-tynzb3z5dtparcxsf2d2.png)

Why the Run on Real Assets May Be Just Getting Started

In a world dominated by all things technology-related, it’s been easy for investors to forget about real assets. Until recently, many did. But recently, a noteworthy shift began back toward the precious metals, commodities, infrastructure, and real estate of the real assets world. Their appeal is intuitively easy to understand. It’s their tangibility, while historically they’ve been viewed as inflation hedges and diversifiers.

But the real assets investment case has evolved of late. Real assets may be entering a new phase, rather than simply repeating past patterns. Two key shifts are driving this evolution: stronger fundamentals (lower valuations + policy tailwinds) and portfolio regime change (high market concentration + inflation/interest-rate uncertainty).

The upshot is that the relative attractions of real assets have rarely been higher. Whilst most portfolios have a 5-10% real assets allocation primarily for the inflation protection attributes, now may be time for a higher weighting…

Valuation & Fundamentals Aligning

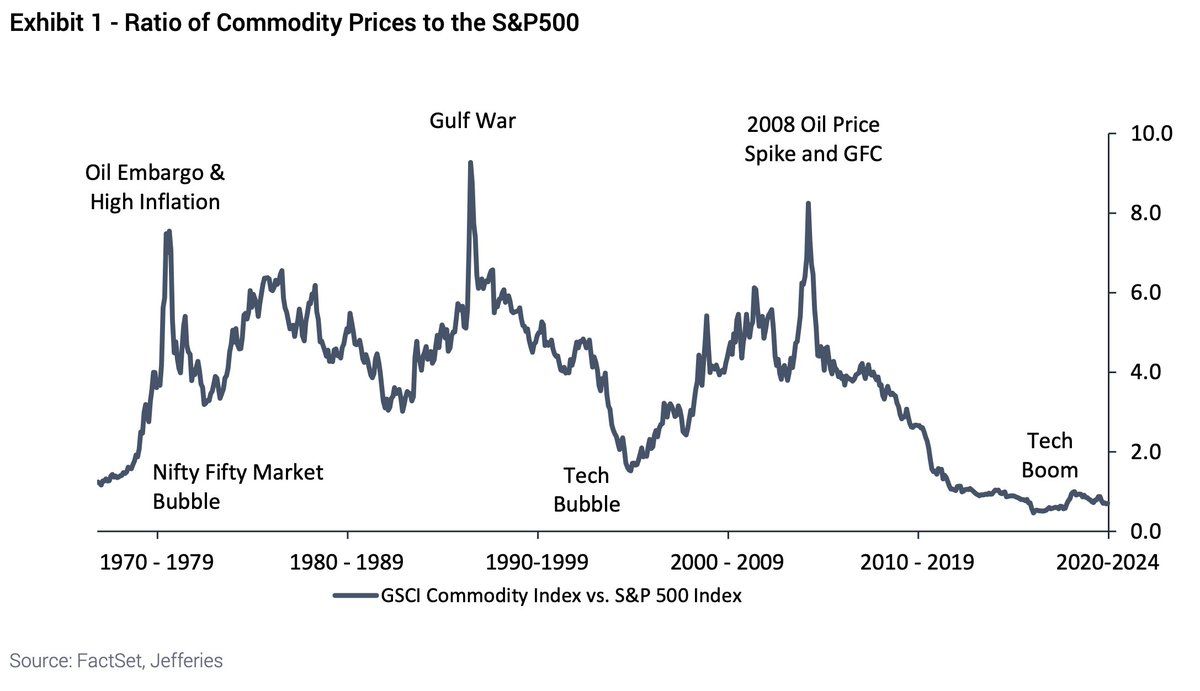

One of the strongest arguments that real asset outperformance may only be starting is valuation.

After a long period in which growth and mega cap technology companies have led global equity indices higher, commodities look cheap versus the broader market.

And it’s not just commodities. Valuation is an argument in favour of real assets in general.

As at 31st October 2025, the MSCI World Index was trading at a trailing price to earnings ratio of 24.8x, a forward P/E of 20.4x, a price to book ratio of 3.9x, and a dividend yield of only 1.6%.

In contrast, many real asset segments have lagged global equities over the last five years and that underperformance has left them trading on lower multiples and higher yields, as shown below.

For example, global listed real estate has underperformed global equities by 9% p.a. over the past five years, which has pushed their relative forward P/E multiples more than one standard deviation below the long term average. Moreover, listed real estate currently offers a dividend yield of 4% p.a., which is well above global equity yields.

Similar patterns are visible in listed infrastructure. The iShares Global Infrastructure ETF (IGF) offers a trailing P/E ratio of 20.6x and a price to book of 2.39x as at 21st November 2025, both of which are cheap versus the MSCI World even though the underlying businesses often have regulated or contracted cash flows.

