning tool worthy of consideration. Just remember: AI will always depend on the quality of the inputs you provide it. It remains important to trust, then verify.

Funds Mentioned

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.