Once upon a time, income investors might simply have used a select group of dividend-paying equities and bonds to cover their needs. Today’s income portfolio looks vastly different – though equities and bonds still play a role.

Investors learnt the hard way long ago.

In the years post the GFC, globally low rates made it challenging to generate sufficient income from bonds or savings accounts, pushing investors into riskier assets like equities. But that, in itself, raised challenges, leaving investors dependent on the ebbs and flows of market activity and not guaranteed that dividends would remain consistent.

Then rates rose with inflation, and investors were forced to broaden their horizons to keep up with the cost of living. The end result was that income portfolios needed just as much diversification as growth-oriented portfolios but faced different challenges in construction.

The biggest challenge of building a reliable income portfolio?

Planning for income today and ensuring the foundations for income in the future that meets your ongoing needs within the market environment.

As Josef Jindra, Senior Financial Adviser for Viridian Advisory, says, “the objective of building an income portfolio is not to remove volatility altogether, but to ensure the portfolio has both income stability today and the capacity for income growth tomorrow.”

What this all means is that you might, broadly speaking, be invested across the same asset classes as in a more growth-oriented portfolio, but your approach to the investments within those asset classes might be a bit more nuanced.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Meeting a Reliable Objective

Investors planning for income portfolios can fall into the trap of simply seeking high yield. Jindra suggests they need to redefine this and start with what purpose they specifically need income for, be it living expenses in retirement, or supplementing existing employment income.

“From there, the most important considerations are income reliability, capital preservation, liquidity, diversification, tax efficiency, and the ability of that income stream to keep pace with inflation over time,” Jindra says.

He notes that high-yield is not always the same as sustainable, long-term income so factors like asset quality, earnings durability, and disciplined portfolio construction need to come into play.

Working with a financial adviser may help you define what level of income you need your portfolio to generate – and this will influence the types of assets you might need in your portfolio, what level of risk your portfolio can sustain while still offering the returns you might need and mapping out future growth to offset inflation.

Think of reliable as being:

- Consistent payments

- Resilient in the face of market volatility

- A growth buffer

This is partly why government bonds have been so popular with income investors over time – guaranteed return of principal at the maturity date and set coupons paid at regular intervals.

Similarly, franked dividend paying equities in Australia have been popular because of the ability to supplement income further through franking credits, as well as receive a regular dividend. Jindra lists Aussie favourites like Telstra (ASX: TLS), Transurban (ASX: TCL) and APA Group (ASX: APA) as examples of defensive players in this space.

Setting Asset Allocations in an Income Portfolio

Jindra views income portfolios as a delicate balance of yield and longer-term growth and stability.

“The balance typically comes from combining stabilising assets such as cash, term deposits and high-quality fixed income, with growth-oriented income assets, such as quality Australian equities, infrastructure and selective listed property,” he says.

He adds that the portfolio shouldn’t be dependent on any one sector, one company or any one rate regime and should have diversified sources of income.

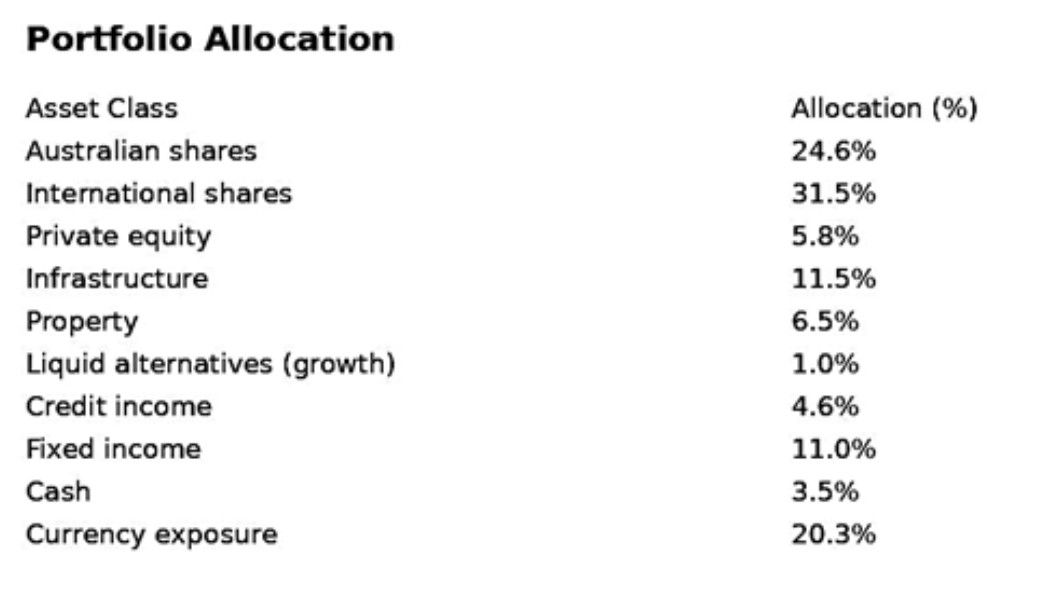

There’s no one-size-fits-all when it comes to investing, but if you are looking for a general model, this is the asset allocation used in the Aware Super Retirement Income Balanced Portfolio to give you an idea of how diversified such a portfolio can look.

