Sequencing Risk: Why Average Returns Don’t Matter

Simon Turner

Mon 9 Mar 2026 6 minutesInvestors are generally taught to focus on average returns as a gauge of investment success. This makes intuitive sense to most. Over the long run, developed market equities have delivered average returns of around 10% p.a. That solid result has reinforced the advice: stay invested, reinvest your dividends and compounding will do the heavy lifting for you.

The arithmetic appears reassuringly simple. Yet one of the most consequential risks investors face can’t be captured by average returns. Sequencing risk, the order in which returns occur, can determine whether identical average long-term market performance produces financial security or financial stress.

It’s All About Timing

Sequencing risk is a bigger deal than most investors realise, particularly those approaching retirement. In fact, it’s often the decisive factor separating successful wealth preservation from permanent capital erosion.

As Nobel laureate William Sharpe observed, ‘investors consume returns in sequence, not in averages’.

Morningstar research shows that portfolios subject to withdrawals during early market downturns suffer disproportionate damage because capital removed during losses no longer participates in subsequent recoveries.

Two investors may experience the same average annual return over twenty years, yet end with dramatically different outcomes depending on when their loss-making periods occur.

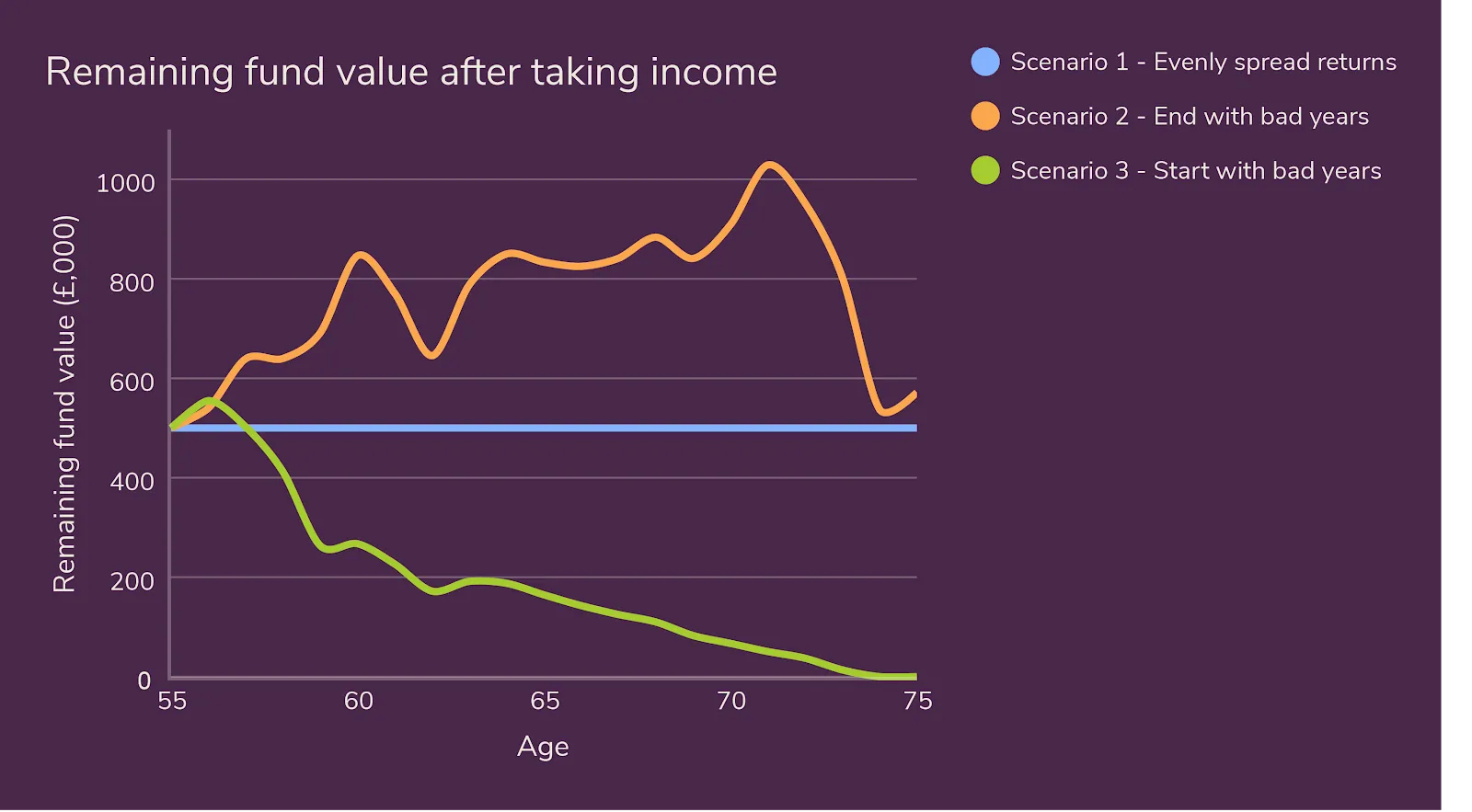

Consider this simple example. A portfolio falls 20% in its first year, and then rises 25% the following year. The average return across the two years is modestly positive. Yet, an investor who’s dependent on their portfolio for income and locks in the year one capital loss out of fear, is unlikely to recapture their losses by later gains.

