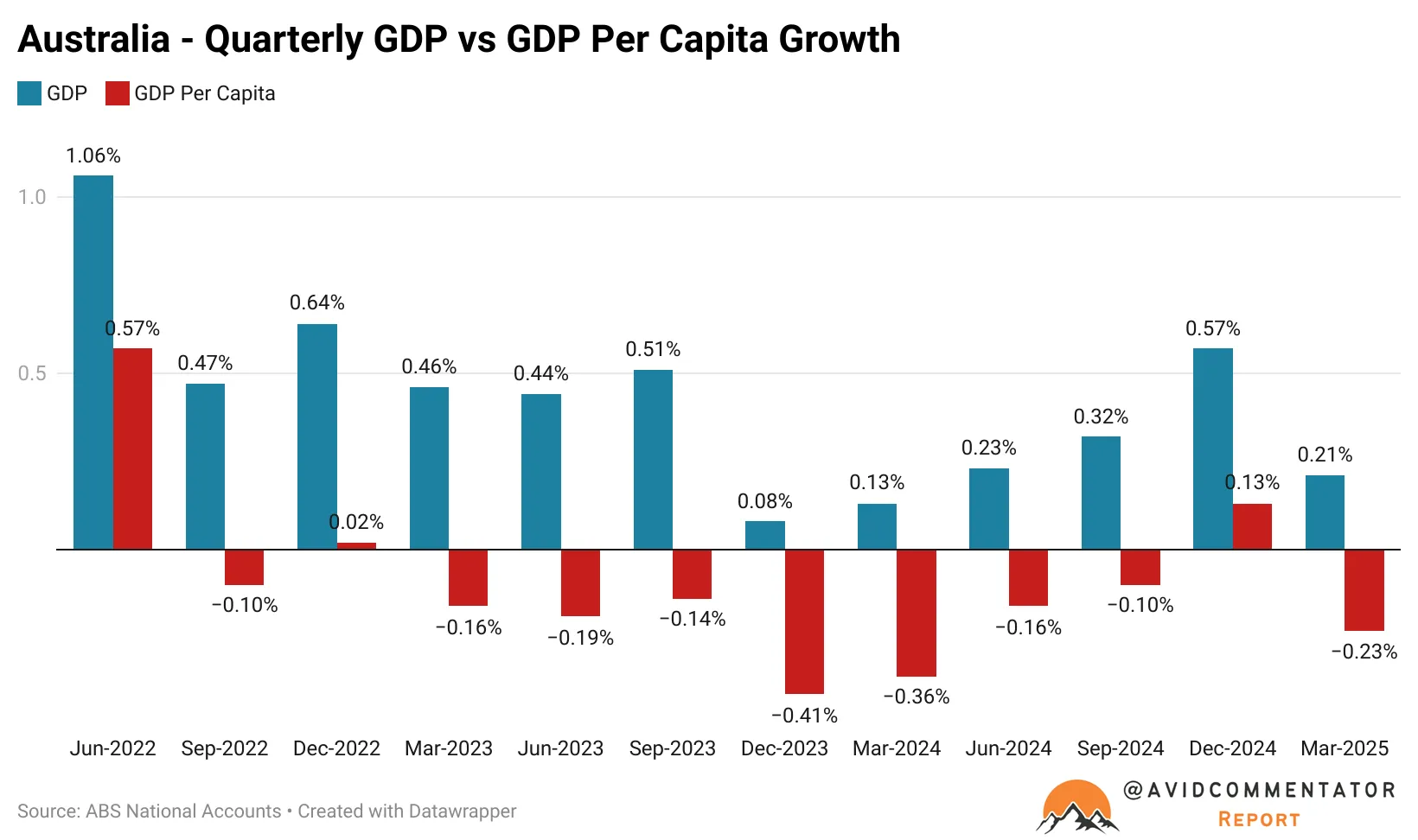

Australia’s GDP rose 0.3% in the March quarter and 2.5% over the year. While that’s not recessionary, it’s hardly exuberant and was once again negative in per capita terms. The main headwinds are subdued household and government consumption, while adverse weather hampered mining production and exports. On a more positive note, there’s been a lift in business investment linked to data centre machinery and equipment.

For investors, the domestic sectors with structurally growing demand, pricing power or capital investment tailwinds look better placed. The sectors which are dependent on discretionary spending, cheap debt or benign commodity conditions look more vulnerable.

The Australian Economy in Pictures

The Australian economy is still dependent on mining although less so than in the past: 9.9% of the country’s economic output comes from the mining sector, while 13.9% is generated from its largest contributor, health and education.

Business investment into data centre machinery and equipment was the largest contributor to March quarter GDP growth, even though the import-heavy nature of that investment muted its GDP impact through net trade.

Data centres benefit from sitting across multiple investment themes: electricity demand, industrial land, utilities, construction, telecommunications, engineering, cooling systems and listed infrastructure.

Growth is clearly the name of the game in this space. More physical assets are required to meet rapidly growing demand for digital capabilities.

Having said that, digital infrastructure assets can be sensitive to bond yields, regulation and refinancing costs. Data centre growth also depends on energy availability and grid investment.

Still, the underlying demand drivers remain stronger than in many of the more cyclical parts of the economy.

Winner: Construction

Construction is another winner, although not all construction is created equal.

Building approvals tell a nuanced story.

Total dwelling approvals fell 3.4% in April 2026 to 16,710, but were still 10.2% higher than a year earlier.

Private sector dwellings excluding houses were up 20.5% over the year, while the value of non-residential building rose 29.4% to $7.75 billion.

