A Young Investor’s Path to Wealth Without Acquiring a Property Empire

Simon Turner

Wed 25 Feb 2026 7 minutesThere’s a uniquely Australian breed of wealth creator who achieved financial independence before the age of 30 by accumulating a sprawling property portfolio.

People generally judge their success relative to others. So should younger investors follow in the footsteps of these ultra-successful property moguls? Or is there another, simpler pathway forward they should be aware of that might be aligned with their goals?

How Property Moguls Do It

Like all successful investing, becoming a property mogul depends on having the right plan.

The core strategy for most is to invest in properties which generate significant capital growth. Over time, that translates into accumulated equity which can be tapped for portfolio expansion.

In short, this investment strategy leverages the power of compounding along with the amplification of leverage. A property portfolio’s capital growth serves to fund further property investment which also compounds, and so on.

As the portfolio expands, its collective capital growth becomes a powerful engine of wealth accumulation.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

But…

Whilst this strategy looks compelling on paper, it’s not for everyone, and there are times when it’s harder to execute.

For starters, it’s important to understand that this strategy assumes rising leverage capacity, benign interest rates, and a housing market that keeps compounding without interruption.

Meanwhile, the arithmetic reality is that the average residential dwelling in Australia has entered the lofty heights of seven figures. In the September quarter of 2025, the ABS reported the mean price of residential dwellings at $1,045,400.

Whether or not this number can keep rising at the 8-10% p.a. many property investors expect is the million-dollar question. Maybe it will. Maybe it won’t.

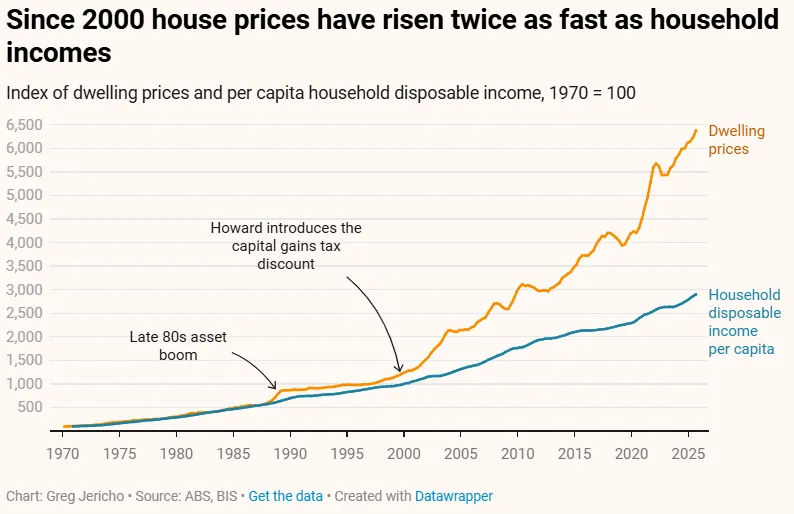

We do know that risk is a function of height, particularly relative to household disposable income. And right now, Australian property is looking extremely expensive versus household disposable income, as shown below.

This backdrop surely raises the risk that future property capital growth will be lower than in the recent past. And if we’re heading toward a period of negative capital growth, the above-mentioned property portfolio expansion strategy isn’t just high risk. It can lead to negative financial outcomes.

What’s a Young Person to Do?

If the optimal wealth-building path for young people isn’t necessarily acquiring 20 properties what is it?

The closest thing to a repeatable pathway is in combining three forces that don’t require heroic forecasting about the future:

Maximise your savings rate early.

Harness the power of diversified equity compounding over decades rather than years.

Control your own behaviour and emotions so you don’t sabotage your returns by selling at the wrong time.

It sounds so simple. That’s because it is. It isn’t easy though.

Most young (and older, for that matter) investors will discover that their biggest challenge with investing like this isn’t the market. It’s the third force on the list: controlling their emotions to ensure they can stick with their plan.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Time in the Market is Key

Start with the uncomfortable advantage that some property spruikers downplay: time is more powerful than leverage if you remain invested.

By way of background, the All Ordinaries Accumulation Index (which includes dividends) has generated a 12.2% p.a. return since 1985, but it’s important to understand the persistence required to capture these headline returns.

The challenge with all equity investing is that the returns can be volatile, with occasional sharp drawdowns and sudden recoveries along the way.

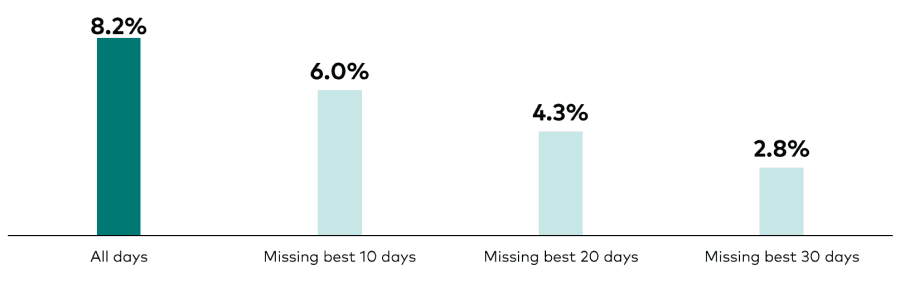

That’s precisely why selling at the wrong time is so expensive. Missing just a few days in the market can be catastrophic to returns. As per Vanguard’s analysis below, missing twenty days in the market can halve your returns over a quarter of a century.

Annualised total returns of Australian stock market from 2000 through 2025

So it’s time in the market that matters most, not timing the market.

