The Shifting World Order & What it Means for Investors

Simon Turner

Wed 11 Mar 2026 7 minutesFor the longest time global investment markets been defined by the implicit assumption that globalisation, relative geopolitical stability and expanding trade would continue indefinitely. However, that assumption is being tested.

The U.S.-Israel attack on Iran is one of many signals that the world order underpinning markets for three decades is evolving into something less predictable and more fragmented. The implications for investors are significant.

Bigger Issues at Play

Markets reacted immediately to the news of the U.S.-Israel attack on Iran. Oil prices surged amid fears of wider Middle East escalation and possible disruption to the Strait of Hormuz, through which more than one fifth of global oil supply passes. Analysts warned prices could move north of $US100 per barrel depending on the escalation dynamics, illustrating how quickly geopolitical risk is repriced in exposed financial assets.

The bigger implication for investors is the structural change that’s occurring behind all this geopolitical noise.

The global system that delivered disinflation, abundant energy supply and synchronised economic growth is giving way to a multipolar world characterised by strategic rivalry, resource security and political fragmentation.

To be fair, this has been a while in the making. Markets have had a lot of warning signals to digest since the beginning of Trump 2.0, and until recently chose to ignore them. The consensus was that geopolitical shocks are just temporary noise rather than enduring return drivers. Maybe it was recency bias that dissuaded investors from putting too much weight on geopolitical developments.

On that note, we’ve been arguing for some time that markets have been under-pricing geopolitical risk, and oil for that matter. Unfortunately, high and rising geopolitical risk is no longer a benign market backdrop that everyone knows about but few worry about. It’s a very real part of the 2026 investment landscape.

