Why Using Your $30,000 Concessional Super Cap Each Year Could Be One of the Best Investment Decisions You’ll Ever Make

Simon Turner

Wed 25 Mar 2026 6 minutesAustralia’s superannuation system is regarded as one of the most effective retirement savings structures in the world. Yet many investors are underutilising one of its most valuable features: the concessional contributions cap. For the 2025–26 financial year, Australians can contribute up to $30,000 of their pre-tax income into superannuation each year through employer contributions, salary sacrifice, or personal deductible contributions.

If you can afford it, consistently utilising as much of this annual cap as possible can deliver powerful long-term benefits through tax efficiency, compounding returns, and disciplined savings. This simple strategy is likely to significantly enhance your retirement outcomes.

The Tax Advantage is Immediate and Substantial

The most obvious benefit of concessional contributions is their tax efficiency.

Contributions made from pre-tax income are taxed at just 15% when they enter a super fund, which is substantially lower than most investors’ marginal income tax rate.

This benefit is particularly powerful for higher earners. For investors in the 47% tax bracket, contributing income into super instead of taking it as salary effectively reduces the tax paid on those funds by 32%.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

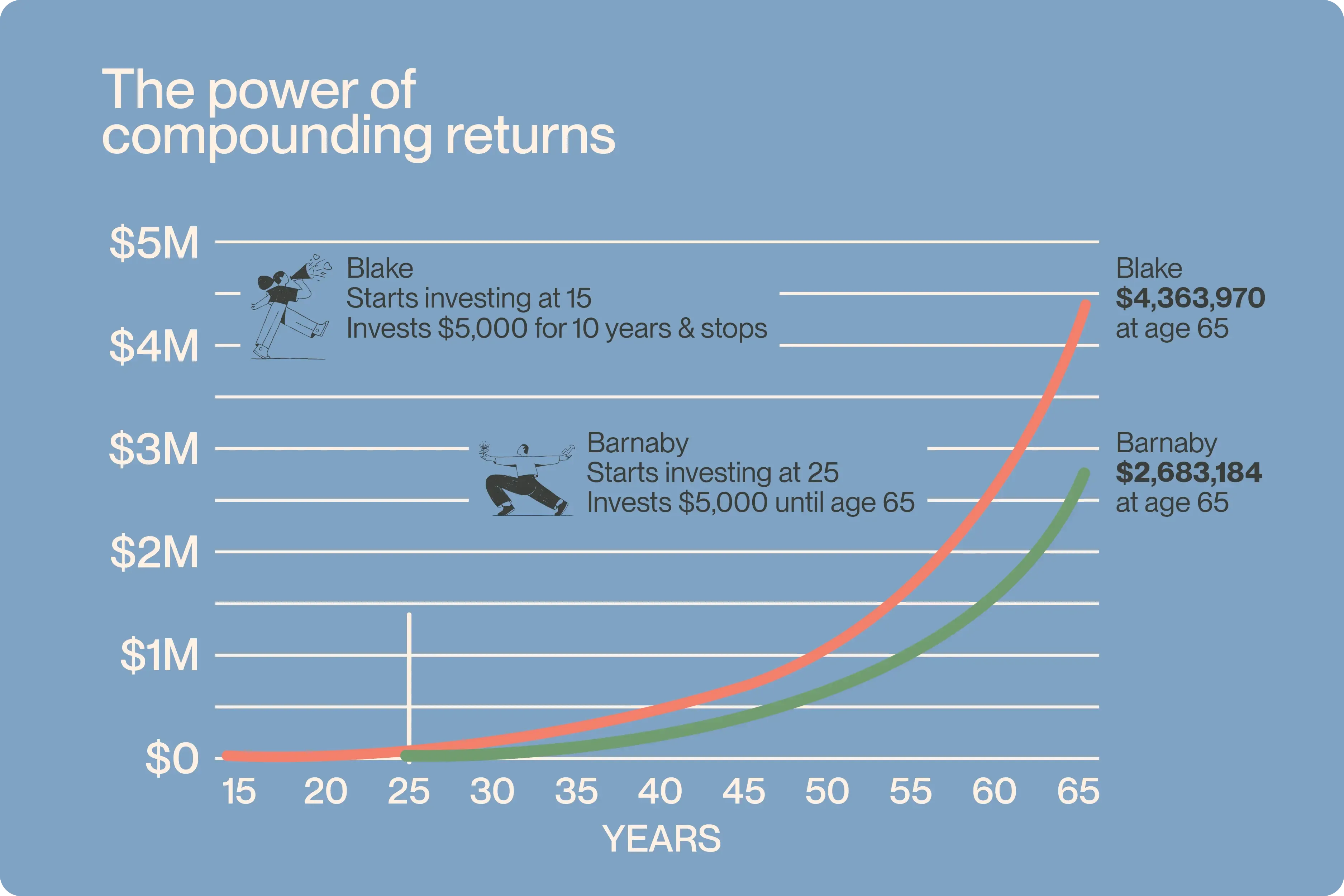

Compounding Amplifies the Long-term Benefit

A contribution strategy that consistently utilises the $30,000 concessional contributions limit each year benefits from three forces simultaneously:

- The reduced tax on the contributions,

- Lower tax on investment earnings within super, and

- The reinvestment of higher retained returns over long periods.

Time is your friend in this process, so start as soon as possible. Additional contributions made earlier in an investor’s career have more time to compound and therefore produce disproportionately larger retirement balances.

This time horizon benefit is particularly powerful when contributions are invested in growth assets such as global funds and ETFs.

A Valuable but Limited Annual Opportunity

Time is also of the essence from an ATO perspective when it comes to utilising the annual concessional cap.

