What Do Higher Oil Prices Mean for Markets?

Investors have long watched oil prices as a gauge of global inflation, corporate profitability, geopolitical risk, and consumer spending. When it moves sharply in one direction, it’s arguably one of the most heeded signals in the market. When it spikes, the news headlines often predict equity market turmoil. When it collapses, they are more focused on the likelihood of a global recession.

Yet the historical relationship between oil prices and stock market returns is more nuanced than many investors assume. The evidence suggests that higher oil prices do influence equities, but the magnitude, duration, and direction of that impact depend heavily on the underlying cause of the price rise.

A Tax on the Global Economy

It’s well-understood that when energy becomes more expensive, production costs rise across the global economy while consumers have less disposable income. In effect, higher oil prices operate as a tax on consumers, reducing spending power and slowing economic growth.

The immediate market reaction to oil spikes often reflects these concerns, as we’ve witnessed in recent weeks. Investors have become concerned about the outlook for growth, inflation and central bank policy simultaneously.

In the words of Michael Lynch (Forbes): ‘The primary economic effect of an oil crisis is naturally due to increased oil prices on inflation and consumer income and spending. Higher oil prices lead to increased inflation; a rule of thumb says that a 5% increase in oil prices leads to 0.1% increase in inflation. The 50% increase we’re seeing now would therefore add about 1% to the inflation rate, or about one-third increase in current levels.’

In other words, oil shocks like the current one tend to produce the most uncomfortable environment for equity investors: slower growth combined with rising inflation, and pressure on both sides of the Fed’s dual mandate.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

But the Relationship is Weaker Than Many Assume

Despite the obvious impacts of higher oil prices, the long-term correlation between oil prices and equity market returns is surprisingly modest.