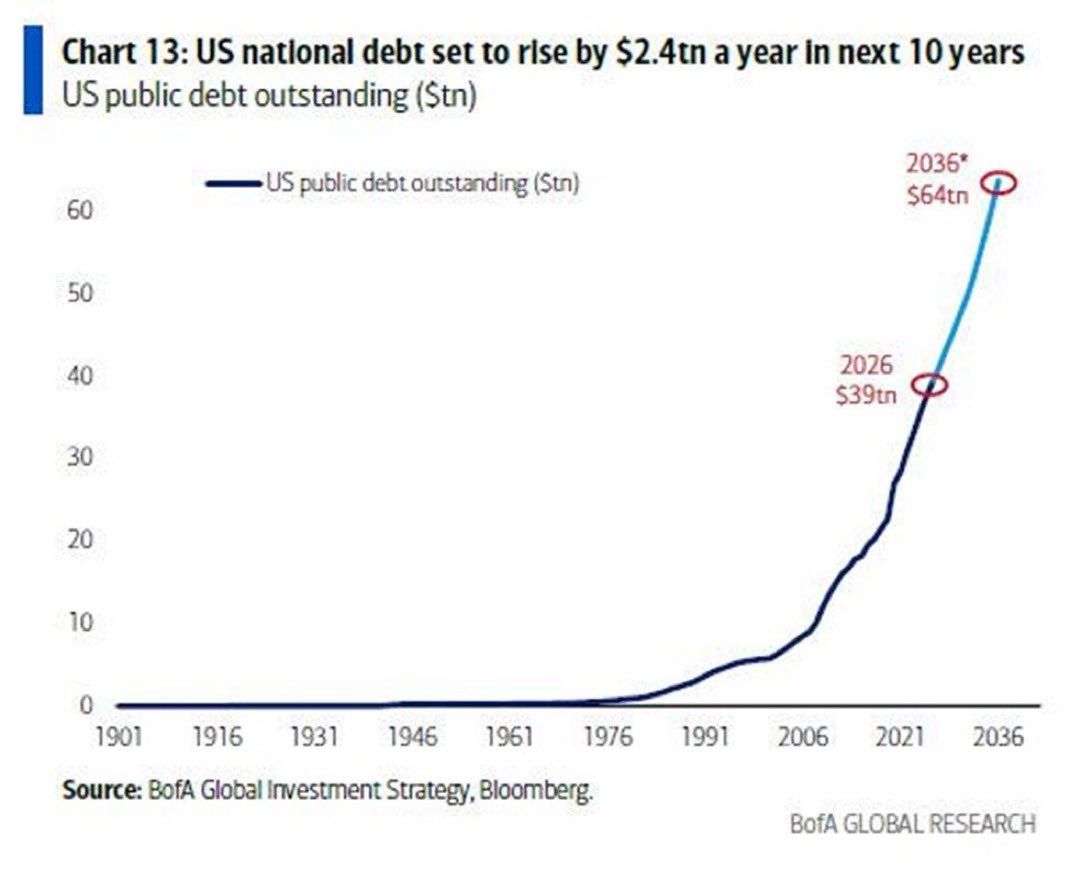

Beyond the sad but inevitable loss of human life, arguably the biggest fundamental issue posed by geopolitical eruptions like this is the impact on U.S. public debt. It was already trending toward dangerous levels prior to this event, as shown below.

A prolonged war could make this situation catastrophic for the U.S. Wars have been the primary historical driver of spikes in U.S. public debt, financed mainly through loans, taxes, and currency issuance, which generates higher inflation and prolonged costs in operations, equipment, veteran care, and interest.

For example, World War I raised U.S. Debt from $US1 billion to $US25 billion; World War II cost $US4 trillion adjusted, pushing debt to 106% of GDP in 1946; the Vietnam War (1955-1975) cost $US2.27 trillion adjusted. The list goes on.

Combining operational and reconstruction expenses, it has been estimated that each day of war with Iran is costing the U.S. $US1.8-2.4 billion. If the situation escalates, it could be much higher and could cost hundreds of billions in total.

This is not an unrealistic scenario. This war may not be short or cheap wars given Iran’s population of 90 million people and military strengths. Worse, it could drag in the entire Middle East region.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