That’s why a young investor’s primary edge is their long time horizon. It’s their capacity to save and invest each year, for long enough that compounding has time to work its magic.

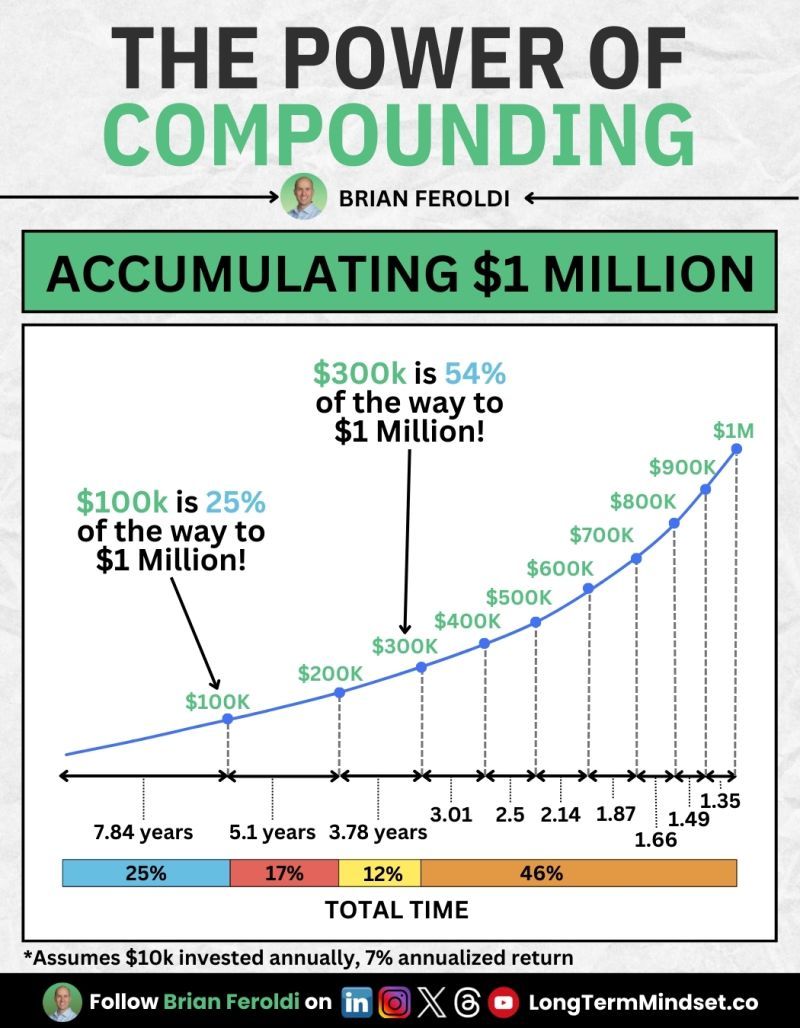

To do this, it’s important to understand and respect compounding for what it is: a means of accelerating your wealth accumulation. Over decades, its powers are extraordinary, as shown below.

Start Simple & Low Cost

In practice, the optimal starting strategy for most young investors (depending on their personal goals) is to begin constructing a core portfolio that’s diversified, low-friction, low-cost, and easy to hold through the inevitable market noise.

ETFs are a great starting point. For example, Vanguard Australian Shares ETF (ASX: VAS) is a straightforward building block providing broad Australian equities exposure, while Vanguard MSCI Intl ETF (ASX: VGS) provides diversified global exposure.

Through low-cost ETFs like these, young investors are able to start accumulating the type of broad, diversified market exposure needed to compound their equity returns over the long term. Importantly, they can add to ETFs like these in small increments as and when they can afford to invest.

👉 Tip: Investing each month once you’ve been paid and before you’ve started spending may well be the one habit that allows young investors to remain on track with their long-term investment plan more than any other.

Invest in Super

Utilising Australia’s superannuation system properly is also an important strategy for young investors. In short, it can meaningfully increase the share of your gross earnings that ends up compounding for you rather than for the ATO.

From 1st July 2024, the general concessional contributions cap is $30,000. Make sure you take advantage of as much of this benefit as possible each year.

For many young professionals, a disciplined pattern of concessional contributions, combined with a well-chosen investment option inside super, can represent their highest expected return decision on a risk-adjusted basis, because it increases their after-tax investable capital and forces time in the market.

Master Thyself

As mentioned above, the greatest challenge most young and old investors face is mastering their emotions during the investment journey. Many fail by selling at exactly the wrong time.

The simplest behavioural fix is to remove as many decision points from the investment process as possible.

For example, automate your contributions on payday.

Set a rebalancing rule that triggers infrequently, such as annually or when allocations drift beyond a defined band, and stick to it.

Reduce the regularity of your portfolio checking, because constant monitoring invites reactive action, the enemy of future returns.

Treat any urge to sell during a drawdown as a hypothesis that should be tested by AI, or against a written investment plan.

👉 Tip: If you’re thinking of selling but can’t write a calm, falsifiable reason for selling that would still look sensible if prices were 10% higher tomorrow, you’re probably responding to your discomfort rather than objective information.

Get Started

None of this denies that property can build immense wealth over the long term. But it’s not the only scalable pathway toward that goal, and an obsession with property can distract from simpler strategies which are also effective.

For many young investors, the optimal pathway to wealth is creating a structured investment plan that makes high-quality investing almost automatic, so you can focus your ambition on career and earnings growth while your portfolio does what you need it to do in the background: compound.

The key is to get started now.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.