The number of investors proclaiming they’ve made millions from AI infrastructure stocks is on the rise. That’s a dubious data point that’s surely synonymous with taxi drivers sharing the same hot stock picks near the peak of the market.

The implication is unavoidable: the risk appears to be rising that AI stocks are forming a bubble.

Given most Australian investors are exposed to this theme through their global fund and ETF exposures, we investigate the risk of an AI bubble below.

AI Embedded in Global Portfolios

If you’ve global exposure, your portfolio has almost certainly benefited from AI as a tailwind over the past couple of years.

The AI trade has become embedded in broad global equity indices, large-cap ETFs, superannuation portfolios, and managed funds.

The upshot is that even investors who’ve never bought a dedicated technology ETF may already own a meaningful slice of Nvidia, Microsoft, Alphabet, Amazon, Meta and other AI-linked businesses through their diversified global equity exposure.

This raises an obvious question: is your portfolio more exposed to the AI trade than you realise?

Why the Bubble Question is Back

AI infrastructure stocks have been on fire of late.

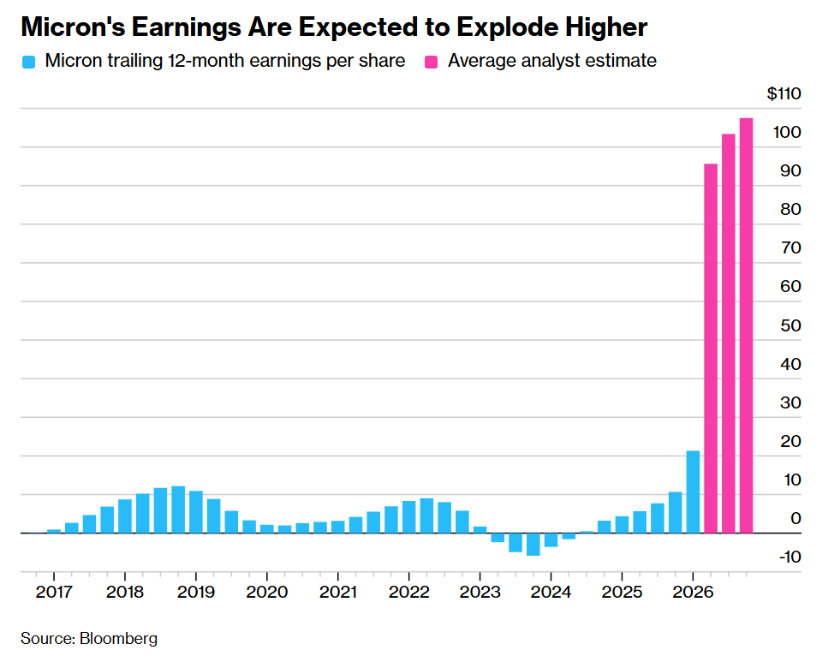

Case in point: Micron is the eleventh company to join the trillion US dollar club as demand for its semiconductor products has skyrocketed thanks to the AI rollout.

Unlike the late-1990s dot-com boom, companies like Micron are highly profitable, cash-generative businesses with dominant market positions.

And they are directly benefitting from the AI rollout. Check out Micron’s earnings forecasts.

Micron isn’t an isolated AI beneficiary.

Powered by the same tailwinds, the technology and communication services sectors now make up half of the S&P 500, matching the weighting of all the other nine sectors combined.

Source: A Wealth of Common Sense

So, is this a bubble in the making?

Firstly, it’s worth asking what is a bubble?

Cliff Asness once defined it as: “a price that no reasonable future outcome can justify.”

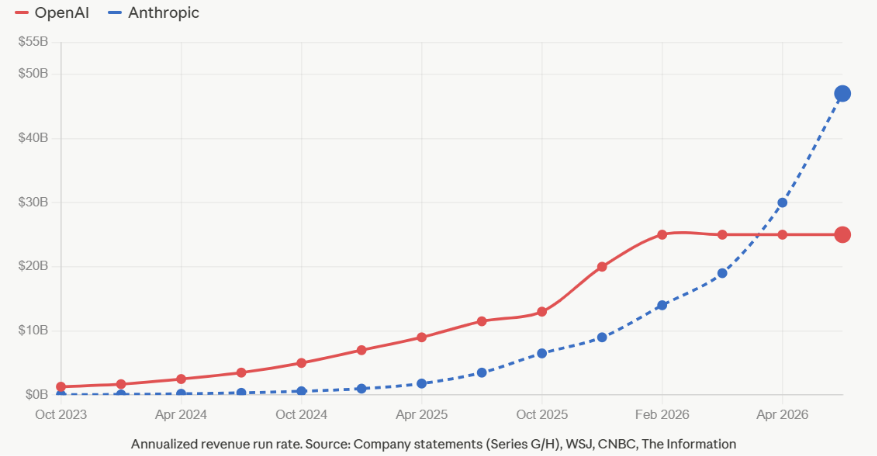

The problem with calling a bubble in AI stocks based on this definition is that the earnings estimates are following many of these AI beneficiaries upward. In other words, while valuations have also been expanding, the AI opportunity is turning into real business opportunities for many of the AI infrastructure stocks benefiting from the capex boom.

