-tocogsj3zy2mt2vfay5i.png)

Why more Australians are turning to SMSFs for retirement planning

The trend of Australians taking control of their own superannuation investments has been steadily rising over the years. Despite challenges like sticky inflation and higher-for-longer interest rates, the self-managed superannuation fund (SMSF) sector has shown remarkable resilience, surpassing the significant milestone of $1 trillion in assets last year.

According to ATO data, there are over 621,809 SMSFs in Australia, collectively managing nearly $1.02 trillion in assets. This growth includes a 1.6% increase in the number of SMSFs during the September quarter, and a 4.3% rise over the past year, highlighting its growing appeal as a do-it-yourself solution for retirement planning.

Source: CLASS 2024 annual benchmark report

What is an SMSF?

A Self-Managed Superannuation Fund is a type of superannuation fund that lets individuals take complete control of their retirement savings. Instead of professional fund managers making investment decisions on investors’ behalves, as happens in traditional super funds, SMSF members serve as trustees of their own SMSFs.

As trustees, they decide where to invest, choosing from options like Australian equities, property (commercial and retail), cash, term deposits, and managed funds, while complying with Australian Taxation Office (ATO) regulations.

Why SMSFs are so popular

SMSFs are gaining momentum in Australia, thanks in large part to their strong performance—particularly during market downturns.

Research from the University of Adelaide’s International Centre for Financial Services found that SMSFs outperformed regular super funds by 4.1% in 2021–22, thanks to limited exposure to overseas assets—a pattern also seen during the 2008 Global Financial Crisis.

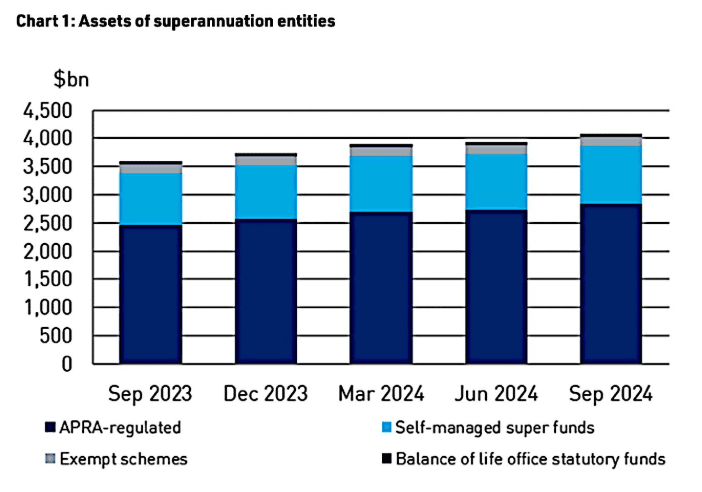

This track record has helped build trust among Australians, with more than 1.15 million people now using SMSFs, which collectively hold around a third of the nation’s $4.1 trillion in super assets.

Source: APRA

For the SMSF sector, with about half the funds in the retirement phase, a resilient portfolio is essential to preserve capital.

But it’s not just outperformance during bear markets that makes SMSFs appealing. These funds come with several unique benefits that are attracting more investors every year:

1. Strategic control over investments

The main motivation for establishing an SMSF is greater autonomy over investments and the freedom to tailor a portfolio that aligns with your financial goals and risk appetite.

Trustees can invest in property, shares, managed funds, and more—choices often managed by professionals in traditional super funds.

In fact, SMSFs are the only way you can use your superannuation benefits to directly invest in residential property, provided it is solely providing retirement benefits.

This control can improve investors’ tax planning and risk management.

This investment flexibility, autonomy, and ability to implement real-time solutions make SMSFs particularly appealing to younger, more engaged trustees. The average age of new SMSF members has dropped, with individuals in their mid-30s to mid-40s now making up 30% of newly established SMSFs—a clear sign of the increasing preference for hands-on retirement management.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

2. Estate Planning

SMSFs can be helpful in estate planning due to the extra flexibility they provide compared to public superannuation funds.

They enable families to consolidate their retirement savings and plan more efficiently for the future, as well as to create tailored estate plans that align with a family’s unique dynamics.

SMSF members also have more options for beneficiary nominations than those typically available in public funds and can even choose to establish an SMSF will, further enhancing their estate planning flexibility.

3. Cost-effectiveness for larger balances

Cost-effectiveness can be a key advantage for people with larger super balances, as the per-member expense of running an SMSF can sometimes be lower than for a traditional super fund.

Additionally, SMSFs can include up to six members, allowing families to pool their resources and invest together. However, the fees involved in setting up and maintaining an SMSF—such as audit, administration, and legal costs—can be disproportionately high for smaller balances.

Challenges and considerations

While SMSFs provide unparalleled control and flexibility for retirement planning, they also demand substantial time, expertise, and resources.

One of the most significant challenges is adhering to the strict guidelines set by the ATO, which include rigorous reporting and auditing requirements. SMSF compliance can be complex, requiring detailed knowledge of regulatory frameworks and a meticulous approach to administration.

Planning ahead is also crucial, particularly when considering how and when to exit the fund. Life events such as the death or incapacity of a member or relationship breakdowns can trigger the need to wind it up. This process often involves extensive paperwork, tax implications, and decisions about reinvesting or distributing the superannuation assets.

Therefore, financial literacy is a non-negotiable for SMSF trustees. Even if some tasks are outsourced, it’s vital for all members to have a clear understanding of where their money is invested.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Taking charge of your retirement with SMSFs

Superannuation is often a person’s largest asset after their family home, and it’s natural to want greater control over how it’s managed. SMSFs offer precisely that—hands-on control that enables trustees to craft an investment strategy tailored to their financial goals and risk tolerance.

However, with this control comes significant responsibility. Trustees must manage compliance, make strategic investment decisions, and dedicate time to administration. Non-compliance carries serious penalties, making financial literacy and diligence essential.

For those ready to meet these demands, SMSFs can be a rewarding option.

Disclaimer: This article is prepared by Ankita Rai for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Ankita Rai

Finance Journalist

Related Articles

-62itb6ivjyp6irexulrl.png)

-jadpty6yyvte3cbjel3k.png)

Recent Articles

View all articles-4yb643awg03namrcahu4.png)

-zrxpxihmn0inisejx8wx.png)

-vke5r81en85n0lawxvqo.png)