Rising Energy Supply Risk

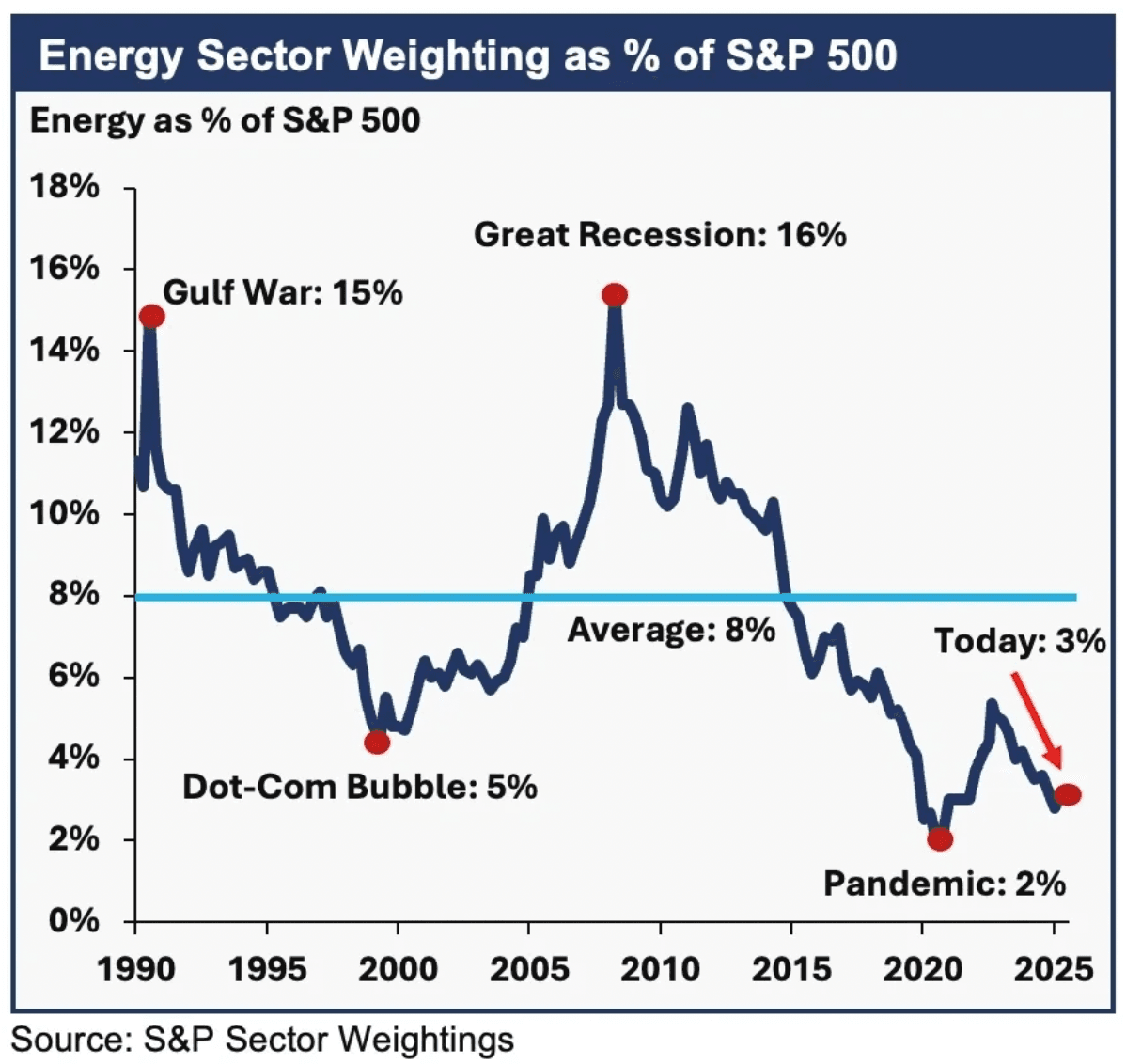

The energy sector tends to be the canary in the coalmine when it comes to geopolitical risks turning real.

Now is a case in point. Years of underinvestment in new oil supply have left the sector fragile precisely when geopolitical tensions are escalating and supply is at serious risk of disruption.

Even before the Iran escalation, analysts estimated a geopolitical risk premium of between $US4 and $US10 per barrel was embedded within oil prices, reflecting persistent geopolitical uncertainty rather than physical shortages.

What matters right now for investors isn’t whether supply is immediately disrupted by the way, which is a very real risk, but that energy has re-emerged as a strategic asset rather than a declining legacy sector.

This represents a profound reversal of the post-2008 investment consensus. For much of the past decade, capital flowed overwhelmingly towards technology, duration assets and low inflation beneficiaries. The energy sector has been largely ignored which is why it is so vulnerable to shocks right now. At only 3% of the S&P 500, the sector could run long and hard from here.

Energy exposure was often treated as optional or even undesirable within ESG-oriented portfolios. However, the new world order suggests energy security, defence capability and supply chain redundancy are likely to once again become structural return drivers that investors should be aware of.

