Overvalued vs Undervalued Sectors in 2026: Where Smart Investors Are Reallocating Now

Simon Turner

Thu 2 Apr 2026 8 minutes2026 is emerging as a year when it pays to understand what’s happening beneath the surface of markets. Whilst global equity markets have been weaker, there have been a number of consequential sectoral shifts behind the index headlines, some of which have insulated savvy investors from the broader weakness. Moreover, some of these shifts may be here to stay, determining the market outlook for the full year and beyond.

A Relatively Weak Start to the Year

We’re only three months into 2026, and it feels like we’ve already witnessed a game of two halves; before the US-Israel attack on Iran, and after it.

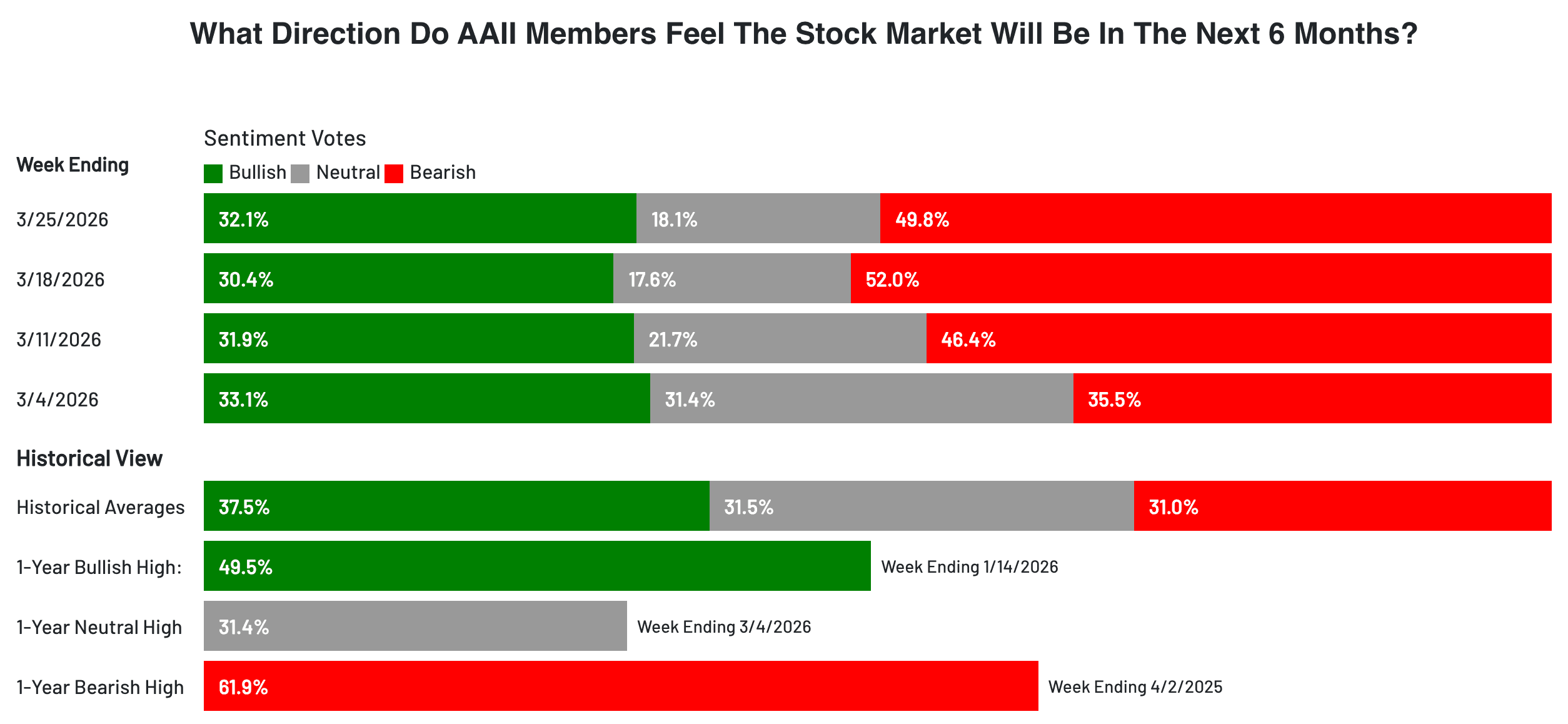

We’ve certainly entered a more pessimistic phase. Recent sentiment surveys show investors are currently unusually bearish about the market outlook (which is often a bullish signal):

This has translated into weaker equity market returns. At the time of writing, the MSCI Global Index is down 6% year to date, with similar performance in the US and Australian markets.

The End of Uniform Markets

At face value, global equity markets look slightly more attractive than they did late last year.

Global earnings growth expectations remain upbeat with 11.4% growth expected this year, and a similar outlook in 2027.

As a result of recent weakness, the price-to-forward-earnings ratio has fallen to under 19x, still relatively expensive but below previous market peaks.

Markets, in other words, are being carried more by profits than expanding optimism.

What’s more interesting is the divergence of valuations across sectors.

As shown in the Z-scores (a measure of standard deviations from the mean) below, US value, the Australian market, and the broader US market look relatively expensive in a global context. Conversely, technology, energy, Japan, and Emerging Markets appear to be more reasonably valued.

So, what’s going on here? Why are some sectors outperforming whilst other are languishing?

In a word, inflation. It has proved more persistent than many central bankers and investors expected. And with recent geopolitical tensions pushing oil prices above US$100 per barrel and unsettling global markets, inflation expectations have shocked on the upside. That’s leading to reduced expectations of further cuts from the Fed, and more hawkishness from most of the world’s central bankers.

