Emerging markets (EMs) entered 2026 with strong structural momentum behind them, but the escalation of conflict in Iran has introduced a new layer of geopolitical risk that’s reshaping capital flows, commodity dynamics, and currency regimes.

The EM opportunity remains compelling, but returns will increasingly depend on selective exposure to commodity beneficiaries, domestic-demand-led economies, and technology exporters, rather than broader exposure.

A Market Darling as the Year Began

EMs entered 2026 with a sense of renewed purpose. Economic growth was well in excess of developed markets, capital was flowing in, and the global rate-cutting cycle that began in 2024 had reoriented investor attention away from the developed world.

Of course, that was before the US and Israel attacked Iran and added higher geopolitical risk and rising oil prices to the global, and EM, market narrative.

The upshot is that the previous optimism about the EM outlook remains present, but it has been refracted through a harsher and more complex geopolitical lens.

Oil Matters for EMs

Oil has become the most immediate transmission mechanism for that change.

Oil prices have swung sharply as markets attempt to price in disruption risk across the Middle East, and the consequences are unevenly distributed.

For oil exporters such as Saudi Arabia, Brazil and parts of Latin America, the environment has become more supportive.

For importers such as India and Turkey, it has introduced renewed inflationary pressure and currency strain.

Hence, the defining feature of EMs in 2026 is a rising dispersion of returns shaped by the interaction between local fundamentals and global shocks. The Iran war has exposed the degree to which energy exposure, fiscal flexibility and external balances now determine EM resilience.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

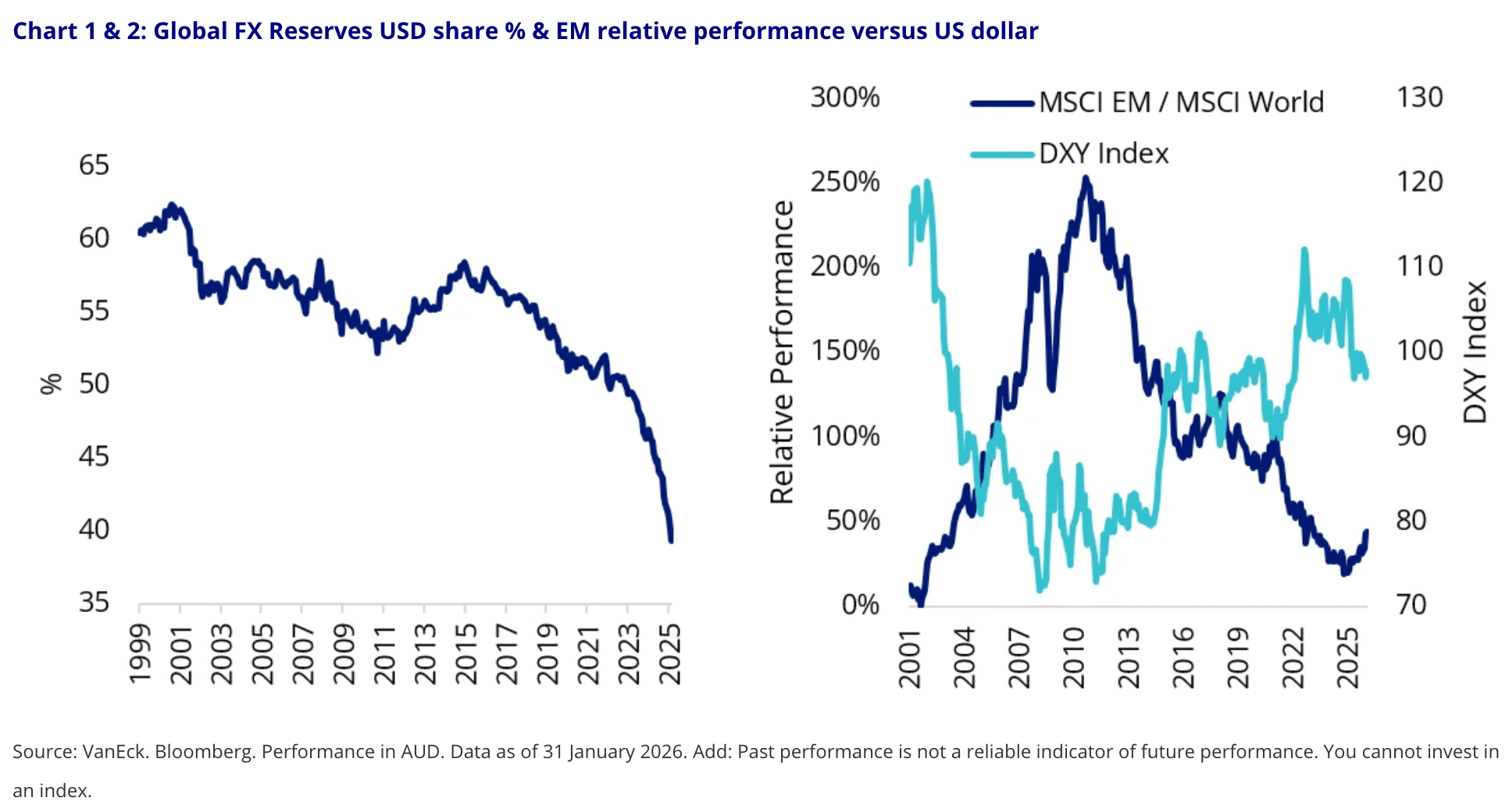

Currency Wars Also Playing a Role

The US dollar has long played a central role in EM performance since it has been regarded as the global reserve currency which, in turn, determines EM export flows.