This valuation discount appears historic. Russell Investments estimates that listed real assets are trading near a fifteen-year low on a P/E basis relative to global equities.

So investors have the opportunity to benefit not only from real asset income and earnings growth, but also from a potential valuation rerating over time

That rerating may come care of improving fundamentals. Macro conditions appear to be supportive of that outcome.

For example, falling real interest-rate expectations, still-sticky inflation, rising infrastructure investment, the energy transition, and the growing recognition that the equity market is overly concentrated (e.g. the top 10 stocks in the S&P 500 account for ~39% of its market cap) are all potential drivers of real asset outperformance.

Macquarie concurs with this view: ‘The combination of falling interest-rates and healthy global-growth has historically been a powerful one for real-estate returns.’

Real assets also generally benefit from built-in inflation hedges via leases linked to CPI, and long-dated contracted cash flows. That means in a world where inflation remains elevated but real growth fragile, real assets appear well-positioned to outperform with relatively low correlation to global equity markets.

In short, real asset valuations are less stretched than the broader market, fundamentals are improving, and the portfolio diversification benefits are becoming more acute.

The Gold Sector as a Poster-Child for Real Assets Being Back in Favour

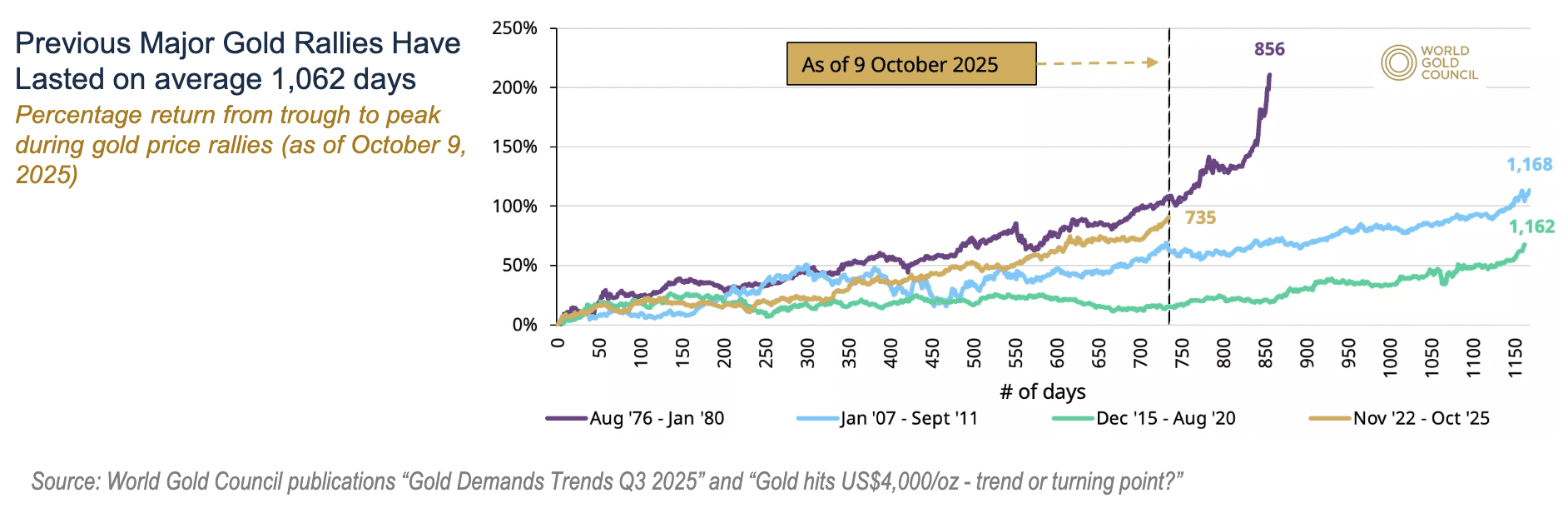

The gold market provides a vivid illustration of how real assets might be entering a new phase.