These developments are serving to focus investors’ attention on cash flow today over promises of growth tomorrow.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

What Next?

Given recent trends, what should we expect next?

1. Technology: from Dominance to Dispersion

Technology remains a focal sector in global markets as the AI revolution gathers pace. The sector’s earnings outlook is still robust, and it continues to exhibit relatively strong earnings growth expectations. Yet its status as the unquestioned market leader has weakened of late.

On that note, recent performance has been uneven. Whilst pockets such as cybersecurity and cloud computing have shown resilience, the broader technology sector has clearly lost the momentum that drove dramatic outperformance in recent years.

The issue isn’t growth. It’s valuation. Many tech stocks are currently pricing in strong long-term growth. In some cases, the market appears to have priced in an overly optimistic outlook.

This suggests that technology has ceased to be a homogeneous trade. Investors are beginning to differentiate between stocks with durable earnings power and those reliant on distant and optimistic growth expectations.

What Next: The days of everything tech-related outperforming appears to be over for now. Stock picking within the tech sector is likely to matter more as a result. So, whilst it’s entirely feasible that profitable market leaders such as Alphabet, Microsoft, and Amazon may resume outperforming after the recent sell-off, it’s less likely that the entire global tech sector will benefit from the exuberance that drove speculative valuations to extremes in late 2025.

2. Consumer Staples: Expensive Safety

With technology losing its valuation premium, consumer staples may be the next to follow.

In recent years, the sector has benefited from growing investor demand for defensive income. That demand has pushed valuations to levels that appear difficult to justify given the sector’s modest growth prospects and cost base challenges due to rising inflation.

In an environment of rising yields and inflation, the sector’s appeal is less compelling than it once was.

What Next: Investors allocate to defensive sectors such as consumer staples for expected outperformance during market selloffs. However, when valuations and expected earnings growth is challenged by inflation, that appeal is arguably diluted. Consumer staples may struggle to outperform as a result.

3. Materials: The Limits of Momentum

The materials sector illustrates the recent tension between earnings strength and valuation risk. After a difficult few years, this sector is expected to deliver earnings growth of more than 30% in 2026 driven by higher commodity prices, particularly in critical and strategic minerals.

But commodity cycles are rarely linear. Recent geopolitically driven volatility in metals markets, including sharp declines in mining-related ETFs, shows how investors view this sector: high risk and prone to sharp reversals.

What Next: The recent sharp selloff creates opportunity in the relatively undervalued materials sector at a time when expected earnings growth is trending upwards. Hence, this may well prove to be an opportunity in hindsight, although investors should be prepared for more of the same: sharp rallies followed by equally sharp selloffs. Historically, it’s only during the euphoric (read: late) stages of a commodities bull market that volatility mainly works in an upward direction. That suggests we’re still likely early- or mid-cycle.

4. Energy: A Re-rating of Real Assets

If there’s one sector at the heart of the current rotation, it’s energy. Rising oil prices, geopolitical uncertainty, and supply constraints have combined to support the sector’s earnings outlook and valuations.

The foundations of a long-term recovery appear to be in place. Unlike previous cycles, energy companies have shown greater capital discipline in recent years, favouring shareholder returns over expansion.

What Next: In a world in which inflation risk is rising, real assets have regained their appeal. Whilst oil prices are likely to remain volatile in both directions, the arguments in favour of long-term energy sector outperformance have rarely been stronger.

5. Financials: Beneficiaries of Higher Rates

Financials, particularly in Australia, have benefited from rising interest rates which have supported the sector’s net interest margins, whilst credit growth has remained resilient.

Earnings expectations for the sector have been revised upward, reflecting this improved outlook, although valuations have also risen.

What Next: Financials are positioned to benefit from rate hikes, so the sector provides compelling protection against rising inflation. Further short-term valuation upside probably depends on further rate rises though.

6. Healthcare: Stability with Growth

The healthcare sector’s appeal lies in its consistency of returns in all market environments. It offers structural growth, driven by demographics and innovation, but with less sensitivity to economic cycles than most sectors.

What Next: Healthcare valuations aren’t as compelling as they were a few months ago, but healthcare’s defensive appeal may lead to growing investor interest if recent volatility were to continue. Expect outperformance during market sell-offs and underperformance during recoveries.

7. Infrastructure: Critical Assets

Infrastructure has become central to the emerging markets narrative following the Iran war, which has exposed the fragility of key trade and energy routes.

At the same time, investment into the sector is accelerating. The World Bank estimates emerging markets need over US$4 trillion p.a. in infrastructure spending through 2030, whilst the International Monetary Fund puts the required investment at US$5 trillion p.a. by the end of the decade.

What Next: Infrastructure is a core exposure within emerging markets. These are assets which are supported by long-term demand, policy backing, and increasingly critical roles in energy security, supply chains and economic growth. Whilst higher interest rates may impact some highly-indebted infrastructure plays, the broader sector is likely to perform defensively.

8. Gold: The Return of Insurance Demand

The renewed strength in gold reflects broader uncertainty about the US dollar, inflation, and geopolitical risk. In response to so much uncertainty, investors are placing a higher value on traditional hedges.

What Next: Gold is effectively insurance rather than growth. With markets in the midst of repricing risk, the value of gold as insurance is expected to remain buoyant. So, the recent sector selloff appears to offer investors an opportunity to enter the sector at a more attractive entry point.

A More Selective Market

A defining feature of 2026 is the widening divergence of sectoral returns as markets fragment along lines of valuation, earnings quality, and macro sensitivity. The upshot is that sector allocation is becoming a more important determinant of performance. It seems fair to expect more of the same through to the end of the year.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.