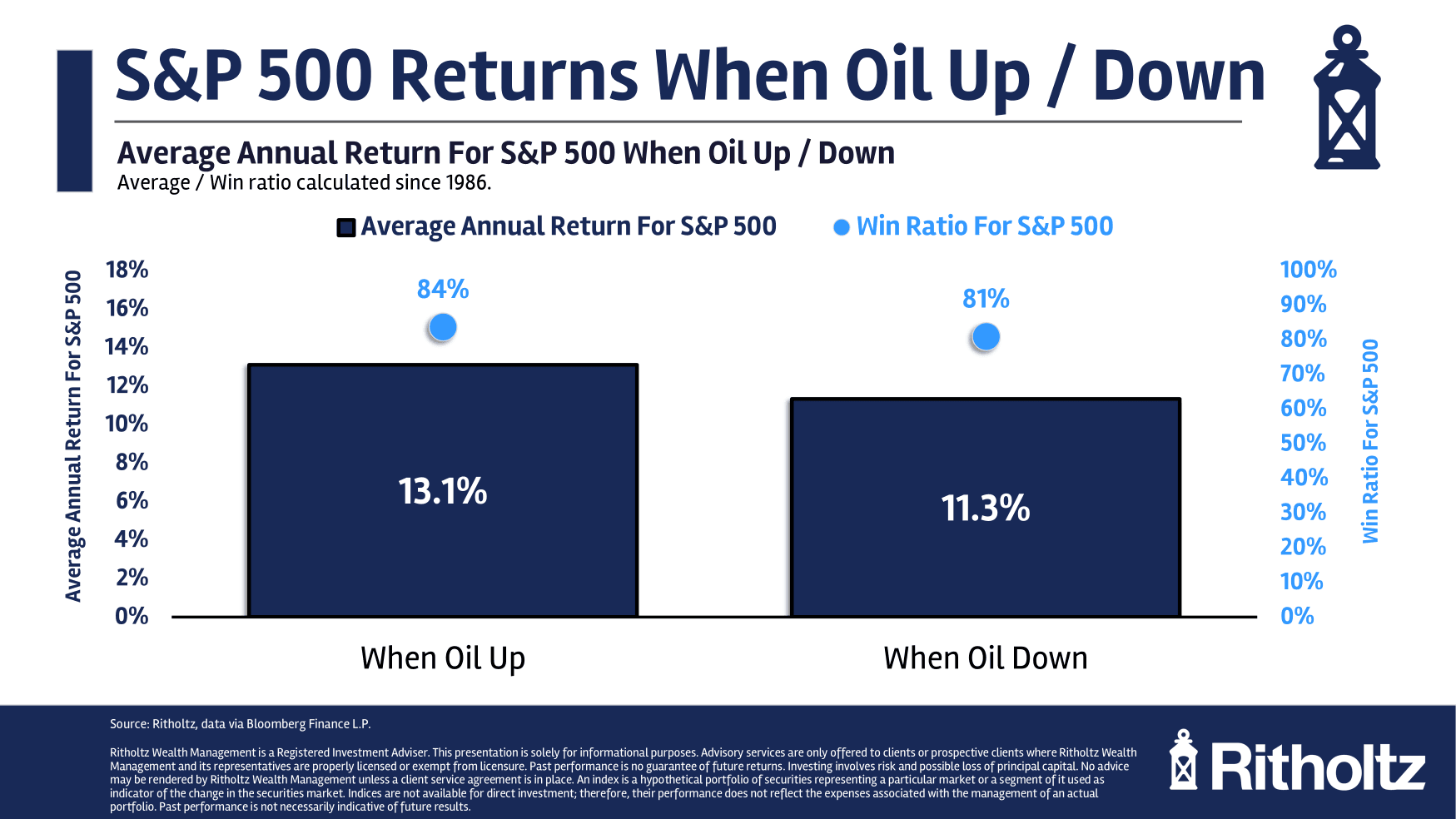

Moreover, contrary to consensus expectations, average S&P 500 returns have been higher in the years when oil has risen than in the years it has fallen. You read that right. Check out the chart below.