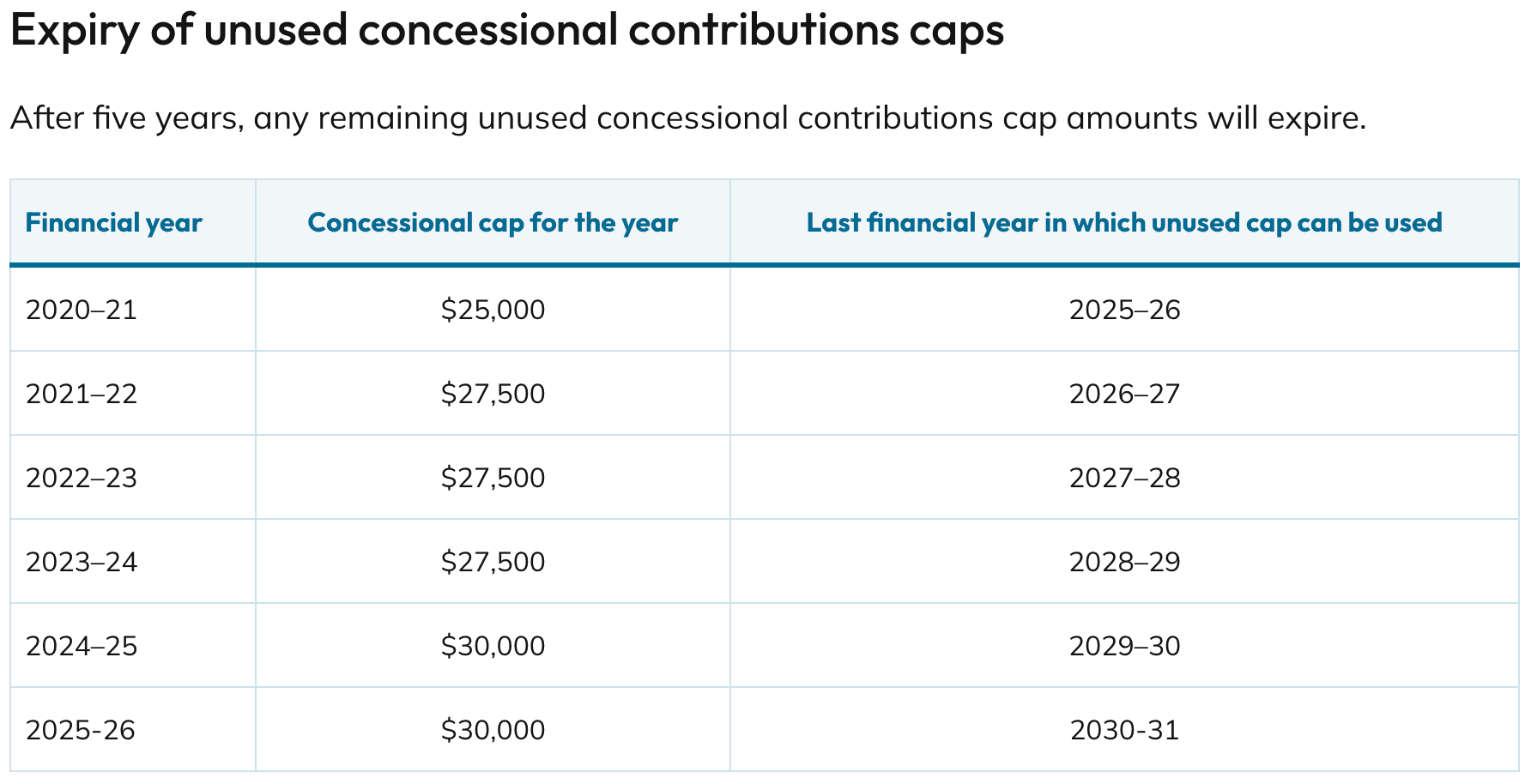

If investors do not use their available cap in a given year, they may permanently lose that tax-advantaged contribution space.

The current concessional contributions cap is $30,000 p.a. This includes employer Superannuation Guarantee contributions, salary sacrifice arrangements, and personal deductible contributions.

Unused cap amounts can be carried forward for up to five years if an investor’s total super balance is below $500,000. This allows investors to make catch-up contributions after periods of lower savings.

Tip: You can find how much you have in unused cap contributions by logging into myGov, entering the Tax section, and clicking on Super. The data there is up to date as of your last tax return.

You do not need to fill in any forms or notify your super fund (or anyone else) when utilising carry-forward contributions. Simply make your concessional contributions in the usual way via salary sacrifice or personal tax-deductible contributions. Your fund will report your concessional contributions to the ATO, which will automatically carry forward unused cap amounts from prior years (if you are eligible). The oldest unused cap is used first. When it has been used up, the following year’s unused cap will be drawn upon, and so on.

While catching up makes perfect sense for investors with unused concessional contributions, as a strategy it is not a substitute for consistent annual contributions, which serve as an enforced means of dollar cost averaging in a global market that generally rises over the long term.

Hence, the best and simplest way to maximise the benefits of the cap is to use it annually. By investing up to $30,000 of your annual income into your super, you are taking an important step towards financial freedom in retirement.

A Structurally Efficient Investment Vehicle

Beyond contribution tax advantages, superannuation enjoys other structural benefits that enhance investors’ long-term returns.

For example, investment earnings within super funds are generally taxed at a maximum rate of 15% during the accumulation phase, which is substantially lower than the tax rate applied to most investments held outside super.

Moreover, in retirement phase accounts, earnings generally become tax free.