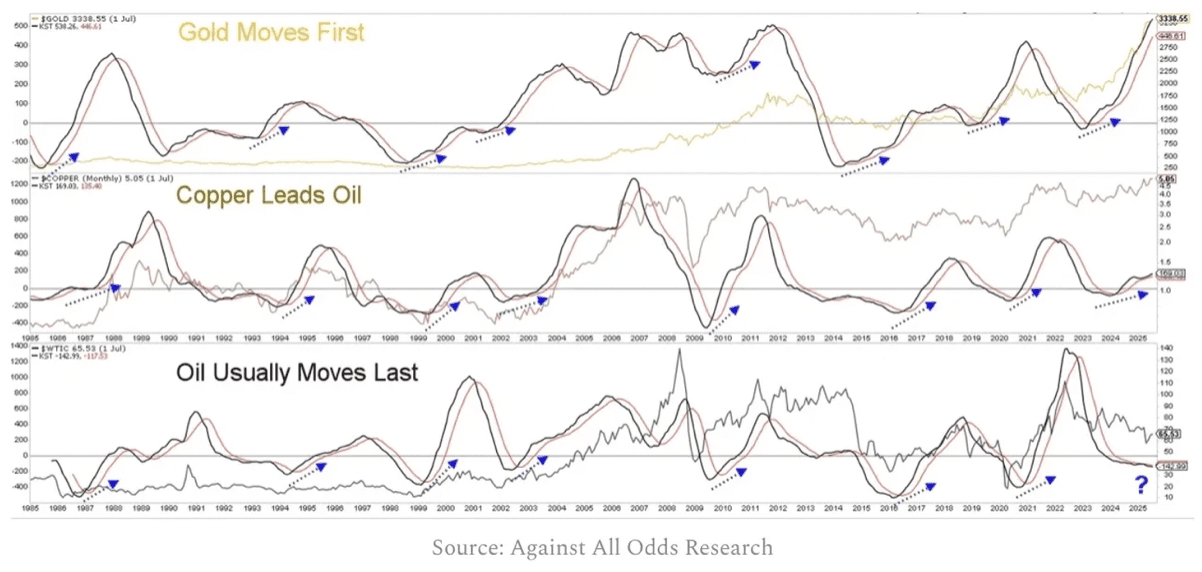

Even without a war to add to the supply risks, it’s well-known that oil tends to follow gold and copper higher.

The Reallocation Effect

These shifts are reshaping both the risks and opportunities available to investors.

The Middle East conflict has already been priced as a primary market risk. If this conflict lasts for months rather than days, the market implications could have much further to run.

In particular, it’s likely to prompt rising reallocations towards energy, commodities, defence industries and inflation hedges.

Such rotations reflect a recognition that geopolitical fragmentation changes the opportunity set rather than merely increasing volatility.

For Australian investors, the implications are unusually significant.

Australia sits at the intersection of commodity supply, Asian demand and Western security alliances. As global blocs harden, countries rich in resources and political stability, like Australia, are likely to gain strategic relevance.

Energy exposure arguably deserves greater consideration for investors who are underweight the sector. Funds such as the BetaShares Global Energy Companies ETF (ASX: FUEL) provide diversified exposure to oil producers benefiting from structurally higher geopolitical risk premiums.

Similarly, sustainability-focused strategies including the BetaShares Global Sustainability Leaders ETF and transition-oriented clean energy funds such as the VanEck Global Clean Energy ETF allow investors to participate in the energy transition, which is accelerating precisely because energy security has become a higher priority geopolitical policy.

These allocations acknowledge that the future energy system is likely to be additive rather than substitutive, with renewables and nuclear expanding while oil and gas continue to play an important baseline supply role.

Defence and security themes are also becoming more structurally relevant in a fragmented world. Rising military expenditure across NATO and Asia reflects what economists describe as a ‘security premium’ embedded within fiscal policy. ETFs such as the BetaShares Global Defence ETF and VanEck Global Defence ETF provide exposure to companies positioned to benefit from rising defence spending.

Gold and defensive assets have historically benefited during such periods care of rising investor demand as tensions escalate. ETFs such as VanEck Gold Bullion ETF provide exposure to this normally defensive sector.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Diversification Now Needs to Cover Multiple Outlook Scenarios

Beyond sector allocation, the shifting world order challenges traditional portfolio construction itself.

Global diversification once relied on historical correlations declining during stress events. However, increasingly, geopolitical shocks are affecting all asset classes simultaneously through energy price shocks, rising inflation expectations and volatile currency movements.

Supply chains are regionalising, industrial policy is expanding and governments are prioritising resilience over efficiency.

The key takeaway for investors is that the underlying trend towards rising geopolitical fragmentation appears to be here to stay. So portfolios built solely for the low-rate, low-conflict world of the 2010s may struggle to adapt.

Investors should arguably be positioning their portfolios for a new world order characterised by higher inflation volatility, rising resource competition, and a growing market awareness of the strategic value of assets.

Psychological Impacts to Remain

The U.S. strike on Iran may prove be contained sooner rather than later. Or it may run for weeks or months. Who knows. Yet even contained conflicts leave lasting marks on capital allocation decisions. Each episode reinforces a market psychology that increasingly values security, scarcity and sovereignty more highly than before.

For investors, the opportunity lies in recognising that markets are transitioning from an age of optimisation to one of resilience. Those who adapt early may find that volatility is the mechanism through which the next era’s long-term winners emerges.

Funds Mentioned

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.