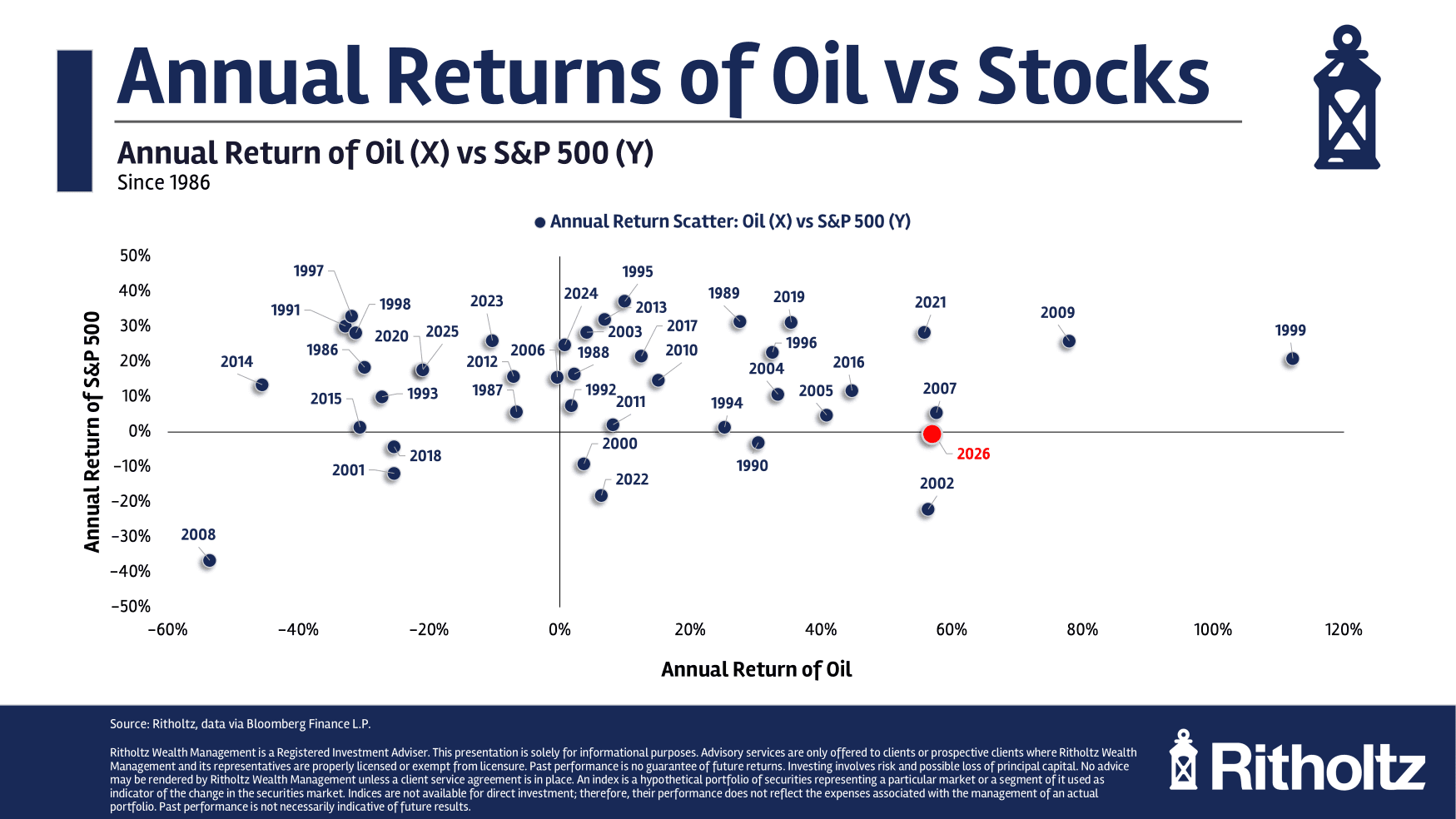

You can see the annual data behind these averages in this chart:

How do we make sense of a rising tax on the global economy being connected with stronger equity market returns like this?

The Cause of the Oil Spike Matters

The most important factor is why oil prices are rising.

When oil increases because of strong global demand, the effect on equities is often positive.

Higher energy prices in this scenario typically reflect expectations of rising global economic growth and industrial activity. Under those conditions corporate earnings are usually expanding, which supports global equity markets.

Conversely, when oil spikes due to supply disruptions or geopolitical shocks (like now), the effect is more negative.

The data concurs, at least in the short term:

In this scenario oil prices are rising because supply is constrained rather than because demand is strong. That combination tends to weaken global economic activity.

Hence, the recent closure of the Strait of Hormuz and escalating Middle East tensions has pushed oil above US$100 per barrel, and has triggered declines across global equity markets.

At this point, most analysts agree that further oil price rises are likely to impact the global economy and potentially trigger a broader equity sell-off. Equally, a swift end to the war would likely lead to lower oil prices and a gradual resumption of business as usual.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Sector Winners and Losers

Oil shocks rarely affect all equities equally. Instead they tend to trigger powerful sector rotations.

Energy companies are the obvious beneficiaries. Rising crude prices lead to much higher margins for oil producers and energy infrastructure companies.

Hence, the dramatic outperformance witnessed in major oil companies in recent weeks.

The potential upside in the energy sector is being amplified by the context of many years of low investment into new supply, and the sector’s low relative weighting in the S&P 500 (and global markets).