Lower ongoing tax on dividends and capital gains allows a larger proportion of investment returns to remain invested and continue compounding over the long term.

This is why allocating additional capital into super is generally more tax efficient than holding the same assets outside of super.

It also explains why utilising the $30,000 annual contributions cap (and any unused contribution caps over the preceding five years) is a rare no-brainer strategy for almost all investors.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Behavioural Benefits Also On Offer

An overlooked advantage of this strategy is the behavioural discipline it demands of investors.

Salary sacrifice contributions serve to automate savings by diverting income into super before it reaches investors’ bank accounts.

It has long been recognised that automated saving and investing is arguably the one habit which builds wealth faster than any other.

By removing the need to think about whether to invest or spend, this strategy increases long-term saving rates. It is a highly effective habit that leads to enhanced wealth accumulation.

Slow and Steady Wins the Race

The concessional contributions cap represents one of the most powerful wealth-building mechanisms available to Australian investors.

Investors should begin by determining how much of their annual $30,000 cap is already used by employer Superannuation Guarantee contributions or personal contributions. The remaining capacity (and any unused caps from the last five years, if your super balance is under $500,000) can potentially be filled through salary sacrifice or personal deductible contributions.

Investors should also ensure that their contributions are invested appropriately within their super fund. Diversified exposure to high-quality global equity funds and ETFs is generally a solid means of maximising long-term growth potential within this tax-efficient super structure. But, of course, everyone’s investment goals are unique.

Arguably, the most important takeaway is that consistent contributions matter more than occasional large contributions. Regularly utilising as much of your concessional cap as you can afford could transform your retirement outcomes over decades.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.