This is a classic two-speed signal.

Housing demand remains structurally strong because of population growth and undersupply, but feasibility is still difficult when labour, materials, finance and planning delays remain pressure points.

Non-residential work, infrastructure and large development fund projects look healthier than the supply-constrained parts of the residential development market.

Winner: Healthcare

Healthcare and social assistance remains one of Australia’s most durable economic engines.

Jobs and Skills Australia reported in April 2026 that healthcare and social assistance employment grew by 95,000 workers, or 4.1%, over the previous year.

This solid demand is driven by demographics, disability services, aged care, hospitals, allied health and chronic disease management.

These are defensive drivers which aren’t easily deferred in the way a holiday, renovation or new car purchase can be.

The trade-off is that listed healthcare companies can face wage pressure, regulation, government funding risk, litigation, offshore earnings volatility and high valuation multiples.

But as a sector, healthcare remains one of Australia’s strongest long-term demand growth stories.

Winner: Tourism and Hospitality

Tourism is another sector with momentum behind it.

Tourism Research Australia reported 8.5 million international visitor trips to Australia in the year ending March 2026. Its 2030 forecasts point to international visitor arrivals reaching 10.9 million and international visitor spend reaching $46 billion.

It’s not just the tourists who are enjoying their time eating, drinking and exploring. Household spending data shows that domestic hospitality demand remains solid despite cost-of-living pressure. Household spending rose 1.3% in May, with strong rises in discretionary categories including hotels, cafes and restaurants, up 1.9%, and clothing and footwear, up 2.7%.

That’s encouraging for travel, hospitality, airports, leisure and selected consumer services.

But higher mortgage payments and insurance bills are still likely to limit household spending flexibility.

The better-positioned businesses are likely to be those with pricing power, strong brands, exposure to domestic and international demand, and disciplined cost control.

Loser: Mining

Mining has been a short-term drag on the economy.

During the first quarter of 2026, mining sales of goods and services fell 3.1% in chain volume terms, while mining gross operating profits fell 9.1%. Adverse weather hampered both production and exports.

It’s not all bad news. Australia still has world-class iron ore, gas, gold, copper, lithium and critical minerals exposure. The Department of Industry expects the country’s critical minerals export revenues to rise from $11 billion in 2024-25 to $14 billion in 2026-27.

However, mining is a price-and-volume business. When both are growing, the sector benefits from the cyclicality of its operational leverage.

It can be a portfolio diversifier and inflation hedge, but it will always be exposed to China, weather, capex cycles, global supply increases, currency and commodity-specific shocks.

Loser: Retail

Retail is under pressure.

During May, retail volumes fell 0.2%, even though they were still 1.5% higher over the year.

So, households are still spending, but inflation, mortgage costs, rent, insurance and other rising costs of living are forcing sharper trade-offs.

These are likely to be longer-term issues. The RBA expects underlying inflation to remain above its 2-3% target range until mid-2027.

So, for investors, exposure to the domestic consumer sector should be selective.

It’s time to be more cautious on discretionary retailers exposed to big-ticket purchases, fashion, homewares and other postponable spending. Businesses with weak pricing power or high operating leverage are especially vulnerable.

More resilient exposure is likely to come from retailers tied to essential spending, value-conscious consumers or structural shifts, including supermarkets, discount formats, selected travel operators and high-quality online platforms.

In a weaker consumption environment, the gap between defensive, value-oriented and discretionary retail models should matter more than headline retail sales alone.

A Nuanced Story

Australia’s economy is not weak everywhere, nor strong everywhere. It’s uneven.

Being more selective about your domestic exposure makes sense at this juncture.

The winners are likely to be those sectors benefiting from structural demand, capital investment or demographic support. For example, data infrastructure, non-residential construction, healthcare and tourism are positioned to benefit from visible demand drivers.

The losers are likely to be those sectors exposed to weaker volumes, higher input costs, stretched consumers or commodity volatility. Mining and retail are currently navigating these sharper cyclical risks.

And remember: sector-driven investing can improve portfolio precision, but it can also increase concentration risk. Being genuinely diversified is prudent for most investors.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.

The SpaceX IPO may go down as one of the defining market events of the decade. Not simply because of its size, or its role in catapulting Elon Musk into the world’s first trillionaire. And not even because it’s trading at a somewhat shocking 2026 EV/EBITDA ratio of 222x.

The number of investors proclaiming they’ve made millions from AI infrastructure stocks is on the rise. That’s a dubious data point that’s surely synonymous with taxi drivers sharing the same hot stock picks near the peak of the market.

Australian consumers are feeling mighty gloomy right now. It’s easy to understand why. The war in Iran, the sharp rise in fuel prices and the proposed removal of the capital gains tax discount has Australian households unusually worried about the future.

The Federal Reserve has a new chairman in position. Kevin Warsh recently chaired his first meeting and the message was clear: global markets need to get used to less hand-holding looking forward.

Retiring soon and wondering how to structure your investments? There are a range of strategies you can follow, from maintaining your existing approach to shifting into a new strategy. One approach investors use is known as the 3-bucket strategy.

-qp0n60ykj8tsr669unwt.png?_a=BAMAAAcg0)

-ayqymdg5wjaq90vnhi6r.png)

-ulhzagvbsmdk2tc72zgj.png)

-l7rg6lkopgoa2x6pxhua.png)

-s5c0uf81il26meg3icyx.png)

-5bk99rneoh6q6ud0ea67.png)

-pxiuel5d343plbjy7hdo.png)