In other words, if a portfolio suffers a significant drawdown earlier rather than later, it’s risk of not recovering is much higher, as shown below.

The sequence of returns risk is most acute in the five to ten years surrounding retirement, a period sometimes described as the retirement danger zone.

So long-term averages describe markets but not investor experiences. In the real world, portfolios have to navigate withdrawals, emotional behaviour and market volatility simultaneously. Theory tends to go out the window when the sequence of events is at odds with investors’ goals.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

An Australian Perspective

Australian investors face additional sequencing complexity due to compulsory superannuation contributions and concentrated exposure to equity markets through both domestic and global equities.

Case in point: Australian superannuation funds remain heavily allocated to growth assets, with equities accounting for nearly half of assets, even near retirement. The country has one of the most growth-oriented retirement sectors in the world.

In short, such high equity exposure supports a portfolio’s long-term growth prospects but increases its vulnerability to early retirement drawdowns if markets fall sharply.

For example, during the Global Financial Crisis, the MSCI World Index declined 54% from peak to trough between 2007 and 2009. Investors still accumulating assets during this selloff recovered and thrived over time. However, retirees drawing income and reacting defensively during that period will have experienced structurally lower portfolio returns ever since, despite markets eventually rebounding.

Sequencing risk, therefore, can transform market volatility from a temporary inconvenience into a permanent structural threat.

The deeper lesson is philosophical as much as mathematical.

Markets reward patience over decades, while investors’ financial lives unfold year by year.

The question is whether investors’ portfolios can be held onto long enough to benefit from the recovery that tends to follow major market selloffs.

Navigating the Uncertainties of Sequencing

Most investors tend to think of diversification as across asset classes, but with sequencing risk lurking in the background, it may be more realistic to think about it in terms of return drivers.

For example, a study by Wade Pfau and Michael Kitces demonstrated that portfolios combining equities with defensive income assets significantly improved retirement sustainability by reducing early drawdown risk and severity. They concluded that managing volatility early in retirement matters more than maximising long run average returns.

There are a number of practical implications for investors:

- Reframe Your Investment Goals Around Resilience and Survivability.

Rather than chasing the maximum possible return, sequencing-aware investors may be more prudent to optimise their portfolios for survivability across the uncertain sequences of an infinite number of potential market outcomes.

This perspective aligns with behavioural finance findings showing investors are more sensitive to losses than gains. Large early losses often trigger emotional decision making, compounding sequencing damage through poorly timed selling.

- Consider Flexible Withdrawal Strategies.

Vanguard research shows that dynamic spending rules, whereby withdrawals adjust modestly in response to market performance, significantly extend portfolio longevity compared with fixed withdrawal rates.

In practice, this means allowing your spending to fluctuate within reasonable boundaries rather than enforcing rigid income targets regardless of market conditions.

- Multi-Asset ETF and Funds Reduce Drawdown Risk.

The growing popularity of diversified multi-asset fund and ETFs reflects their generally resilient performance profiles.

These funds integrate equities, bonds and alternative exposures within a single structure designed to moderate drawdowns while preserving long-term compounding potential.

- Global Exposure is a Powerful Core But Be Ready For Volatility.

Exposure to global equities through diversified global market funds and ETFs offer essential growth participation.

However, it’s important to be aware that growth assets can’t reduce your exposure to sequencing risk. Defensive allocations that behave differently during periods of equity stress are the critical stabilisers all portfolios need.

- Fixed Income Has a Role to Play

Global fixed income ETFs and funds also provide diversification benefits through government and investment grade bond exposure that historically cushions equity downturns.

- Maintaining a Cash Buffer Plays an Underappreciated Role.

Research from the US-based Retirement Research Center found that maintaining several years of spending needs in low volatility assets meaningfully reduces the probability of portfolio depletion because withdrawals occur from stable reserves rather than depressed equities.

In other words, holding a solid cash weighting helps investors to ride out the volatility of investment markets.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Sequencing Risk Growing in Importance

In an era defined by rising geopolitical risk, sequencing risk may be becoming a more prominent portfolio management issue, particularly for older investors. So investors who anchor their decisions solely on average performance data may be misunderstanding the fragility embedded within real world portfolios.

Ultimately, successful investing is less about predicting returns than managing the path those returns take. Compounding works only when capital remains intact. As financial historian Peter Bernstein once wrote, ‘survival is the only road to riches’. Recognising that average returns do not determine long-term outcomes may be the most important step you can take toward ensuring your wealth endures through to retirement.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.