However, the traditional safe-haven status of the US dollar has come under question of late. This is not just because of rising geopolitical fragmentation, but also due to US policy uncertainty and the lingering effects of tariff disputes.

A weaker US dollar tends to make higher-yielding currencies more attractive, increasing the appeal of EM currencies and equity exposure. Hence, EMs began outperforming a few months ago, as shown below.

For Australian investors, this backdrop introduces a powerful second-order effect. EM returns are no longer solely a function of equity performance, but also of currency translation. During periods when the US dollar softens, EM exposure can deliver a dual uplift.

The EM Narrative Remains Compelling

Recent EM outperformance hasn’t just been driven by the weakening US dollar. It also reflects a confluence of higher growth, more attractive valuations, and a global search for yield.

The Iran war hasn’t undone any of those forces. If anything, it has made them more selective and, therefore, more exploitable.

The structural core of this story remains anchored in the superior economic growth on offer in Asia, which is driving EM economic growth of more than double that of developed markets.

In particular, China, despite its well-documented challenges, continues to play a central role in global supply chains and technological production. Chinese policymakers are attempting to rebalance their economy towards stronger domestic demand, while maintaining a level of fiscal support that maintains economic growth near the government’s target. Moreover, the momentum in their technology sectors, particularly those linked to semiconductors and AI, remains strong. At the same time, concerns remain around Chinese household confidence and property weakness.

Elsewhere in Asia, the story is one of divergence rather than uniform strength.

South Korea and Taiwan continue to benefit from their position at the heart of the semiconductor ecosystem, while Indonesia and Thailand are increasingly driven by domestic policy support and consumption-led growth.

India presents a more nuanced case, where long-term structural appeal is tempered by valuation concerns and sensitivity to external shocks, including energy prices.

Commodities provide a second pillar to EM narrative, and extend beyond oil markets.

Recent strength in copper, aluminium and gold prices has reinforced the importance of resource-linked EM economies. In periods of geopolitical stress, gold in particular assumes renewed prominence. For EMs with significant mining sectors such as South Africa, this translates into improved terms of trade and stronger equity performance.

What emerges from this interplay of forces is a more fragmented but potentially more rewarding investment landscape.

Geopolitical risk, far from being a simple headwind, is acting as a sorting mechanism. It’s separating EMs with strong domestic foundations from those reliant on fragile external conditions. It’s also rewarding policy credibility, fiscal discipline and strategic positioning within global supply chains.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Yet Risks Remain

However, as with all investments, there are risks worth being aware of.

The Iran war intersects with broader geopolitical fragmentation, including US-China tensions and ongoing tariff disputes.

These tensions are expected to persist and continue to shape market dynamics. Trade flows may become more regionalised. Supply chains may fragment. Capital may become more selective and politically sensitive.

This environment is likely to reward EMs with strong domestic demand, economies less exposed to US trade policy, and markets with strong governance and capital access.

Investor Implications

The central insight is that EMs are no longer a single trade. They are a collection of distinct opportunities shaped by energy, technology and policy.

But since the Iran war began, there are nuances investors now need to be aware of:

- Commodity dynamics are now a central driver of EM returns.

- Currency shifts, particularly a weaker US dollar, could provide additional upside.

- Geopolitical fragmentation is increasing the dispersion or returns and making active selection more valuable.

The decision is how to invest in EMs in a way that captures the asymmetric return drivers created by current conditions.

In this market, the arguments in favour of actively managed funds are compelling. Funds such as Antipodes Emerging Markets (Managed Fund) allow investors access to immediately diversified funds which are being actively managed to benefit from the above-mentioned tailwinds.

There’s also an argument in favour of focusing on the core EM thematic of Asian technology. ETFs such as BetaShares Asia Technology Tigers ETF provide low-cost and targeted exposure to this theme.

Whilst the arguments in favour of broader, less focused EM exposure have arguably been diluted by recent events, for some investors the broader diversification of ETFs such as iShares MSCI Emerging Markets ETF (AU) remain worthy of consideration.

Enduring Appeal

The enduring appeal of EMs has always rested on their capacity to deliver growth that is both faster and less fully priced than that of the developed world. That remains the case today.

What’s changed is the path by which that growth is translating into returns. It is now more contingent, more uneven and, for the attentive investor, more interesting.

Funds Mentioned

The Fund typically invests in a select number of attractively valued companies exposed to emerging markets or listed on emerging market stock exchanges (usually a minimum 30 long holdings).

Retail Investor

Availability

Open for investment

Funding Stage

Unlisted Mature Fund

The fund aims to provide investors with the performance of the MSCI Emerging Markets Index, before fees and expenses. The index is designed to measure the equity market performance in global emerging markets.

Retail Investor

ASIA aims to track the performance of an index (before fees and expenses) comprising the 50 largest technology and online retail stocks in Asia (ex-Japan), including technology giants such as Alibaba, Tencent, Baidu and JD.com.

Retail Investor

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

-3i6bx8sqjbfe2qcm0orn.png)

-5bk99rneoh6q6ud0ea67.png)

-ayqymdg5wjaq90vnhi6r.png)

-4yb643awg03namrcahu4.png)

-zrxpxihmn0inisejx8wx.png)

-vke5r81en85n0lawxvqo.png)