Source: Aware Super, 31 March 2026

Each of these asset classes has different benefits for an income portfolio.

- Equities: can offer income through dividends and the potential of growth in value if the share price appreciates.

- Private equity: Diversification away from public markets and the potential for higher returns. Private equity can also be less volatile compared to public markets.

- Infrastructure: Typically offers regular stable and predictable cash flows and is often defensive during inflationary periods. For example, toll road operators are typically able to pass through inflation in their tolls.

- Property: Rental yield offers a regular source of income that typically adjusts with inflation. Quality assets can also offer capital protection and some level of growth.

- Liquid growth alternatives: These are non-traditional strategies like long/short equity, managed futures and macro trading which perform differently to other asset classes and can be protective or offer growth in periods of volatility. They can be associated with higher risk so investors should consider how they fit in the portfolio as a whole.

- Credit income: Private credit and other forms of credit can offer regular income, sometimes at higher levels compared to traditional fixed income. They often use floating rates which can be protective in periods of inflation and rising rates.

- Fixed income: Regular coupon payments and the return of your principal at maturity. However, in periods of rising rates and inflation, you may find relying on this a challenge as the coupons are fixed.

- Cash: This is valuable for liquidity for expenses or to add to your portfolio and you can also generate interest off cash balances to support your income needs.

- Currency exposure: This is a buffer for volatility and can also offer growth when exchange rates between Australia and other countries adjust.

Investors should remember there are a range of ways to find exposure to each asset class, be it direct investment, managed funds and listed investments.

ETFs are an increasingly popular option for investors to use within their portfolio for exposure. Jindra finds the options like Vanguard Australian Shares High Yield ETF (ASX: VHY), iShares Core Composite Bond ETF (ASX: IAF) and Vanguard Australian Fixed Interest ETF (ASX: VAF) can be effective core holdings in an income portfolio.

For those specifically looking at regular income in their equities exposure, he finds Betashares Australian Dividend Harvester Active ETF (ASX: HVST) a good targeted option for franked income with monthly distributions.

Active Management for Market Conditions

While your overarching strategy should be forward-thinking and long-term, active management means considering tilts to take advantage of market conditions. This is true regardless of whether your portfolio is focused on income or growth.

When it comes to an income-focus, you should be aware of inflation and the rates environment as part of your approach.

Jindra suggests an emphasis on shorter-duration fixed income, floating rate credit where appropriate and companies with strong pricing power and resilient balance sheets in a rising rate and inflationary environment.

Some examples of fixed income exposures he has used with investors include Vanguard Australian Fixed Interest ETF (ASX: VAF) and iShares Core Composite Bond ETF (ASX: IAF) .

He notes that infrastructure and real asset exposures can be valuable, due to defensive cash flow profiles and long-dated infrastructure assets.

By contrast, a falling rate environment might see a better emphasis on longer-duration bonds and rate-sensitive assets.

“Equally, high quality equities and listed infrastructure can become more supportive contributors to both income and total return,” Jindra says.

Thinking Long-Term for your Income

Building an income portfolio in today’s world should be strategic and forward-looking.

It’s not about picking the highest-yielding options today but mapping out a whole portfolio of diversified income sources which will offer you stability and longer term growth. After all, you can always rely on inflation to erode your income so you need to plan for how your portfolio income can step up to meet market conditions and your ongoing needs.

To quote Jindra, “good income investing is not about stretching for yield. It is about building a portfolio that can deliver cash flow, preserve capital sensibly, and remain durable across market cycles.”

Think about sustainability, quality, and diversification alongside your goals and objectives.

Funds Mentioned

Vanguard Australian Fixed Interest Index ETF seeks to track the return of the Bloomberg AusBond Composite 0+ Yr Index before taking into account fees, expenses and tax.

Retail Investor

The fund aims to provide investors with the performance of the Bloomberg AusBond Composite 0+ Yr IndexSM, before fees and expenses. The index is designed to measure the performance of the Australian bond market and includes investment grade fixed income securities issued by the Australian Treasury, Australian semi-government entities, supranational and sovereign entities and corporate entities

Retail Investor

Opportunity for high income from Australian shares

Retail Investor

Availability

Open for investment

Disclaimer: This article is prepared by Sara Allen. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

-imbv0jwtgfkpzmj55uvm.png)

-7mc6hsayqab3oggarjw2.png)

-pxiuel5d343plbjy7hdo.png)

-4yb643awg03namrcahu4.png)

-zrxpxihmn0inisejx8wx.png)

-vke5r81en85n0lawxvqo.png)