-uin4c8n9fw7agaoxnm93.png)

Feel Behind on Investing? The Biggest Mistakes Younger Australians Can Avoid

First the bad news: many Australians in their 20s and 30s feel they are already late to investing. Property prices seem out-of-reach, the cost-of-living pressure is real, and social media can make everyone else’s financial life appear rosier than it really is. For many, the right pathway forward can feel out-of-reach.

But here’s the thing: starting your investment journey late isn’t your biggest challenge as a younger investor. It’s starting it badly.

The good news is the sooner you start on the right investment pathway, the sooner you’ll start stepping toward your goals with time on your side.

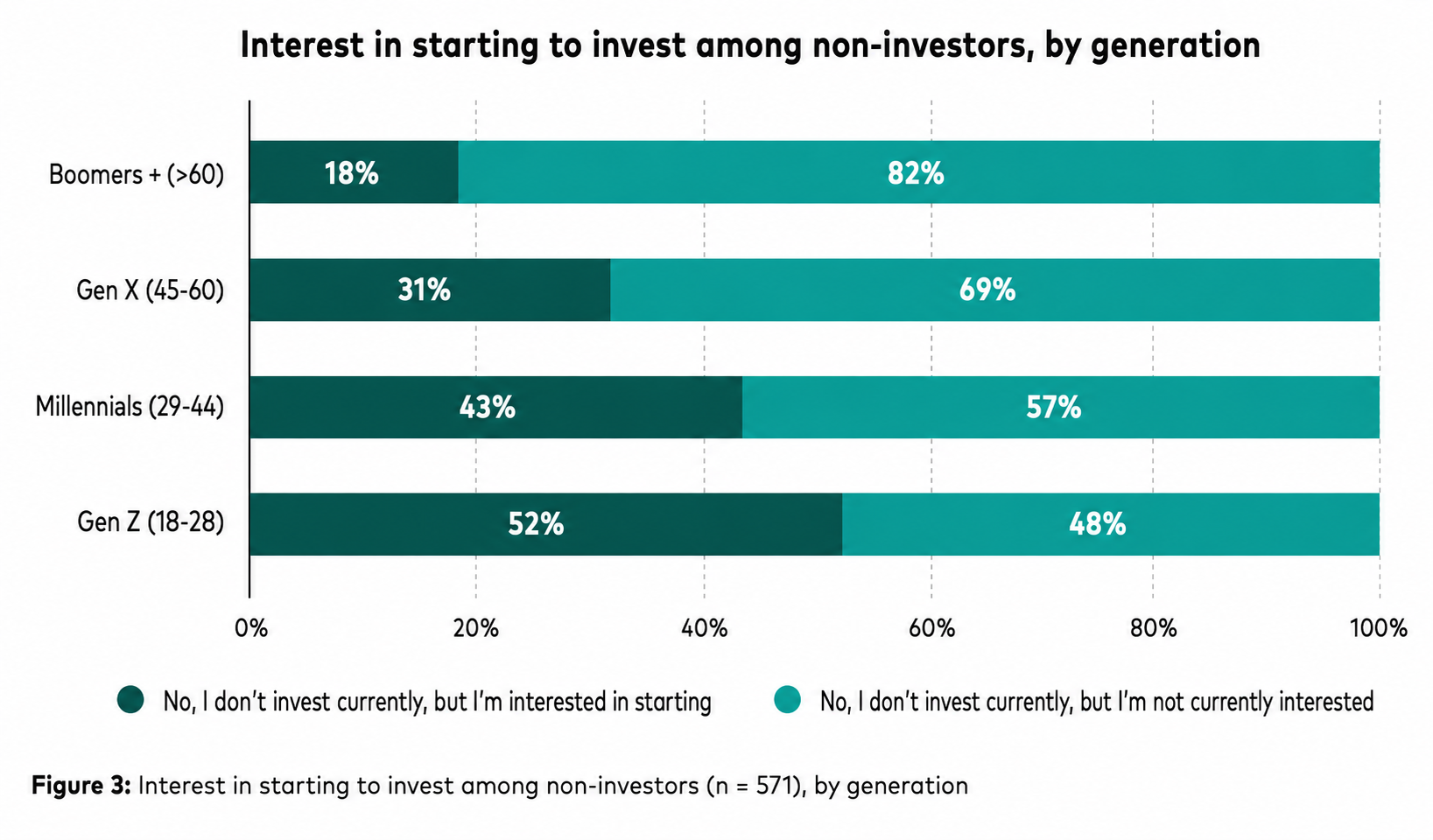

Many Young Australians are Ready to Start Investing

Many younger investors are in this boat, more ready to start investing than ever.

On that note, Vanguard Australia reported in May 2026 that nearly half of Gen Z and Millennial Australians are interested in starting their investment journeys.

So, you’re in good company.

Time is on Your Side

The biggest advantage younger budding investors have is time.

It’s hard to overstate this. If you commit to making regular investing contributions and remaining invested through the inevitable periods of volatility you’ll have to navigate, time is a superpower at your disposal.

There’s one word that explains this: compounding.

Compounding is the process of building upon previous gains or effects. In simple terms, when your annual returns add to the pie you’re building, the pie ends up growing into a much bigger pie over the long term.

This is a good time to introduce the rule of 72. It’s an easy compound return calculation to estimate how long it takes to double your money through the magic of compounding.

As shown below, you just need to divide 72 by your expected annual return to calculate how many years it will take to double your money (assuming that return is repeatable):

In short, time is of the essence, as are returns.

Hence, compounding works best when investors start as soon as they can and save regularly.