Check out the revenue forecasts for OpenAI and Anthropic.

And more broadly, the AI trade in the likes of Micron is one of the main drivers of the recent substantial increase in S&P 500 earnings forecasts.

It’s not often you see short-term S&P 500 earnings upgrades of that magnitude.

So, in AI, we appear to be dealing with a profitable and potentially transformative opportunity which is very different from the last technology bubble.

That’s not to say an AI bubble is not building here driven by excessive spending, hype and unrealistic expectations.

It’s just that recognising whether it’s a bubble or not is unusually difficult given the context of it being a genuinely transformative technology that’s leading to earnings upgrades and rising expectations.

In fact, given the vast range of potential outcomes we’re facing in an AI-dominated world, giving a definite answer as to whether an AI bubble is building may be unrealistic.

US Market Concentration a Proxy for AI Bubble Risk

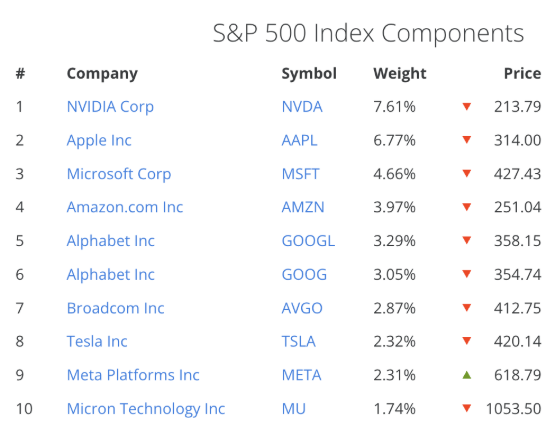

One thing we can say for sure is that the US market is becoming much more concentrated care of the growing dominance of the tech sector, which may actually be a good proxy for AI risk.

On that note, the ten largest constituents of the S&P 500, all of which are tech stocks benefitting to varying degrees from the AI trade, account for a hefty 39% of the index, while the largest single constituent, Nvidia, represents 7.6%.

Source: S&P Dow Jones Indices

That’s not automatically bearish.

Market leaders often become leaders because they are doing many things right.

But concentration risk to this extent changes portfolio risk.

A broad US equity ETF may look diversified because it holds hundreds of companies.

In practice, its performance may depend upon a few mega-cap technology names, all of which are regarded as part of the AI trade.

In short, it’s high time to be aware of how exposed you are to these few stocks, and to this one AI trade.

The AI Trade is No Longer Just American

This is a global theme.

One reason the AI boom may be more sustainable than a simple single-stock mania is that it has spread well beyond the US.

South Korea, Taiwan, China and Japan have all participated strongly, helped by their semiconductor, memory, foundry, hardware and robotics exposure.

This is significant because AI infrastructure is a global supply chain.

Nvidia may be the symbol of the boom, but Taiwan Semiconductor Manufacturing Company, Samsung, SK Hynix and Japanese automation firms are also central to the story.

For investors, this creates both opportunity and risk.

While it’s bullish on the way up, a global AI boom increases the hidden correlations within global funds and ETFs. In a genuine AI-led correction, US mega-cap technology, Asian semiconductor manufacturers and thematic ETFs may all fall together.

Hence, investors should look past fund labels.

A portfolio holding US equities, global equities, Asian equities and technology ETFs may appear diversified by region, but still be highly exposed to the same AI capex cycle.

The Real Pressure Point: Capex

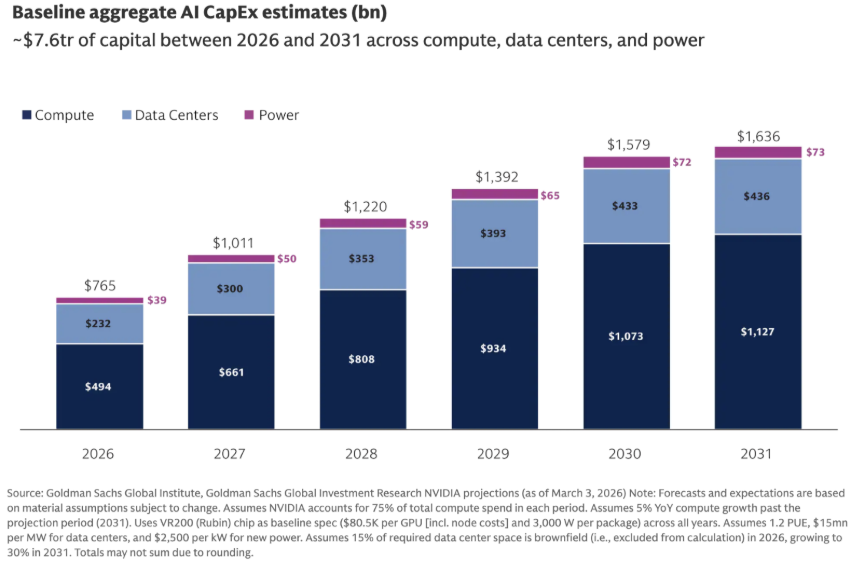

The biggest concern behind recent AI-driven stock moves is the scale of AI capital expenditure.