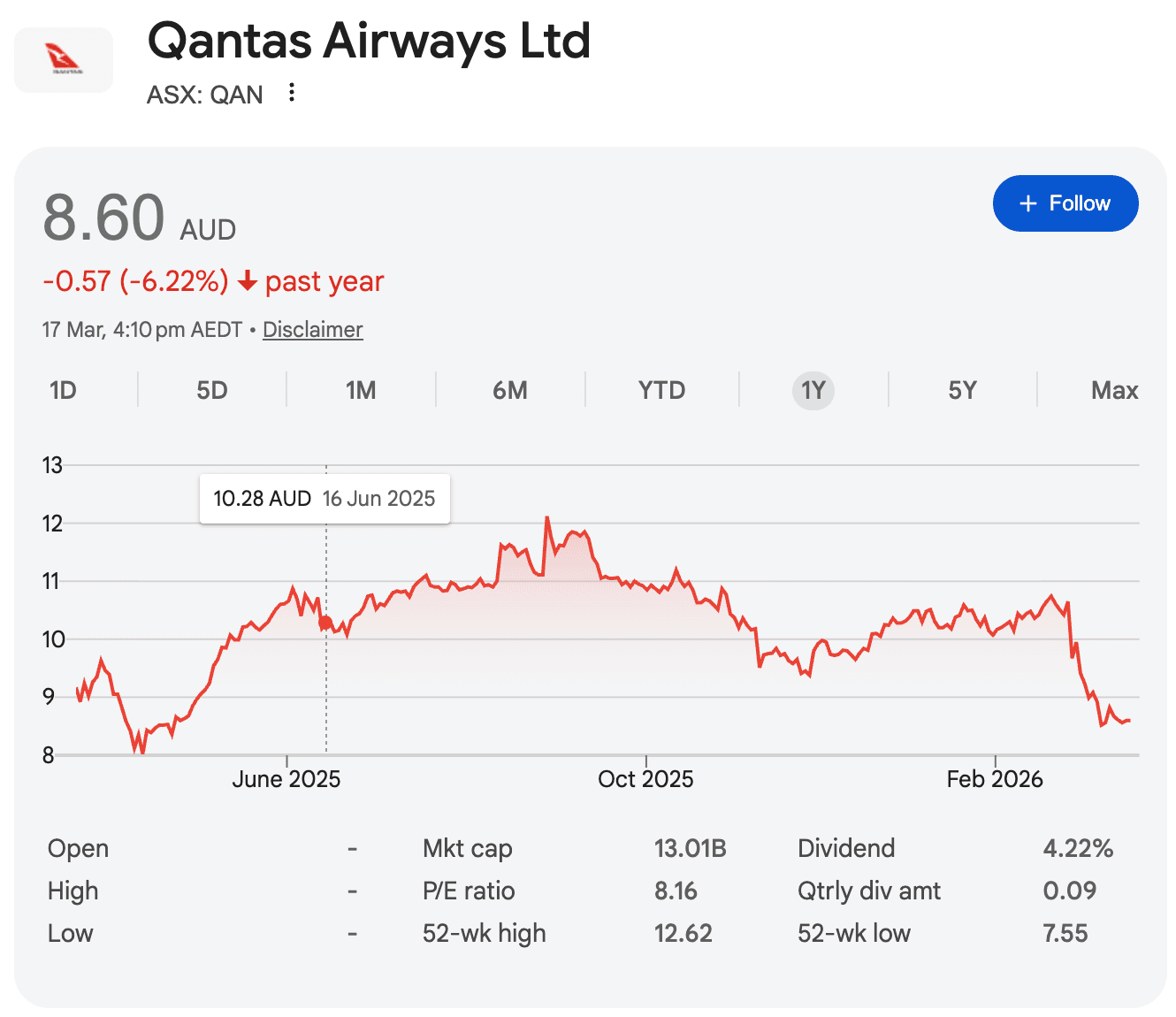

Conversely, fuel-intensive industries such as airlines, transport and chemicals tend to suffer when the oil price spikes. Rising energy costs compress their margins and weaken their earnings outlooks.

True to form, most major airlines have been underperforming in recent weeks.

Financial markets have also begun to price in rising inflation and interest rate expectations. This is hardly surprising. If higher oil prices have indeed added around 1% to global inflation, the Fed, the RBA, and other central bankers may respond by tightening policy, which could put pressure on growth stocks and highly leveraged sectors.

So while some sectors are outperforming and others are underperforming, the net impact of higher oil prices isn’t necessarily a market collapse. Genuinely diversified investors may be protected to some extent from the whipsawing between sectors.

Stay Calm and Carry On

The historical data shows that the long-term correlation between oil prices and equity returns is weaker than widely believed. Energy price shocks tend to lead to a rotation in market leadership rather than long-term bear markets. What matters more is the underlying economic environment, corporate earnings, and investor sentiment.

So while the Iran war rages, investors should focus on maintaining diversified exposure across global equity funds and ETFs. Diversified equity portfolios have historically proved resilient through multiple energy shocks. At the same time, maintaining exposure to quality companies with pricing power helps portfolios withstand higher input costs. The key is to treat oil as one of many macro forces shaping returns within the broader equity market.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

-h4ktuew2tuf5gql3onwm.png)

Recent Articles

View all articles-4yb643awg03namrcahu4.png)

-zrxpxihmn0inisejx8wx.png)

-vke5r81en85n0lawxvqo.png)