The good news for younger investors who feel behind the eight ball is that by starting now with regular annual contributions, you’ll soon be way ahead of investors who contribute a lot more at a later stage of life.

Check out the way a younger investor who contributes $5,000 p.a. for ten years from the age of twenty-five has a significantly larger portfolio at the age of sixty-five than a thirty-five-year-old who contributes $5,000 p.a. for thirty years:

While compounding is a simple strategy for success, it’s not always easy for investors to achieve.

In particular, there are five mistakes you’ll need to avoid if you’re going to optimise your long-term returns in this way:

Mistake 1: Waiting Until You Feel Ready

Many younger people delay investing because they believe they need a large lump sum, a perfect market entry point or expert-level knowledge.

That can be costly.

Interestingly, the ASX Australian Investor Study found that ETF investors tend to start younger than the broader average, with a median starting age of 28 and portfolio size of $46,500.

That’s not to say that all younger investors should only buy ETFs. The point is that widely accessible investment products like ETFs have lowered the up-front barriers to building diversified exposure.

That’s great news for younger investors. It means starting now with whatever amount you’re comfortable investing has never been easier.

Mistake 2: Confusing Excitement with Strategy

Young investors are often targeted with exciting narratives about emerging themes such as AI and crypto.

Some of these themes may warrant a position in their portfolios.

The mistake is letting the theme become the whole portfolio.

Managing your FOMO is part of it. The UK Financial Conduct Authority found in 2024 that 51% of young investors aged 18 to 40 had put in more money than originally intended into an investment because of FOMO.

ASIC has also warned that social media is pushing some young Australians towards riskier financial decisions, including cryptocurrency, based on limited or unproven information.

Here’s a useful test to help address this risk: If an investment requires urgency, secrecy or a celebrity-style endorsement to make sense of it, slow down and think twice.

Mistake 3: Owning Too Few Investments

Diversification across asset classes, geographies, and themes is a valuable strategy which allows investors to optimise their risk-adjusted returns while minimising their downside risks during market selloffs.

It’s worth mentioning that a portfolio of three popular shares is not diversified. A single thematic ETF is not diversified enough either if it is concentrated in one sector, country or trend.

Diversification means spreading your exposure across asset classes, regions, sectors, currencies and managers where appropriate.

For a young investor, a simple starting point with diversification is to own a broad Australian ETF and a global equity ETF, then consider whether fixed income, property funds, active managed funds or thematic ETFs have a role to play in their plan.

Mistake 4: Taking on the Wrong Kind of Risk

Younger investors often hear that they can afford to take on more risk because time is on their side.

That is partly true, but it’s an incomplete truth.

There’s a massive difference between rewarded and unrewarded risk.

A diversified equities ETF may be volatile but remains connected to the long-term earnings of multiple businesses. There may be market selloffs along the way, but you can be confident that over the long term, the ETF’s underlying earnings will be trending upward.

In contrast, a concentrated speculative position, geared product or illiquid private asset can behave very differently. By the nature of these types of investments, it’s common to buy them when they are being hyped; that is, when the value of the investment exceeds the discounted value of its future cash flows by a long shot. That’s unlikely to end well in most cases.

The goal shouldn’t be to avoid risk completely.

It’s to take on risks that you understand, can hold through volatility, and are being fairly compensated for.

Mistake 5: Ignoring Fees, Tax and Liquidity

An ETF or fund can have a strong story and still be a poor fit if costs are high, tax outcomes are inefficient, or the investor may need the money soon.

Hence, before investing, younger Australians should ask:

- Can I sell this easily if my circumstances change?

- What are the management fees, performance fees and transaction costs?

- Is the fund listed, unlisted liquid, or illiquid?

- Does the investment suit my timeframe?

- What role does it play alongside super, cash savings and other assets I own?

It important to remember that even the best portfolio on paper may fail if it doesn’t align with your real-life circumstances.

For example, a house deposit, career change, parental leave or business opportunity may require liquidity sooner than expected.

So, being aware of the key attributes of the products you’re investing in could save you from significant challenges down the line.

Practical Steps to Get Started

Where to begin?

- Start with your investment plan, not the products.

- Decide what your goals are: long-term growth, income, capital stability, diversification, or a mix.

- Decide on your risk profile and investment horizon (which is hopefully long-term to optimise your compounding potential).

- Put together an asset allocation plan specific to your circumstances. If this is challenging, consider getting financial advice.

- Then compare structures and start searching for the right products to execute your plan.

- ETFs may suit investors wanting low minimums, listed liquidity and broad exposure.

- Managed funds may suit investors seeking active management, potential to outperform or access to specialist strategies.

- Finally, build slowly. A sensible portfolio needs to be durable.

The Best Advice if You’re Feeling Behind

In summary, if you’re a younger investor wanting to get ahead, don’t try to catch up by taking bigger, faster bets. Catch up by building a repeatable system with a genuinely long-term investment horizon.

That means investing regularly, diversifying properly, checking fees, avoiding hype, and reviewing your portfolio without constantly tinkering. Your portfolio should fit your goals, timeframe and risk tolerance.

The powerful thing about your 20s and 30s is that small decisions have decades to compound into the type of wealth that may currently feel out-of-reach.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

Related Articles

-s5c0uf81il26meg3icyx.png)

-pp7lmjdtt5eazso52rcw.png)

Categories

Recent Articles

View all articles-5s5447cq4p0lc07q30rt.png)

-gfp1xjdx24emq6stx0qn.png)

-37f8do9xthqpg80ohvuf.png)