Goldman Sachs has projected that AI spending by Meta, Microsoft, Amazon and Alphabet could reach US$5.3 trillion by 2030, with broader AI infrastructure spending potentially reaching US$7.6 trillion over five years.

2026 capex expectations of US$765 billion would be roughly double 2025 levels.

That level of spending can be read two ways.

The bullish case is that hyper-scalers are building the infrastructure layer for the next era of computing. If AI becomes embedded across software, advertising, healthcare, logistics, finance and industrial automation, the spend may be justified.

The bearish case is that companies are racing to build capacity before the revenue model is fully proven. If AI usage grows but monetisation disappoints, investors may begin asking harder questions about returns on invested capital.

This is the scenario in which AI bubble risk becomes more prevalent.

In an investment boom, capital often floods into the right idea at the wrong price.

What it Means for Investors

While picking the exact top of the AI cycle probably sounds like the best strategy here, that’s rarely possible.

The sector may have topped already, or it may run another 50%, or 100%. No one knows. That’s the nature of investing.

The better approach is to stress-test your portfolio exposure.

Start with these questions:

What percentage of your portfolio is exposed to US mega-cap technology?

Do your global equity funds overlap heavily with your technology or thematic ETFs?

Are your emerging market or Asian equity holdings also exposed to the semiconductor cycle?

Do you hold defensive assets that could behave differently in a technology-led sell-off?

Are your income assets liquid, diversified and suitable for your risk profile?

They are not a cure-all, and they carry their own risks, including credit risk, duration risk, and liquidity constraints. But they help reduce reliance on the one equity theme.

Key Takeaways

AI may be real, useful and economically important, while still producing bubble-like conditions in markets.

Market concentration is now a major risk, with technology and AI-linked companies making up an unusually large share of US equity indices.

The AI trade has gone global, particularly through semiconductors and infrastructure, which means regional diversification may not reduce AI exposure as much as investors expect.

Capital expenditure is the key data point to watch. If spending keeps rising faster than monetisation, markets may become less forgiving.

Is AI a Bubble?

The honest answer is that some AI plays may be already in bubble territory, or may be there so soon.

That means investors should be focused on separating the technology’s fast-evolving bullish narrative from the price being paid for exposure to it.

In the short term, AI exposure may well produce disappointing investments for those who buy the most crowded assets after expectations have already run too far. History suggests transformative technologies often create both great companies and painful market corrections.

For now, the best question to ask may well be: ‘How much AI risk do I already have, and what is counterbalancing it within my portfolio?’

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.

AI has quickly established an integral role in fund managers’ investment processes. For most, it has already become an integral part of their investing machinery. Fund managers are using it to read more, screen faster, test risks earlier and monitor their portfolios across larger pools of data.

Just when you thought the Trump administration had surprised investors into a state of expecting anything, they went and restricted foreign access to Anthropic’s advanced AI models due to national security concerns. Whilst those restrictions were later lifted, the incident highlighted how trigger-happy the US Government has become when it comes to interpreting what’s in the country’s national interests, including across the free markets the US used to advocate for.

Technology has made investing easier than ever. Australian investors can now buy shares, compare ETFs, research managed funds, watch market videos, read fund updates and place trades from their mobiles.

Access to the investing world has exploded in the last few decades. Investors may once have required brokers to do their trading, or apply directly to fund managers to invest. These days, investors have a range of options, direct and indirect for their holdings.

Australian households are carrying some of the highest debt loads in the developed world, yet the Reserve Bank is still weighing whether to raise rates again. In the event the inflation print due out on July 29th runs hot, a fourth RBA rate rise may become more likely than not.

Recently, I detailed the 250-year rise of the industrial property sector, a transformation that has seen it evolve from the physical backbone of early manufacturing and storage into one of the most critical forms of modern economic infrastructure.

-vke5r81en85n0lawxvqo.png)

-ovpesoiwa1arap1qzn80.png)

-x5zevcitnzrsy2mixx6e.png)

-2g2znos21mscjwb8ey53.png)

-1aglg148l289gwh7jpc5.png)

-yfc6hfryydk3rz06im3j.png)