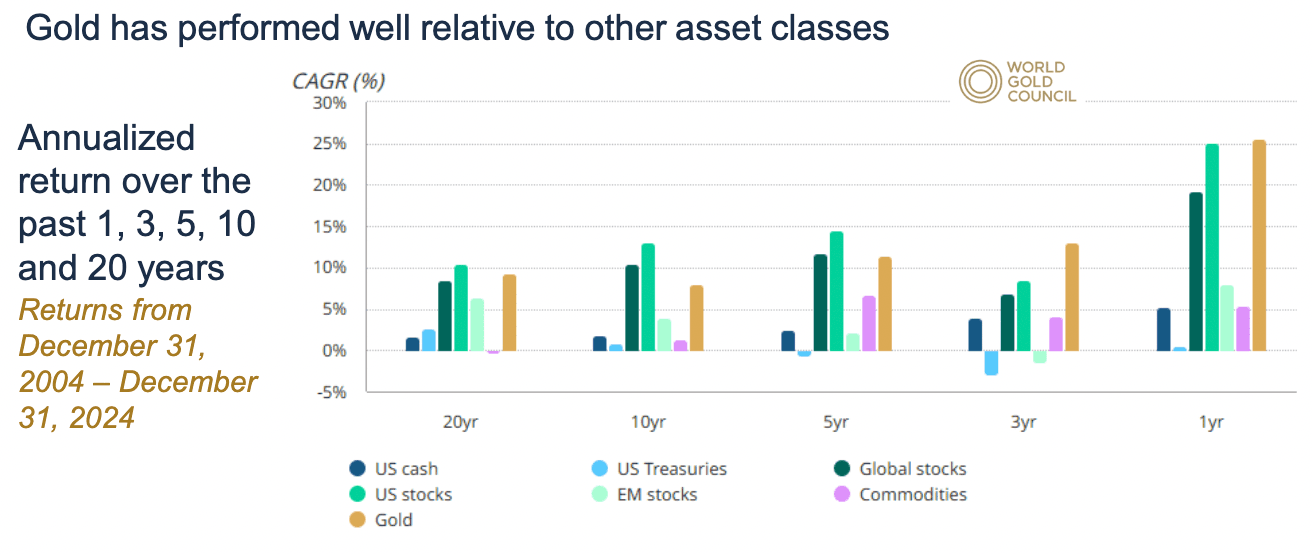

Driven by rising central bank and investment demand, the gold price has risen 56% over the past year.

Analysts at Morgan Stanley see further gold upside into 2026, citing strong ETF flows, central-bank buying and a backdrop of rising geopolitical risk, sticky inflation, and currency debasement. Demand growth is occurring across the board: investment in gold bars and coins rose 17% in Q3 2025, while physical-gold ETFs surged 134 % and central-bank purchases increased 10%.

Most investing frameworks treating gold as a hedge or boutique, but the size and breadth of the current rally suggest a regime shift may be underway: from cyclical commodity for trading to structural allocation.

Risks & Caveats to be Aware Of

Of course no investment is risk-free.

Real assets face headwinds too: inflation overshooting could push real yields higher if central banks respond by raising rates. Infrastructure and real estate valuations are exposed to supply/demand shifts (especially commercial real estate). And commodities may suffer if global demand weakens abruptly.

Nevertheless, many of these risks are already heavily priced in by the market. Hence, in comparison to the potential upside, real assets appear under-priced.

A New Innings Commencing for Real Assets

The investment case for real assets appears to be entering a fresh phase. They offer more valuation upside than most market segments at a time when the macro set-up is bullish. If one subscribes to the view that equity markets are relatively expensive right now, that interest-rates may gradually fall, that inflation remains a residual threat, and that global investment flows into infrastructure and commodities will broaden, then real assets may offer meaningful and asymmetric upside.

The gold market embodies this shift. Whereas gold was once a hedge asset, it appears to be emerging as a legitimate return driver for investors’ portfolios. If gold can deliver longer term upside, and if infrastructure and real-estate start outperforming driven by policy, capital flows, and their superior yields, then real assets may capture a more central role for next-generation portfolio construction.

So rather than the token 5-10% represented in most portfolios, allocating a meaningful portion to real-asset exposure may be prudent. The key is to maintain discipline by investing in high-quality real asset funds and ETFs calibrated to your risk profile. In a world in which global equities are looking fully priced, real assets may just be getting started.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

Related Articles

-v8lxc7275hr89z0hzkrz.png)

-s3ot3fhgl1y3jl4dxvk3.png)

Investments You May Like

Dexus Wholesale Australian Property Fund - DWAPF

The Fund invests in quality commercial properties, targeting assets in major metropolitan markets with high occupancy rates and stable income streams, underpinned by long-term leases with secure commercial tenants.

The Collective Property Fund

The Collective aims to provide Investors with a genuinely diversified portfolio of primarily direct property and Own Unlisted Direct Property Trusts.

Tycoon Core Income Fund

Tailor your investment to your individual risk profile, with a range of interest returns and security types.

Recent Articles

View all articles-ok9x7uwg0ypr232nekwu.png)

-x5zevcitnzrsy2mixx6e.png)

-7mc6hsayqab3oggarjw2.png)